GAO

United States Government Accountabilit

y

Office

Report to Congressional Committees

TROUBLED ASSET

RELIEF PROGRAM

Status of Government

Assistance Provided

to AIG

September 2009

GAO-09-975

What GAO Found

United States Government Accountability Office

Why GAO Did This Study

Highlights

Accountability Integrity Reliability

September 2009

TROUBLED ASSET RELIEF PROGRAM

Status of Government Assistance Provided to AIG

Highlights of GAO-09-975, a report to

congressional committees

The Federal Reserve and Treasury provided assistance to AIG to limit further

disruption to financial markets. These agencies determined that market events

could have caused AIG to fail, which would have posed systemic risk to the

financial system. According to the Federal Reserve, a disorderly failure of AIG

would have contributed to higher borrowing costs and additional failures, further

destabilizing fragile financial markets. The Federal Reserve and Treasury

determined that an AIG default would place considerable pressure on AIG’s

counterparties and trigger serious disruptions to an already distressed

commercial paper market. They concluded that because AIG was a large seller of

credit default swaps—protection against losses from defaults—on collateralized

debt obligations (CDO), had AIG failed, its counterparties would have been

exposed to large losses if the values of the CDOs had continued to decline and

AIG defaulted on its contracts. The Federal Reserve intended the initial

September 2008 assistance to enable AIG to meet these added obligations with its

counterparties and begin the process of selling business lines to raise monies to

repay the government and resolve other liabilities. Subsequent assistance in

November 2008 and March 2009 was intended to augment these goals, support

liquidity needs, and repay FRBNY while mitigating disruptions in the broader

financial markets.

To address systemic risk that could result if AIG were to fail, the Federal Reserve

and Treasury made over $182 billion available to assist AIG between September

2008 and April 2009. As of September 2, 2009, AIG’s outstanding balance of

assistance was $120.7 billion. Some federal assistance was designated for specific

purposes, such as a special purpose vehicle to provide liquidity for purchasing

assets such as CDOs. Other assistance, such as that available through the

Treasury’s Equity Facility, is available to meet the general financial needs of the

parent company and its subsidiaries. The table on the next page provides an

overview of the total federal assistance to AIG and its related entities. Repayment

of the $120.7 billion outstanding government exposure is expected to come from

various sources. As of September 2, 2009, $6.8 billion was paid toward principal

on the Maiden Lane facilities created by FRBNY to purchase certain AIG assets

and provide AIG with liquidity. In providing the assistance, the Federal Reserve

and Treasury have taken several steps intended to protect the government’s

interest. These include making loans that are secured with collateral, instituting

certain controls over management, and obtaining compensation for risks such as

charging interest, requiring dividend payments, and obtaining warrants. Moreover,

Federal Reserve and Treasury staff routinely monitor AIG’s operations and

receive reports on AIG’s condition and restructuring. While these efforts are being

made, the government remains exposed to risks, including credit risk and

investment risk, which could result in the Federal Reserve and Treasury not being

repaid in full.

While federal assistance has helped stabilize AIG’s financial condition, GAO-

developed indicators suggest that AIG’s ability to restructure its business and

repay the government is unclear at this time. Indicators of AIG’s financial risk

suggest that since AIG reported significant losses in late 2008, AIG’s operations,

with federal assistance, have begun to show signs of stabilizing in mid 2009.

Similarly, after a declining trend through 2008 and early 2009, indicators of AIG

insurance companies’ financial risk suggest improved financial conditions that

were largely results of federal assistance. Indicators of AIG’s repayment of federal

GAO’s seventh report on the Troubled

Asset Relief Program (TARP) focuses

on the initial assistance the

government provided to American

International Group, Inc. (AIG)—an

organization with over 200 companies

operating in over 130 countries and

jurisdictions and $830 billion in

assets—in September 2008 and the

restructuring of that assistance in

November 2008 and March 2009. The

unfolding crisis threatened the stability

of the U.S. banking system and the

solvency of a number of financial

institutions, including AIG. In

September 2008, downgrades of AIG’s

credit rating prompted collateral calls

by counterparties and raised concerns

that a rapid and disorderly failure of

AIG would further destabilize the

markets. As a result, the Board of

Governors of the Federal Reserve

System (Federal Reserve) authorized

the Federal Reserve Bank of New York

(FRBNY), in consultation with the

Department of the Treasury (Treasury),

to provide assistance to AIG. This

report describes (1) the basis for the

federal assistance, (2) the nature and

type of assistance and steps intended

to protect the government’s interest,

and (3) selected GAO-developed

indicators of the status of federal

assistance and AIG’s financial

condition.

To do this, GAO reviewed signed

agreements and other relevant

documentation from the Federal

Reserve, FRBNY, Treasury, and AIG

and interviewed their officials, among

others. To develop the indicators, GAO

reviewed rating agencies’ reports,

identified critical activities, and

discussed them with the above named

agencies and AIG.

Treasury had no substantive comments

on the report. It provided technical

comments along with the Federal

Reserve, FRBNY, and AIG.

View GAO-09-975 or key components.

For more information, contact Orice Williams

Brown at (202) 512-8678 or

United States Government Accountability Office

Highlights of GAO-09-975 (continued)

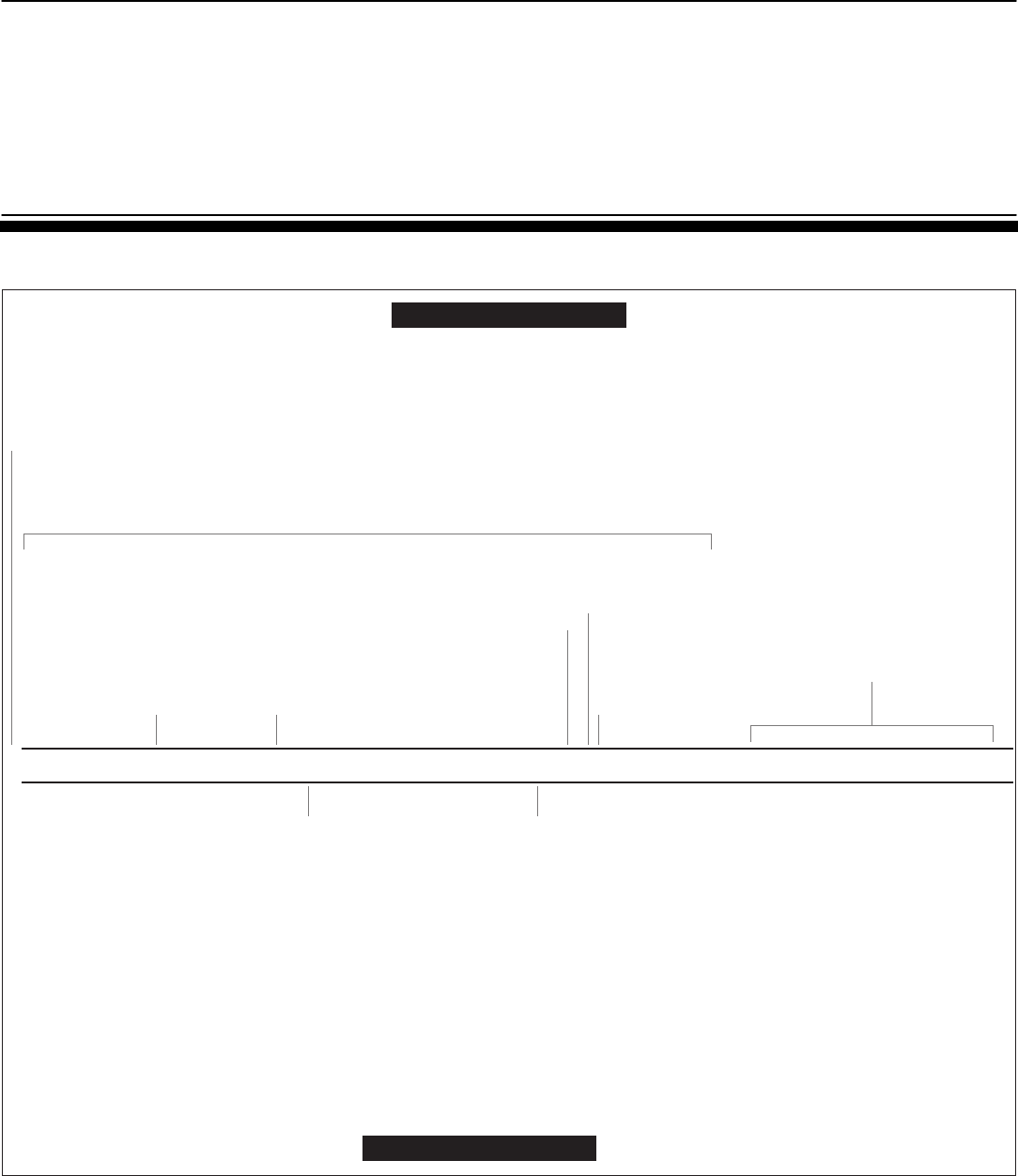

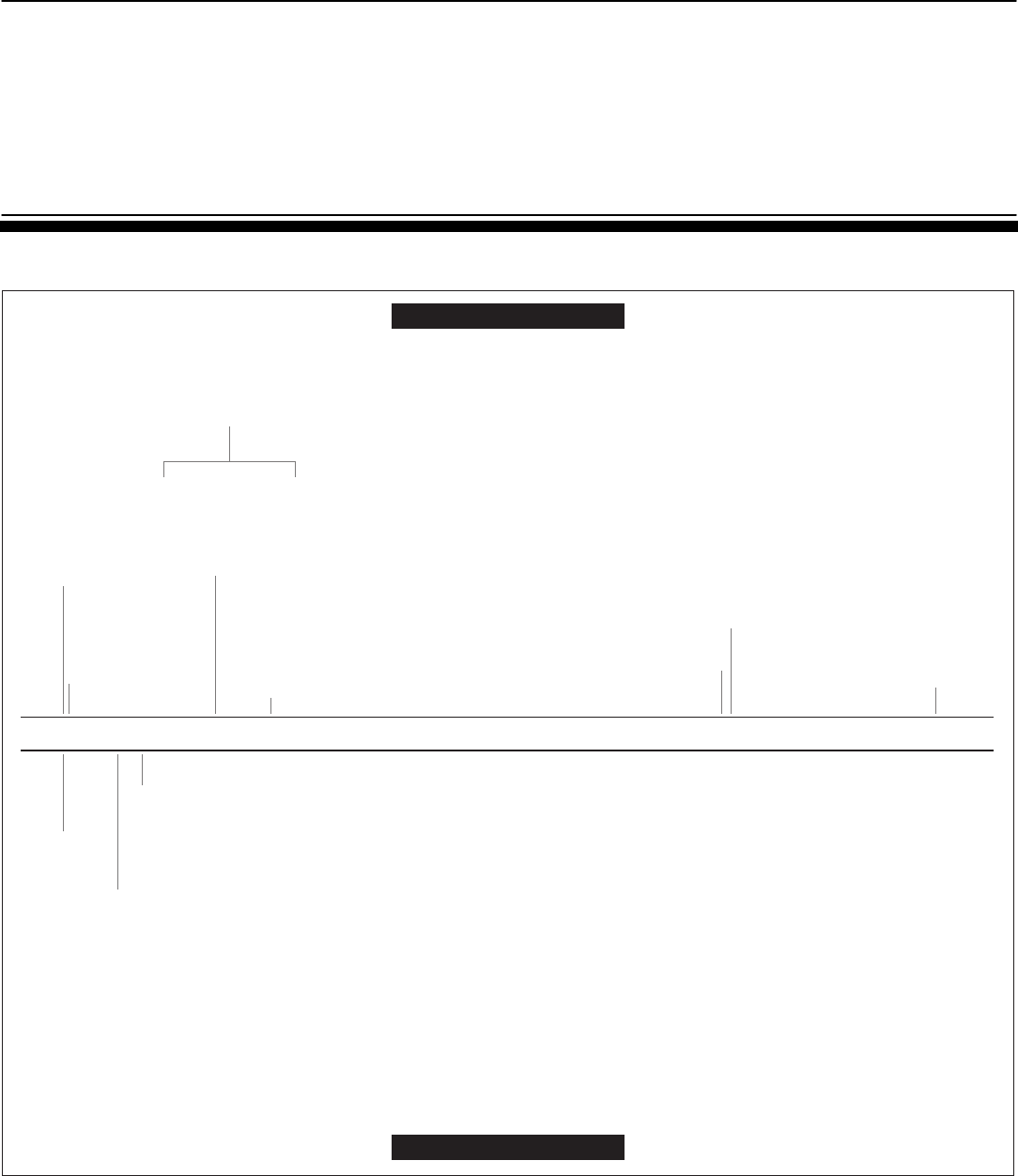

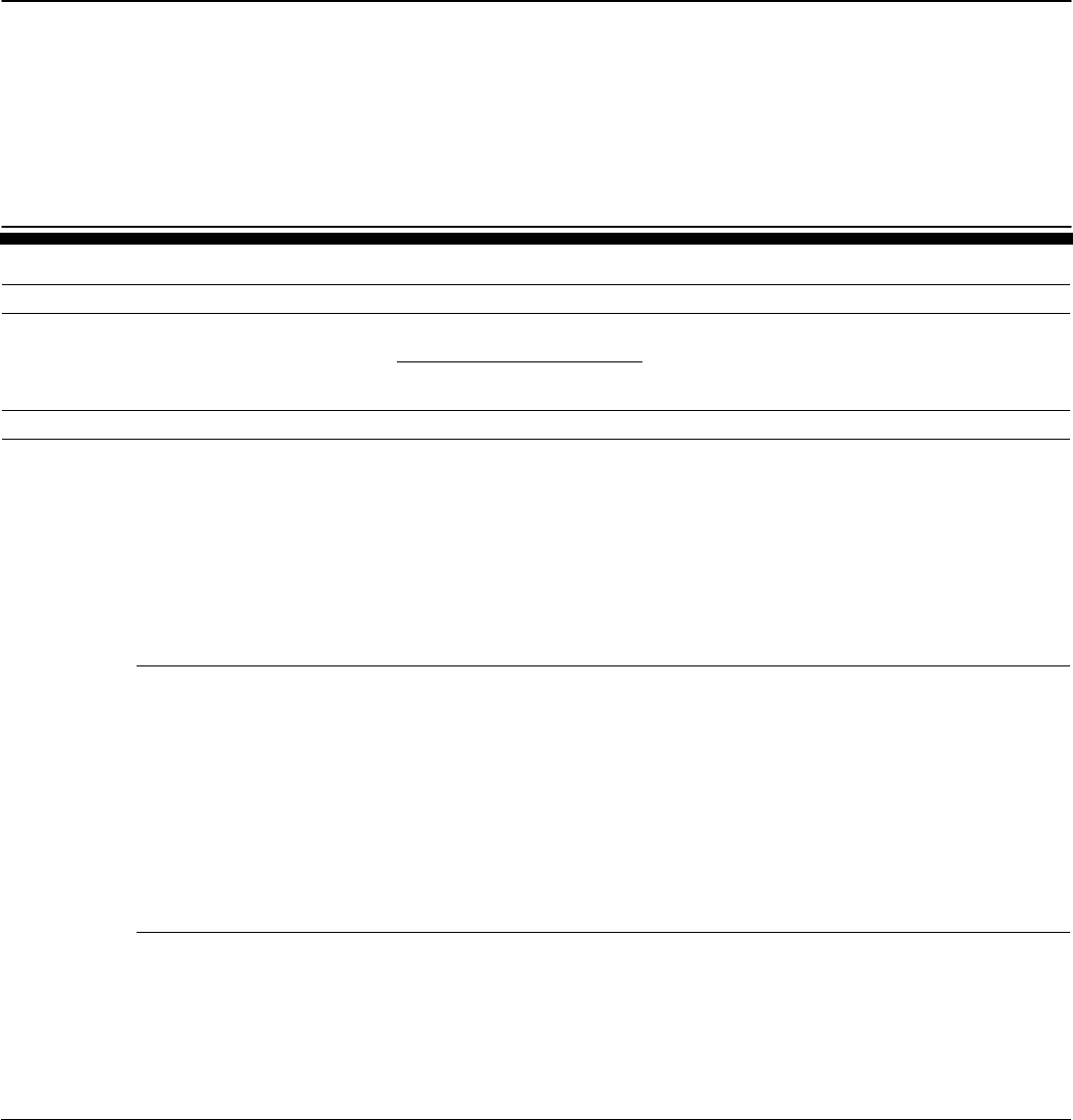

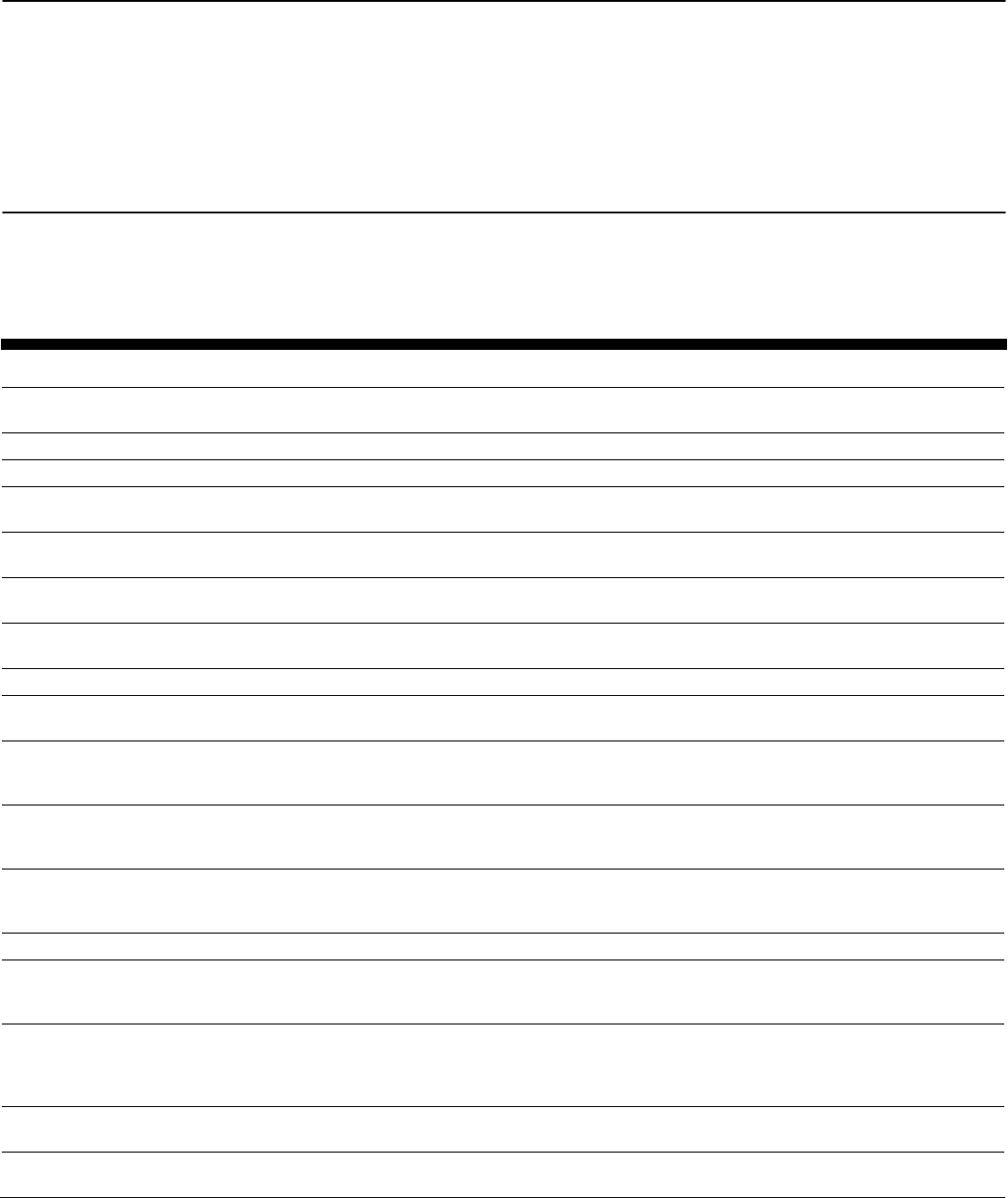

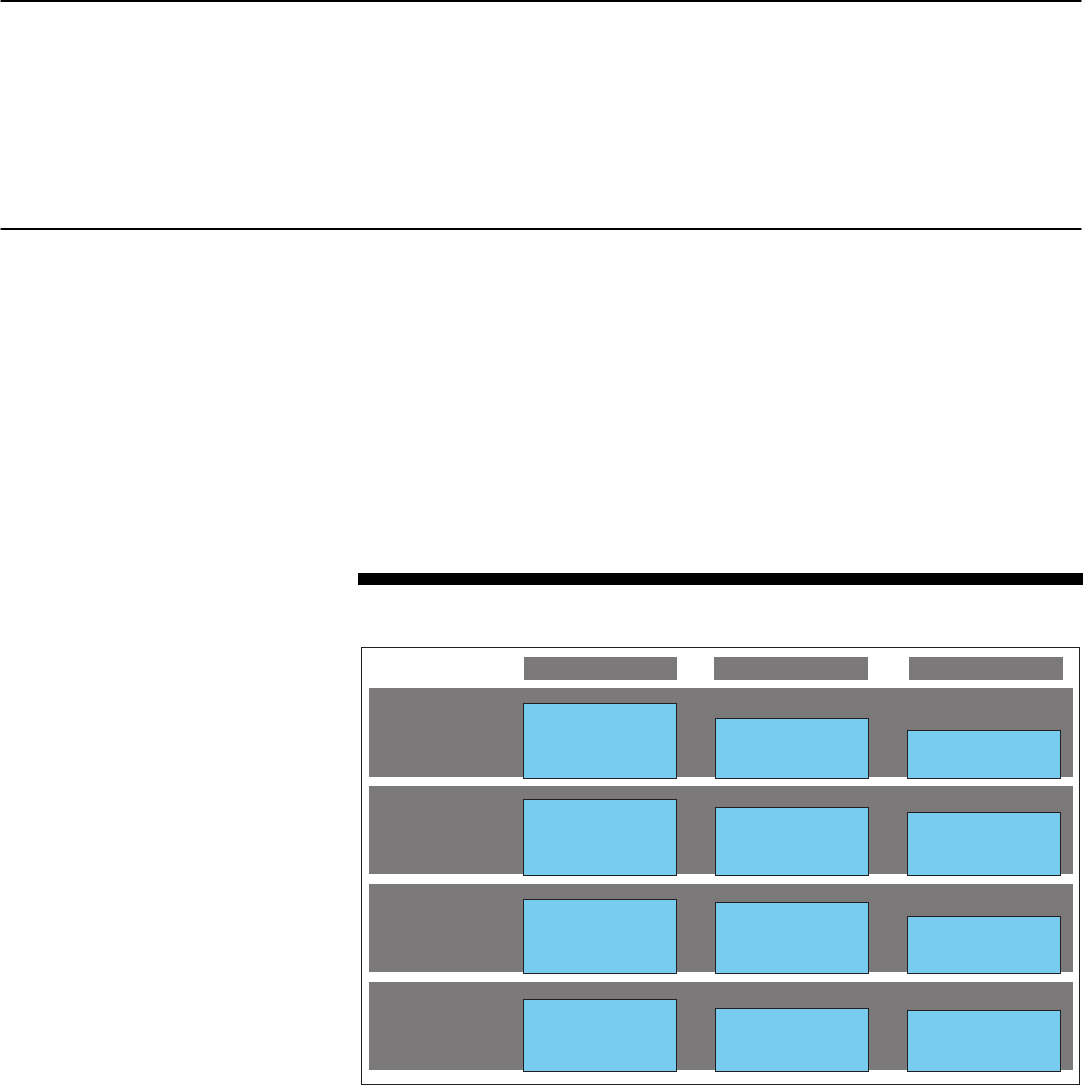

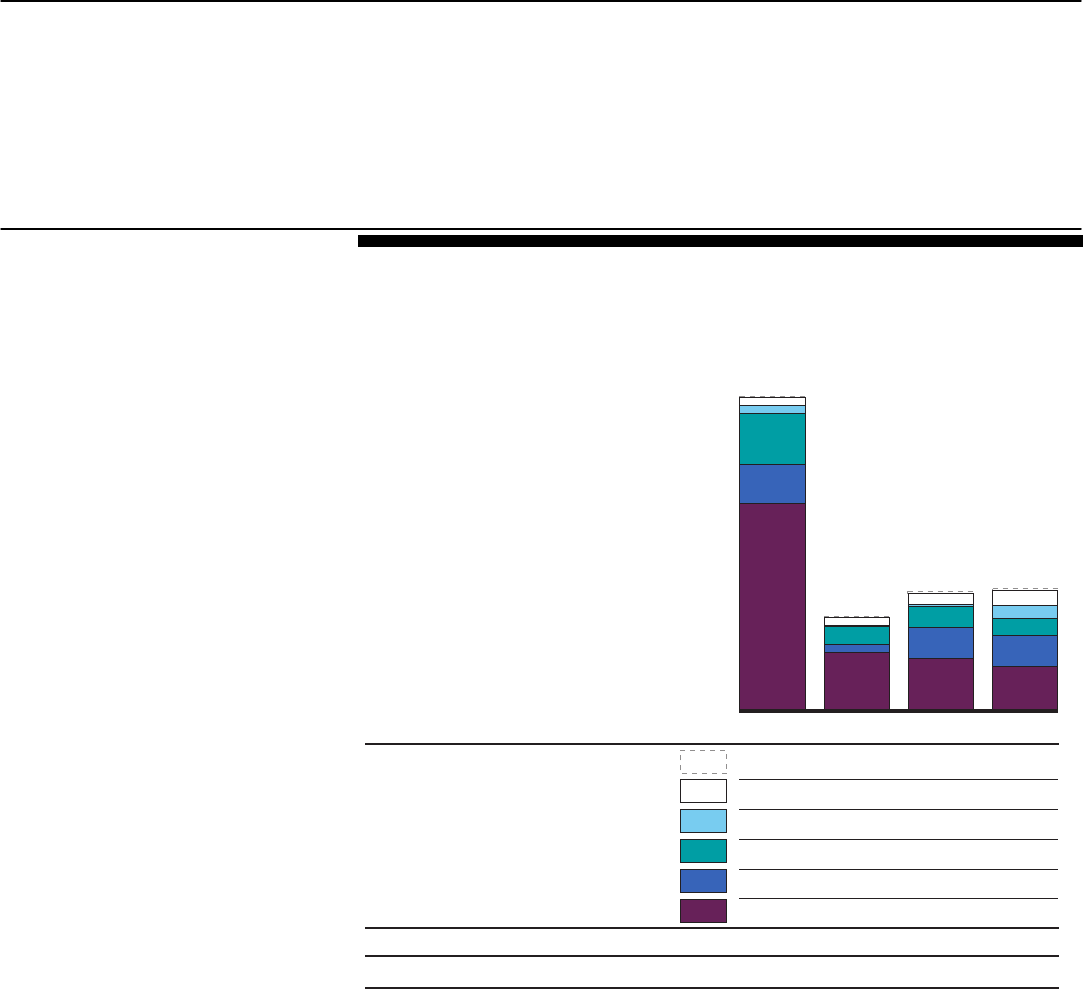

Overview of Federal Assistance Provided to AIG as of September 2, 2009

Dollar in millions

Amount of assistance

authorized

Description of the federal assistance

Debt Equity

Outstanding

balance Sources to repay the government

Implemented

Federal

Reserve

FRBNY created a Revolving Credit Facility to

provide AIG a revolving loan that AIG and its

subsidiaries could use to enhance their liquidity.

In exchange for the facility, for $0.5 million, a

Treasury trust received Series C preferred stock

for the benefit of the Treasury, which gave

Treasury a 77.9 percent voting interest in AIG.

$60,000

a

$38,792.5 Proceeds from dispositions of AIG

businesses, internal cash flows, and

restructuring part of the Revolving Credit

Facility from debt into equity. The initial fee

paid by AIG was reduced by $0.5 million to

pay for the Series C shares and will not be

repaid.

FRBNY created SPV—Maiden Lane II—to

provide AIG liquidity by purchasing residential

mortgage-backed securities from AIG life

insurance companies. FRBNY provided a loan to

the SPV for the purchases. It also terminated a

previously established securities lending

program with AIG.

22,500 16,899 Proceeds from the assets in Maiden Lane II

will be used to repay the FRBNY loan to

Maiden Lane II.

FRBNY created a SPV called Maiden Lane III to

provide AIG liquidity by purchasing CDOs from

AIG Financial Products’ counterparties in

connection with termination of credit default

swaps. FRBNY again provided a loan to the SPV

for the purchases.

30,000 20,196 Proceeds from the assets in Maiden Lane

III will be used to repay the FRBNY loan.

Treasury

Treasury purchased Series D cumulative

preferred stock from AIG. AIG used the proceeds

to pay down the Revolving Credit Facility. These

shares were later exchanged for Series E

noncumulative preferred shares. Unpaid

dividends on the series D shares were added to

the Treasury’s equity in the Series E shares.

40,000 41,605 Proceeds from dispositions of AIG

businesses and internal cash flows of AIG.

Treasury purchased Series F noncumulative

preferred shares of AIG and is allowing AIG to

draw up to $29,835 million through an equity

facility to meet its liquidity and capital needs.

Amounts drawn by AIG represent the cost of the

federal equity interest in these shares.

29,835 3,206

b

Proceeds from dispositions of AIG

businesses and internal cash flows of AIG.

Subtotals $112,500 $69,835

Total authorized and outstanding assistance

c

$182,335 $120,698.5

Pending

AIG created two SPVs to hold the shares of two

of its foreign life insurance businesses to

enhance AIG’s capital and liquidity, and to

facilitate an orderly restructuring of AIG. The

Revolving Credit Facility will be reduced by the

amount of preferred equity interest in the SPVs

to be received by FRBNY.

0 (25,000

d

) 0 Proceeds from the public sale of the SPVs’

common stock could be used to buy out the

federal preferred equity and pay down part

of the Revolving Credit Facility.

AIG will create SPVs that will issue up to $8,500

million in notes to FRBNY, which will be funded

with a loan from FRBNY. AIG will use the

proceeds to pay down part of the Revolving

Credit Facility.

(8,500

d

) 0 FRBNY’s loan to the SPVs will be repaid

from net cash flows of the life insurance

policies.

Source: AIG SEC filings, Federal Reserve, and Treasury data

.

a

The facility was initially $85 billion but was reduced to $60 billion in November 2008.

b

Amount as of September 8, 2009.

c

Does not include AIG’s participation in the Federal Reserve’s Commercial Paper Funding Facility.

d

These transactions have not been completed and are not included in the total assistance provided to AIG. The

amount of the Revolving Credit Facility will be decreased by an equal amount upon completion.

assistance show some progress in AIG’s ability to repay

the federal assistance; however, improvement in the

stability of AIG’s business depends on the long-term

health of the company, market conditions, and continued

government support. Therefore, the ultimate success of

AIG’s restructuring and repayment efforts remains

uncertain. GAO plans to continue to review the Federal

Reserve’s and Treasury’s monitoring efforts and report on

these indicators to determine the likelihood of AIG

repaying the government’s assistance in full and the

government recouping its investment.

Page i GAO-09-975

Contents

Letter 1

Background 4

The Federal Reserve and Treasury Provided Assistance to AIG to

Limit Systemic Risk to the Financial Markets 10

The Federal Reserve, FRBNY, and Treasury Have Taken a Variety

of Steps to Stabilize AIG 27

In Providing Assistance to AIG, the Federal Reserve and Treasury

Have Taken Steps to Protect the Government’s Interest, but

Risks Still Remain 36

Federal Assistance Has Helped Stabilize AIG’s Financial Condition,

but Indicators Suggest that It Is Too Soon to Evaluate AIG’s

Ability to Restructure Its Business and Repay the Government 43

Agency Comments and Our Evaluation 51

Appendix I Comments from the Department of the Treasury 55

Appendix II Overview of the American International

Assurance and American Life Insurance Company

Transactions

56

Appendix III Overview of the Executive Compensation

Restrictions 59

Appendix IV Summary of Rating Agencies’ Ratings 61

Appendix V Overview of the AIG Risk and Repayment

Indicators 62

Appendix VI GAO Contact and Staff Acknowledgments 91

Troubled Asset Relief Program

Related GAO Products 92

Tables

Table 1: U.S. Government Efforts to Assist AIG and the

Government’s Remaining Exposure, as of September 2,

2009 28

Table 2: Overview of Indicators of AIG’s Financial Risk and

Repayment of Federal Assistance 62

Table 3: Credit Ratings, as of March 31, 2009, and May 15, 2009 64

Table 4: Sources and Amounts of Available Corporate Liquidity at

November 5, 2008; February 18, 2009; April 29, 2009; and

July 29, 2009 67

Table 5: Composition of U.S. Government Efforts to Assist AIG and

the Government’s Remaining Exposure, as of September 2,

2009 (dollars in millions) 84

Table 6: Dispositions Closed and Agreements Announced but not

yet Closed, Second Quarter of 2008 through September 5,

2009 (dollars in millions) 89

Figures

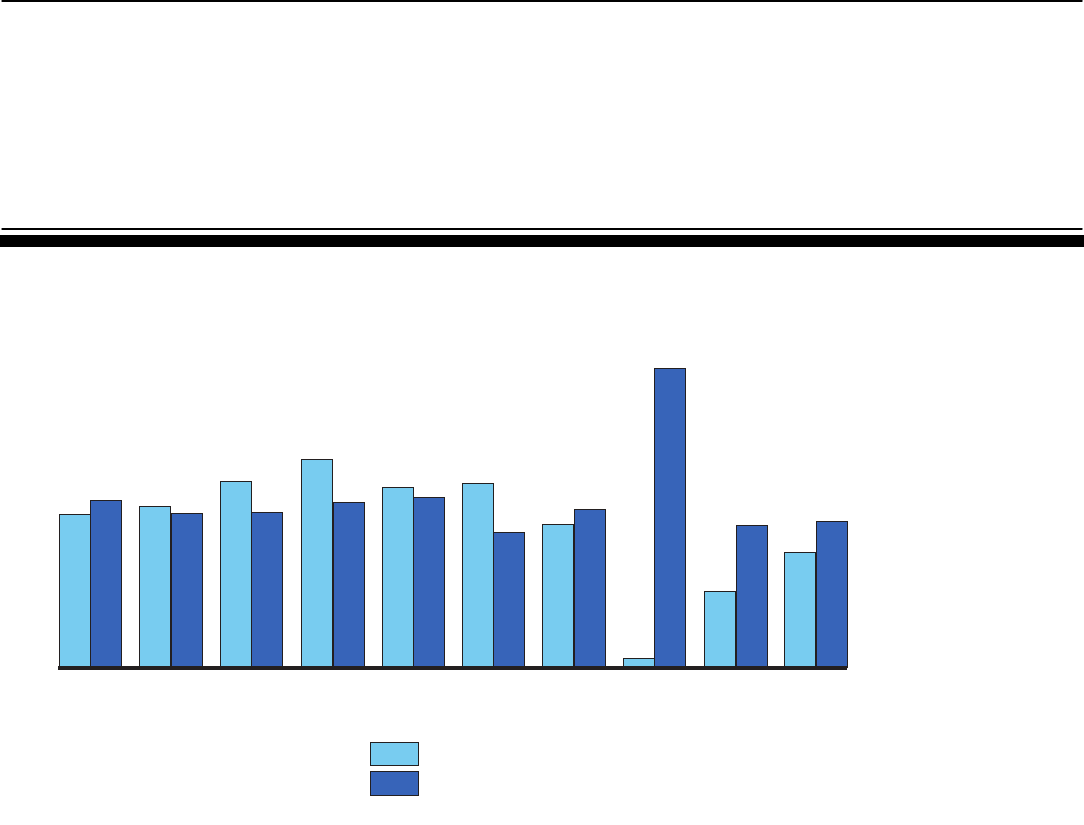

Figure 1: AIG Organizational Structure, as of December 31, 2008 6

Figure 2: Timeline of AIG’s Financial Difficulties and Government

Actions in Response to Market Turmoil, Fall 2007 to

September 30, 2008 14

Figure 3: Timeline of the Restructuring of AIG’s Assistance, Market

Events, and Related Government Actions, October 1,

2008, to April 30, 2009 24

Figure 4: AIG Restructuring and SPV Sale 57

Figure 5: AIG: Corporate Available Liquidity and Company-Wide

Debt Projections (dollars in millions), Third Quarter of

2008 through Second Quarter of 2009 66

Figure 6: AIG: Trends in and Main Components of Consolidated

Shareholders’ Equity, Fourth Quarter of 2007 through

Second Quarter of 2009 68

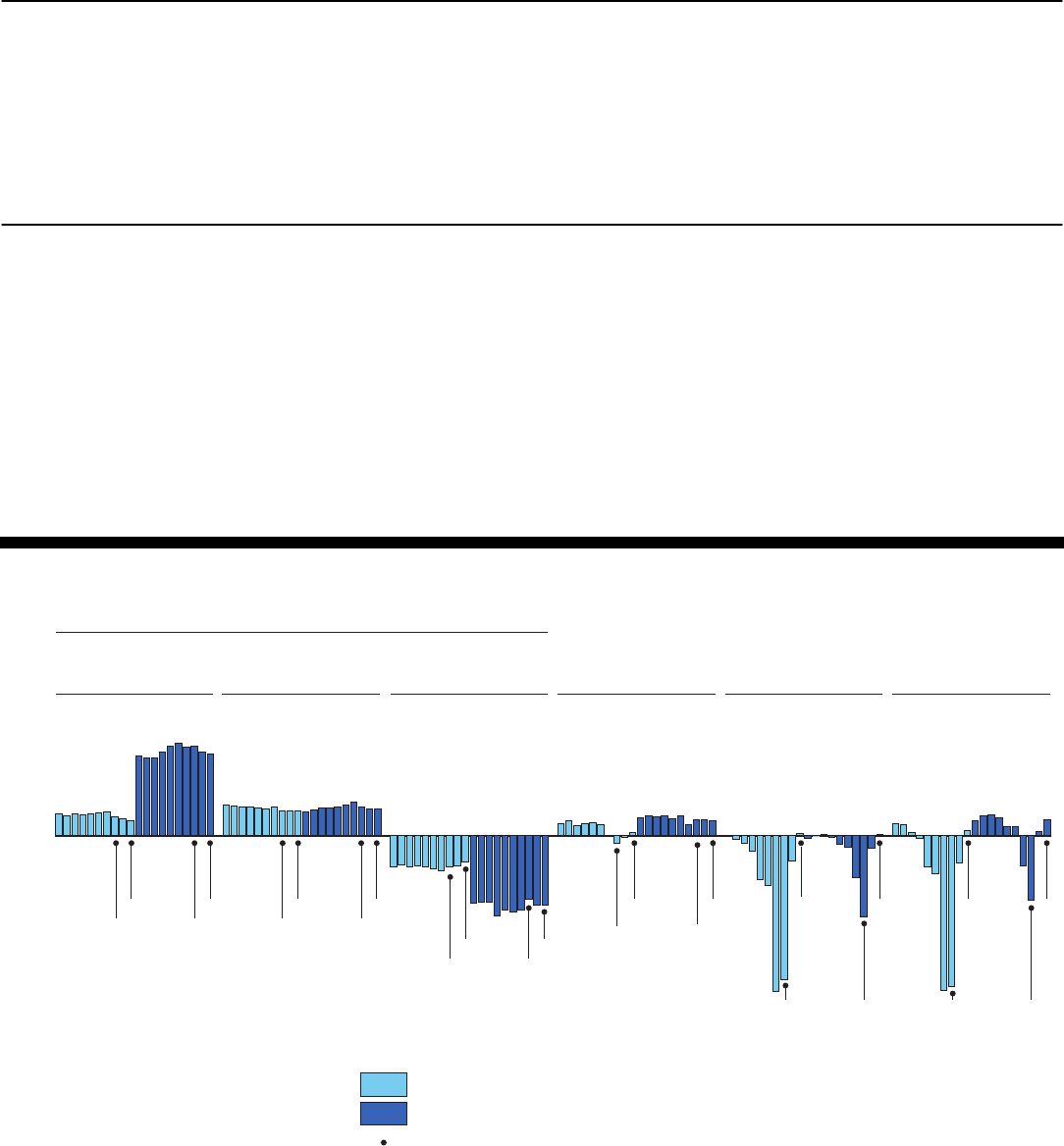

Figure 7: AIG’s Operations by Major Segment: Operating

Income/Loss Before Taxes, First Quarter of 2008 through

Second Quarter of 2009 70

Page ii GAO-09-975 Troubled Asset Relief Program

Figure 8: Status of the Winding Down of AIG’s Financial Products

Corporation, as of September 30, 2008; December 31,

2008; and March 31, 2009 71

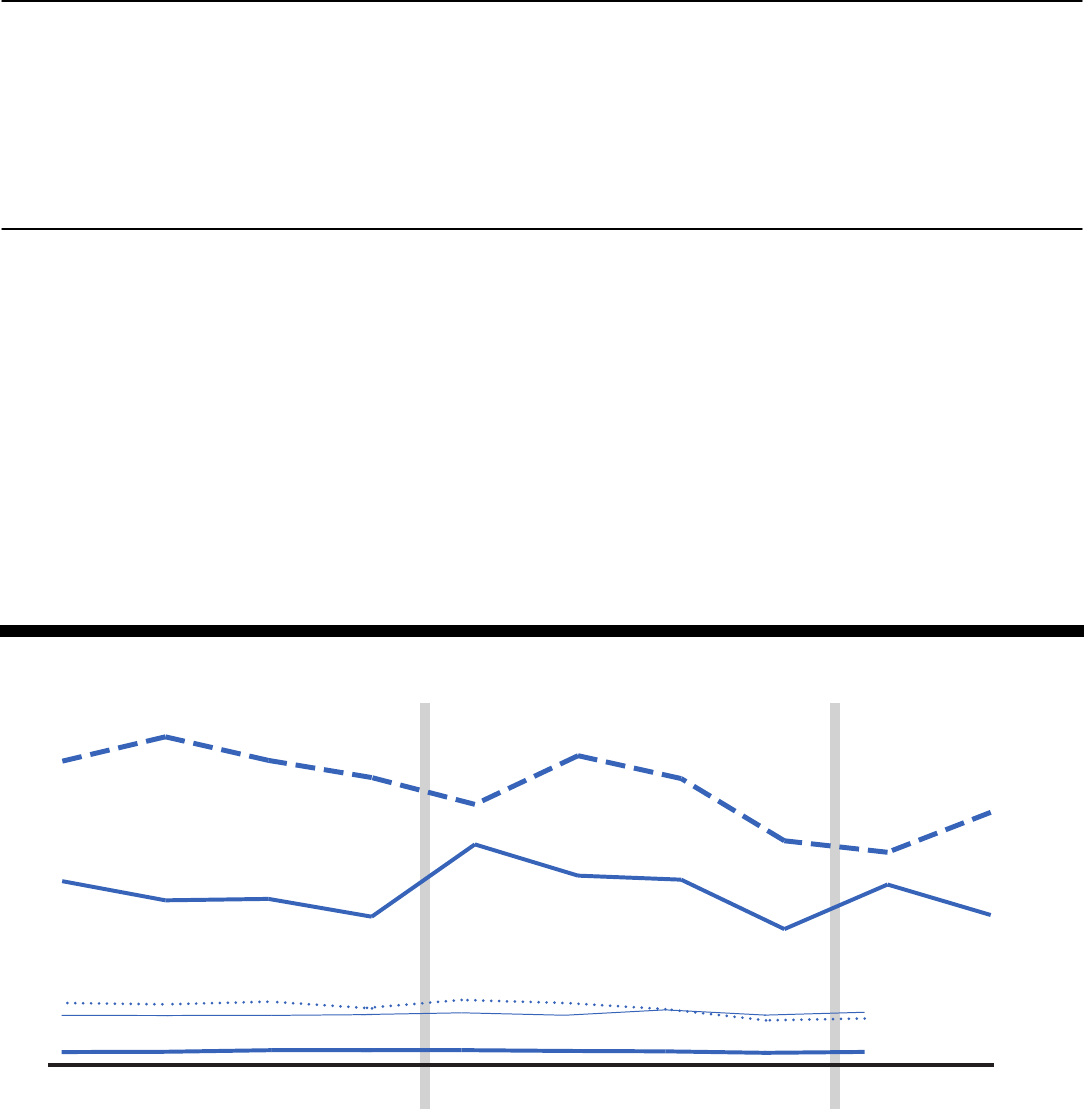

Figure 9: AIGFP: Super Senior Credit Default Swap Portfolio Net

Notional Amount, Fair Value of Derivative Liability, and

Unrealized Market Valuation Gains and Loss, Third

Quarter of 2008 through Second Quarter of 2009 73

Figure 10: AIGFP: Gross Notional Value of Underlying Multi-Sector

Collateralized Debt Obligations That Are Rated Less Than

BBB, Third Quarter of 2008 through Second Quarter of

2009 75

Figure 11: AIG Credit Default Swap Premiums, January 2007

through July 2009 76

Figure 12: AIG Insurance Subsidiaries: Regulatory Capital at

December 31, 2007, and December 31, 2008, and Primary

Activities That Affected Regulatory Capital During 2008

(dollars in millions) 77

Figure 13: AIG Life and Retirement Services: Additions to and

Withdrawals from Policyholder Contract Deposits

Including Annuities, Guaranteed Investment Contracts,

and Life Products, First Quarter of 2007 through Second

Quarter of 2009 79

Figure 14: AIG Life Insurance and Retirement Services: Key

Quarterly Revenues and Expenses, First Quarter of 2007

through Second Quarter of 2009 80

Figure 15: AIG General Insurance: Premiums Written by Division,

First Quarter of 2007 through Second Quarter of 2009 81

Figure 16: AIG Property/Casualty Insurance: AIG Commercial

Insurance Operating Ratios and AIG Foreign General

Insurance Operating Ratios, Second Quarter of 2007

through Second Quarter of 2009 83

Figure 17: FRBNY Revolving Credit Facility Balance Owed and

Total Amount Available, October 2008 through September

2009 86

Figure 18: Principal Owed and Portfolio Values of Maiden Lane

Facilities 87

Figure 19: Proceeds from Dispositions by Quarter, Second Quarter

of 2008 through September 5, 2009 88

Page iii GAO-09-975 Troubled Asset Relief Program

Abbreviations

AGF American General Finance, Inc.

AIA American International Assurance Company, Ltd.

AIG American International Group, Inc.

AIGFP AIG Financial Products Corporation

ALICO American Life Insurance Company

ARRA American Recovery and Reinvestment Act or 2009

CDO collateralized debt obligation

CDS credit default swaps

CPFF Commercial Paper Funding Facility

FDIC Federal Deposit Insurance Corporation

FRBNY Federal Reserve Bank of New York

ILFC International Lease Finance Corporation

NAIC National Association of Insurance Commissioners

OFS Office of Financial Stability

OTS Office of Thrift Supervision

RBC risk-based capital

RMBS residential mortgage-backed security

S&P Standard & Poor’s

SEC Securities and Exchange Commission

SIGTARP Special Inspector General for the Troubled Asset

Relief Program

SPV special purpose vehicle

SSFI Systemically Significant Failing Institutions

TARP Troubled Asset Relief Program

the act Emergency Economic Stabilization Act of 2008

TLGP Temporary Liquidity Guarantee Program

This is a work of the U.S. government and is not subject to copyright protection in the

United States. The published product may be reproduced and distributed in its entirety

without further permission from GAO. However, because this work may contain

copyrighted images or other material, permission from the copyright holder may be

necessary if you wish to reproduce this material separately.

Page iv GAO-09-975 Troubled Asset Relief Program

Page 1 GAO-09-975

United States Government Accountability Office

Washington, DC 20548

September 21, 2009

Congressional Committees:

The United States is experiencing a financial crisis that has threatened the

stability of not only the U.S. banking system but also the U.S. and global

economies and the solvency of a number of critical banks and nonbank

institutions. Consequently, over the past year and a half, the U.S.

government has taken extraordinary measures. The Emergency Economic

Stabilization Act of 2008 (the act) created the Office of Financial Stability

(OFS) within the Department of the Treasury (Treasury) and authorized

the Troubled Asset Relief Program (TARP) to address the crisis.

1

In

addition, Treasury collaborated with the Board of Governors of the

Federal Reserve System (Federal Reserve) to provide government

assistance to institutions it deemed to be systemically significant to avoid

further disruptions in the financial markets that could result from their

failure.

American International Group, Inc. (AIG) is one of the largest recipients of

government assistance. The Federal Reserve and the Federal Reserve

Bank of New York (FRBNY), in consultation with Treasury, initially

provided assistance to AIG in September 2008 following its rating

downgrade, which had prompted collateral calls by its counterparties and

raised concerns that a rapid failure of the company would further

destabilize financial markets. However, AIG’s condition continued to

decline. In November 2008, the Federal Reserve and Treasury announced

plans to restructure AIG’s federal assistance to further strengthen its

financial condition and, once again, avert the failure of the company. In

March 2009, the Federal Reserve and Treasury provided additional

assistance and further restructured the terms of the existing assistance. As

a result of these actions, the federal government has an almost 80 percent

interest in AIG.

1

The Emergency Economic Stabilization Act of 2008 (the act), Pub. L. No. 110-343, 122 Stat.

3765 (2008), codified at 12 U.S.C. §§ 5201 et seq. The act originally authorized Treasury to

purchase or guarantee up to $700 billion in troubled assets. The Helping Families Save

Their Homes Act of 2009, Pub. L. No. 111-22, Div. A, 123 Stat. 1632 (2009), amended the act

to reduce the maximum allowable amount of outstanding troubled assets under the act by

almost $1.3 billion, from $700 billion to $698.741 billion.

Troubled Asset Relief Program

The act requires GAO to provide oversight of actions taken under TARP.

To fulfill our responsibilities, we have been monitoring and providing

timely reporting on Treasury’s assistance to AIG—the largest participant

in TARP and currently the sole participant in TARP’s Systemically

Significant Failing Institutions (SSFI) Program.

2

We testified on the status

of this government effort in March 2009.

3

Because the government

assistance to AIG is a coordinated approach, we are also monitoring the

efforts of the Federal Reserve. Our ability to review the Federal Reserve’s

assistance was recently clarified by the Helping Families Save Their

Homes Act of 2009, enacted on May 20, 2009, which provided GAO

authority to audit Federal Reserve actions taken under section 13(3) of the

Federal Reserve Act for “a single and specific partnership or corporation.”

4

Among other things, this amendment provides GAO with authority to audit

Federal Reserve actions taken with respect to three entities also assisted

under TARP—Citigroup, Inc.; AIG; and Bank of America Corporation. This

amendment also gave GAO the authority to access information from

entities participating in TARP programs, such as AIG, for purposes of

reviewing the performance of TARP.

GAO is required to report at least every 60 days on the activities and

performance of TARP.

5

This 60-day report provides an overview of (1) the

2

Treasury created SSFI to provide capital to institutions on a case-by-case basis to provide

stability and prevent disruption to financial markets caused by the failure of a systemically

significant institution.

3

See GAO, Federal Financial Assistance: Preliminary Observations on Assistance

Provided to AIG, GAO-09-490T (Washington, D.C.: Mar. 18, 2009).

4

Section 801 of The Helping Families Save Their Homes Act of 2009, Pub. L. No. 111-22, Div.

A, 123 Stat. 1632, 1662 (2009), amended the Federal Banking Agency Audit Act, §2, 31

U.S.C. § 714 (2006), which limits GAO’s authority to audit certain Federal Reserve

activities. Specifically, GAO’s audits of the Federal Reserve generally may not include

monetary policy matters, including discount window operations and open market

operations.

5

For our past 60-day reports, see GAO, Troubled Asset Relief Program: Additional Actions

Needed to Better Ensure Integrity, Accountability, and Transparency, GAO-09-161

(Washington, D.C.: Dec. 2, 2008); Troubled Asset Relief Program: Status of Efforts to

Address Transparency and Accountability Issues, GAO-09-296 (Washington, D.C.: Jan. 30,

2009); Troubled Asset Relief Program: March 2009 Status of Efforts to Address

Transparency and Accountability Issues, GAO-09-504 (Washington, D.C.: Mar. 31, 2009);

Auto Industry: Summary of Government Efforts and Automakers’ Restructuring to Date,

GAO-09-553 (Washington, D.C.: Apr. 23, 2009); Troubled Asset Relief Program: June 2009

Status of Efforts to Address Transparency and Accountability Issues, GAO-09-658

(Washington, D.C.: June 17, 2009); and Troubled Asset Relief Program: Treasury Actions

Needed to Make the Home Affordable Modification Program More Transparent and

Accountable, GAO-09-837 (Washington D.C.: July 23, 2009).

Page 2 GAO-09-975 Troubled Asset Relief Program

basis for the Federal Reserve’s and Treasury’s assistance to AIG, (2) the

nature and type of assistance provided to AIG, (3) the steps taken by the

Federal Reserve, FRBNY, and Treasury that are intended to protect the

government’s interest and remaining risks, and (4) the status of federal

assistance and GAO-developed indicators of AIG’s financial condition.

To address the first three objectives—describing both the basis for federal

assistance to AIG and the nature and type of assistance provided to AIG—

we reviewed relevant documents from the Federal Reserve and FRBNY;

recent congressional testimonies on AIG; reports from the Federal

Reserve, FRBNY, Treasury, and the Special Inspector General for the

Troubled Asset Relief Program (SIGTARP); and several GAO reports on

AIG and TARP to obtain information on how the Federal Reserve and

Treasury became involved with AIG, the general goals of the federal

assistance, the nature of the assistance, and how the assistance was

restructured. We also conducted numerous interviews with officials and

staff from the Federal Reserve, FRBNY, Treasury, the National Association

of Insurance Commissioners (NAIC), three state insurance regulators with

major roles in regulating AIG’s insurance companies, two industry

observers, and three rating agencies to understand the government’s

involvement and the condition of the financial markets and the insurance

industry at the time of AIG’s request for assistance. In addition, we

reviewed AIG’s annual and quarterly accounting and financial filings

(10Ks, 10Qs) with the Securities and Exchange Commission (SEC) to

describe the evolving financial condition of AIG and factors affecting AIG’s

financial condition.

6

Furthermore, we reviewed federal laws for

information about the legal framework of the assistance. We also reviewed

studies from NAIC, academics, and rating agencies.

To assess AIG’s financial condition, we developed a set of indicators of

AIG’s financial condition and the status of federal assistance to AIG. We

reviewed reports by several credit rating agencies on how they rate long-

term and short-term debt and financial strength. We also interviewed

officials and staff from the Federal Reserve, Treasury, and AIG about

6

Companies such as AIG that have publicly traded stock listed on the domestic stock

exchanges are required to timely file reports with SEC under the Securities Exchange Act

of 1934. The annual Form 10K gives a comprehensive overview of the company’s business

and financial condition and includes audited financial statements. The quarterly Form 10Q

includes unaudited financial statements and provides a continuing view of the company's

financial position during the year. The Form 8K is the current report companies use to

report certain material corporate events as they occur.

Page 3 GAO-09-975 Troubled Asset Relief Program

possible indicators. No single indicator provides a definitive measure of

AIG’s progress, and indicators should be considered collectively. We

selected indicators that appeared to track the most critical activities

related to the goals for federal assistance to AIG. The resulting indicators

address several dimensions of AIG’s business, including its credit ratings,

operating performance, capital, debt repayment, and liquidity. The data

used to create the indicators came from several sources, but most are

based on publicly available information, such as AIG’s 10K and 10Q filings

and NAIC reports. Specifically, AIG’s SEC filings provided information on

its credit ratings, liquidity, debt, shareholders’ equity, operating income,

credit default swap (CDS) portfolio, collateralized debt obligations

(CDOs), additions to and withdrawals from AIG life and retirement

policyholder contracts, and insurance premiums. In congressional

testimony, AIG provided information about its planned restructuring,

including its divestiture plans and the winding down of its CDS portfolio.

We used Thomson Reuters Datastream to collect information about AIG’s

CDS premiums over time. In addition, NAIC sources provided information

on regulatory capital and primary activities affecting stockholders’ equity

for AIG’s insurance subsidiaries. AIG also provided information on credit

ratings, revenues, and expenditures on AIG’s life and retirement services,

AIG’s property/casualty operation ratios, and AIG business unit

divestitures and asset sales. Rating agencies provided information on

credit ratings. Finally, Federal Reserve reports provided information on

the FRBNY Revolving Credit Facility and the Maiden Lane facilities. We

assessed the reliability of the data and found that the data were

sufficiently reliable for our purposes.

We conducted this performance audit from March 2009 to September 2009

in accordance with generally accepted government auditing standards.

Those standards require that we plan and perform the audit to obtain

sufficient, appropriate evidence to provide a reasonable basis for our

findings and conclusions based on our audit objectives. We believe that

the evidence obtained provides a reasonable basis for our findings and

conclusions based on our audit objectives.

Background

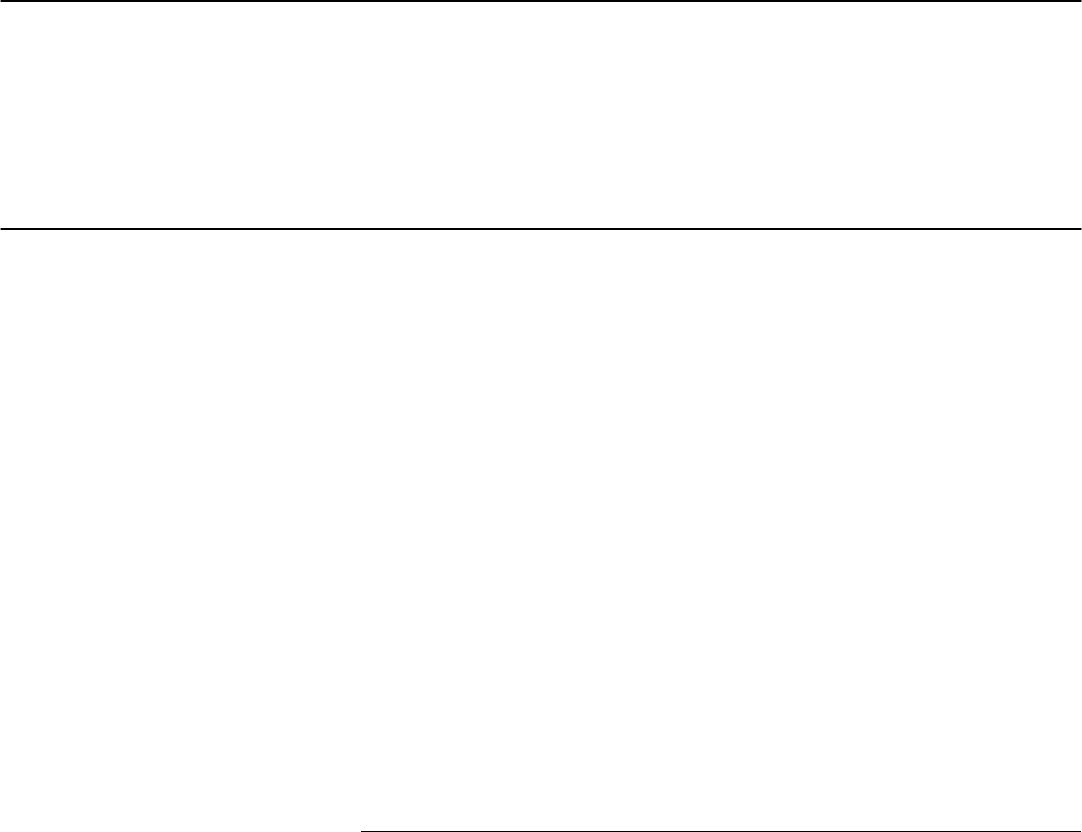

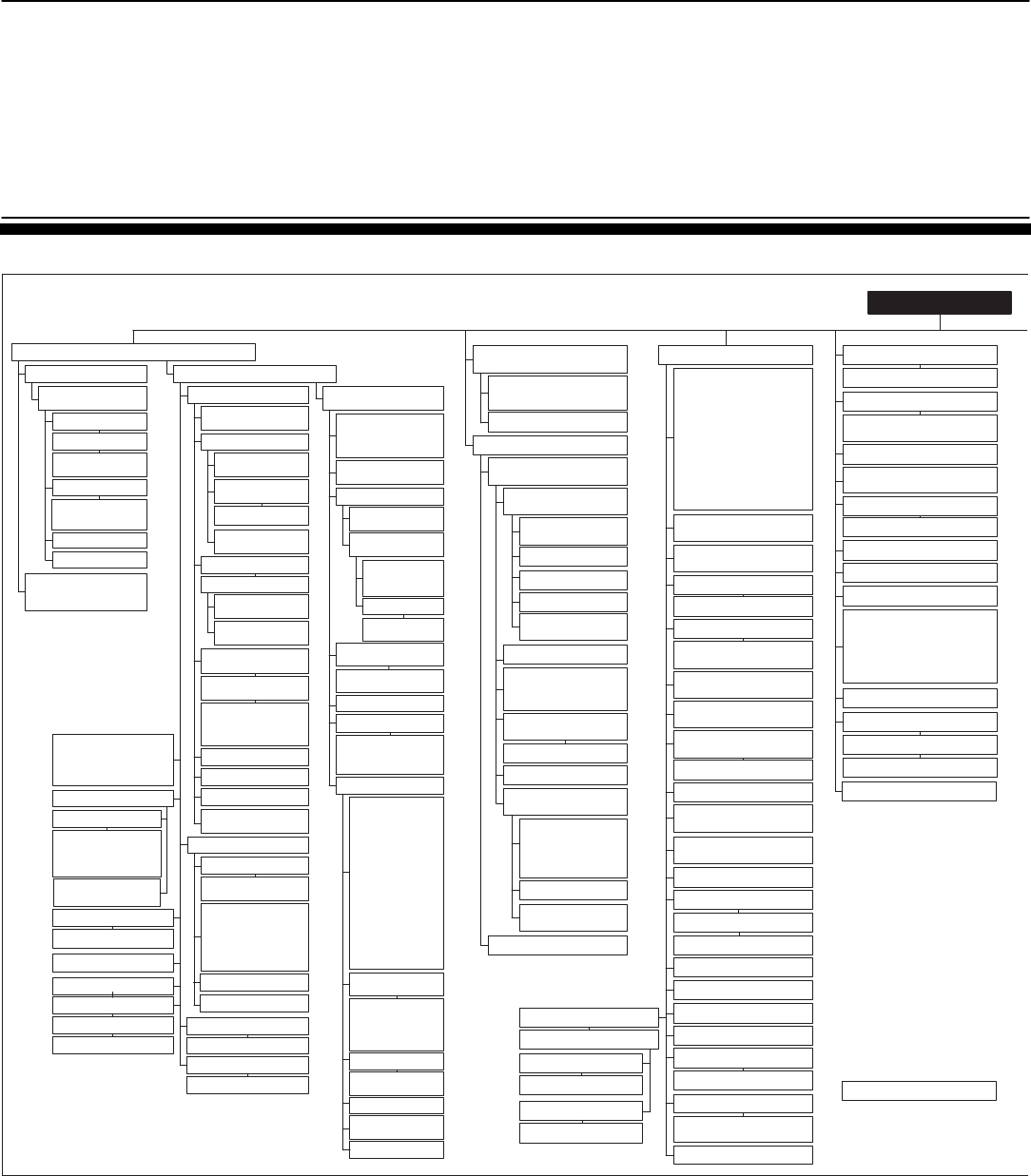

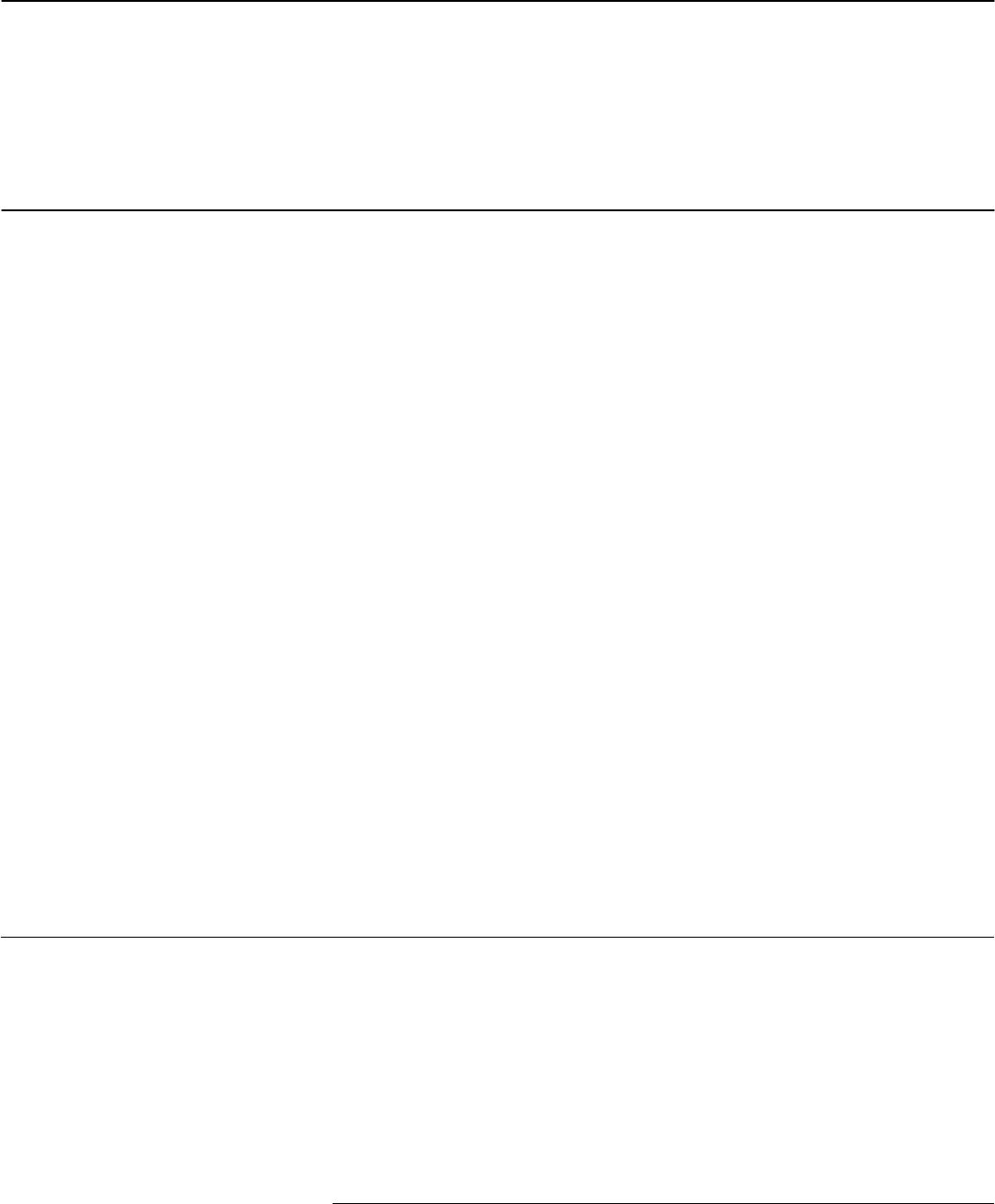

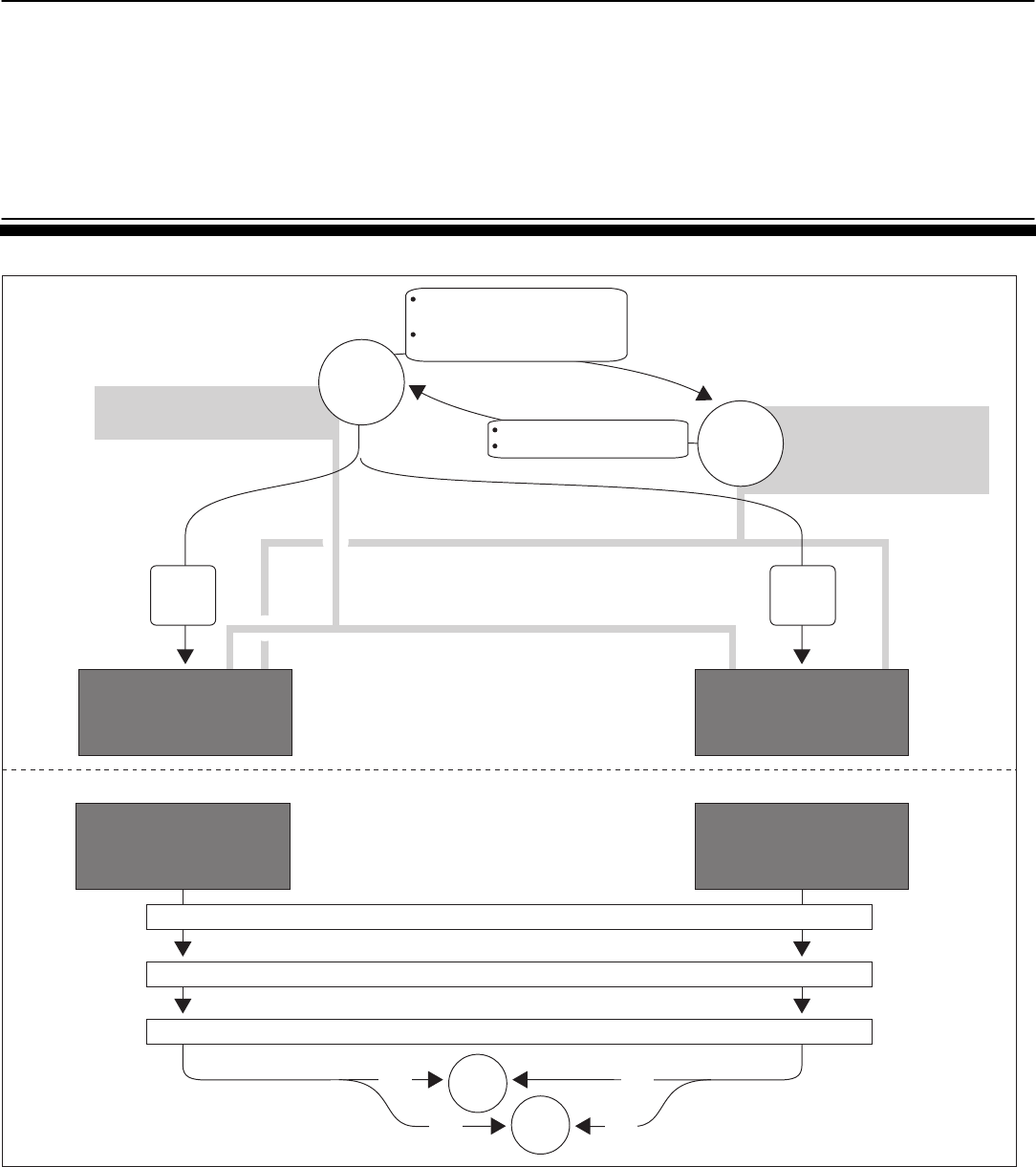

AIG Operations

AIG is a holding company that, through its subsidiaries, is engaged in a

broad range of insurance and insurance-related activities in the United

States and abroad, including general insurance, life insurance and

retirement services, financial services, and asset management. AIG

Page 4 GAO-09-975 Troubled Asset Relief Program

comprises at least 223 companies and has operations in over 130 countries

and jurisdictions worldwide (see fig. 1). As of June 30, 2009, AIG had

assets of approximately $830 billion and $50 billion in revenues for the 6

preceding months, and AIG and its subsidiaries had 106,000 employees.

The AIG organization includes the largest domestic life insurer and the

second-largest domestic and property/casualty insurer in the United

States, and it has a large foreign general insurance business. Figure 1

illustrates the complexity of AIG and its subsidiaries.

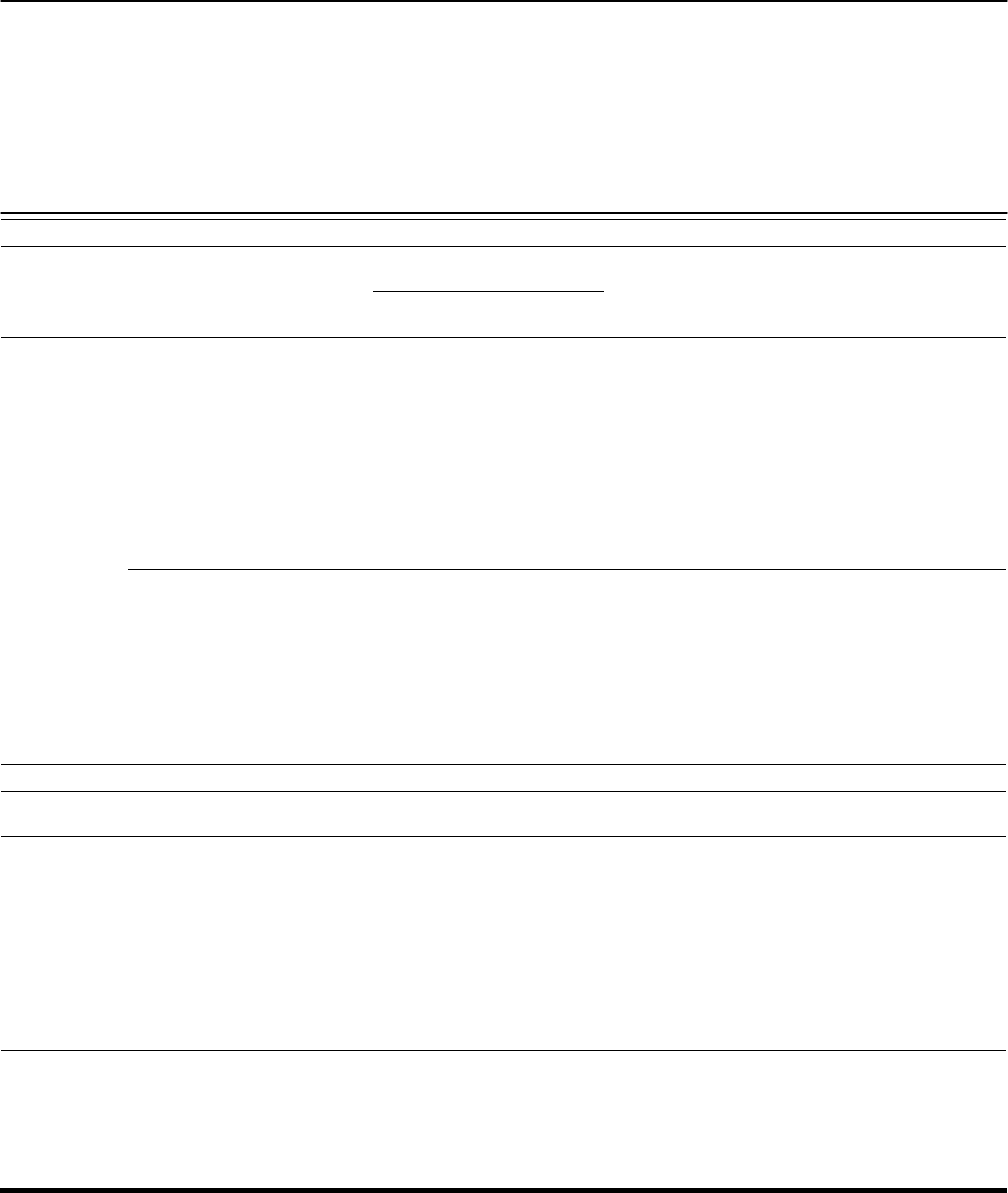

Page 5 GAO-09-975 Troubled Asset Relief Program

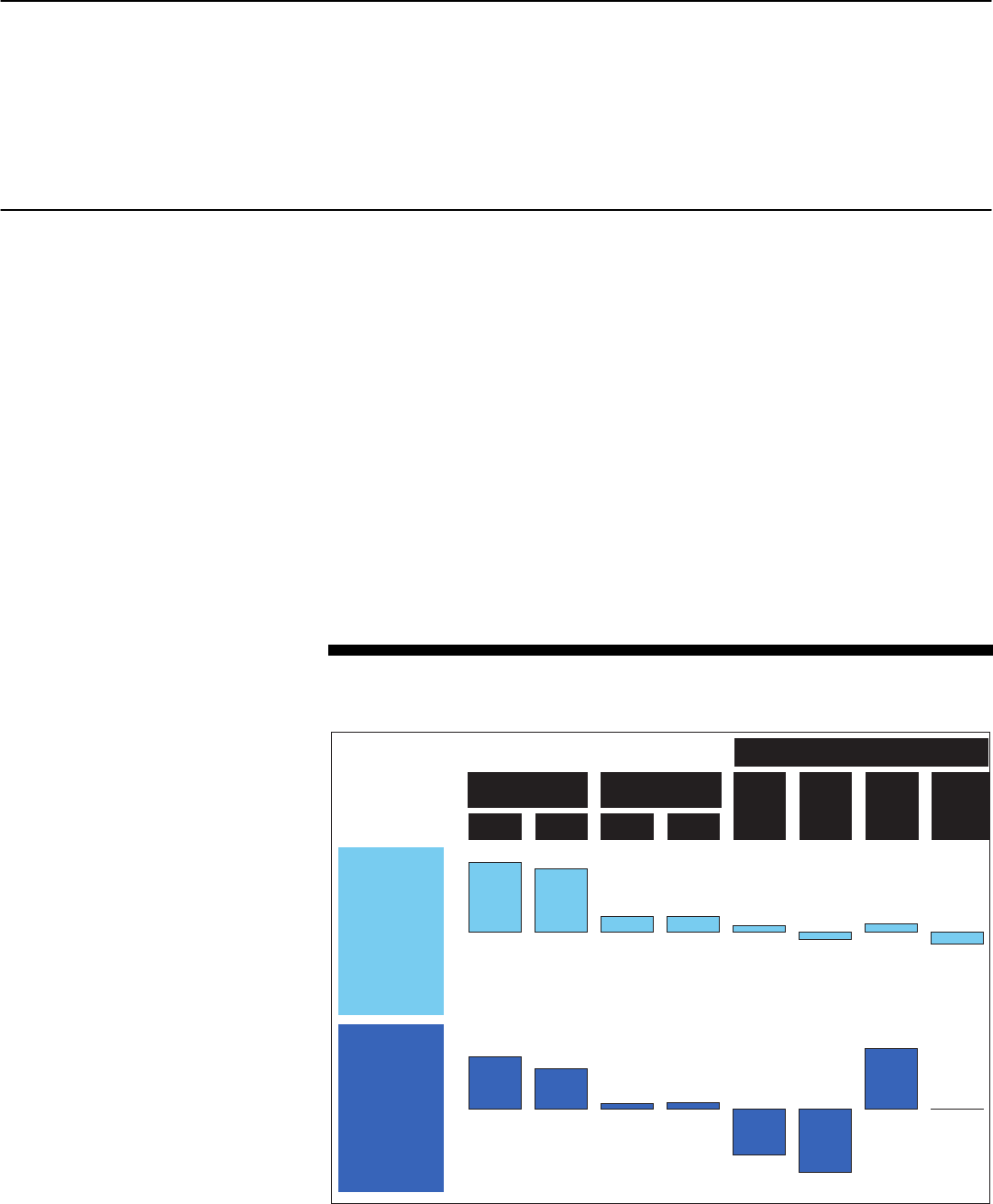

Figure 1: AIG Organizational Structure, as of December 31, 2008

98.5%

AIG

Pol ska

Towarzystwo

Ubezpi eczen

Spol ka

Akcyyjna

100%

National Uni on Fire I nsurance Company

of Pi ttsburgh, Pa.

100%

National Uni on Fire I nsurance

Company of L ouisiana

National Uni on Fire I nsurance

Company of V ermont

AIG Domestic Claims, I nc.

50%

JI

Accident & Fire Insurance

Company, Ltd.

70%

Lexington Insurance Company

N

100%

AIG Auto Insurance Company

of New Jersey

AI G Preferred I nsurance

Company

100%

AIG Indemnity Insurance

Company

100%

AIG Centenni al Insurance

Company

100%

AIG Premier Insurance Company

70%

American International Speci alty

Lines Insurance Company

N

100%

AIG Lodgi ng Opportunities, Inc.

100%

AIG

Excess Liability Insurance International

Limited

75%

American I nternational Insurance Company

100%

AIG Advantage Insurance Company

American I nternational Insurance Company

of California, Inc.

American I nternational Insurance Company

of New Jersey

B

C

American International Group, Inc.

100%

21st

Century Casualty Company

21st

Century Insurance Company

21st

Century Insurance Company of the

Southwest

100%

AIG Excess Liability Insurance

Company Ltd.

100%

Global Standards,

LLC

100%

The Hartford Steam Boiler Inspection

and Insurance Company

of Connecticut

100%

EIG

, Co.

100%

HSB

Engineeri ng Insurance Li mited

100%

The Boiler Inspection and Insurance

Company of Canada

100%

United Gua ranty Commercial

Insurance Company of North Carolina

United Gua ranty Credit

Insurance Company

United Gua ranty Mortgage

Indemnity Company

100%

A.I.G.

Mortgage Holdings Israel, Ltd.

45.88%

United Gua ranty Corporation

P

100%

E.M.I .

-

Ezer

Mortgage Insurance

Company Ltd.

100%

AIG

Centre

Capital Group, Inc.

AIG Mortgage Risk Sol utions

Pt y

Ltd.

AIG United Guaranty

Agenzia

di

Assicurazione

S.R.L.

AIG United Guaranty Insurance

(Asia) Limited

AIG United Guaranty Mortgage

Insurance Company Canada

AIG United Guaranty Re, Ltd.

AIG United Guaranty,

Soci edad

Limitada

United Gua ranty Direct Insurance

Ser v i ces, Inc.

United Gua ranty Services, Inc.

United Gua ranty Insurance Company

United Gua ranty Mortgage Insurance

Company

United Gua ranty Mortgage Insurance

Company of North Carolina

United Gua ranty Partners Insurance

Company

United Gua ranty Residential

Insurance Company of North Carolina

65.93%

Educational Loan Ser v i ci ng ,

LLC

100%

Ra-Hart Investment Company

100%

HSB

Prof essional Loss Control , Inc.

75.03%

United Gua ranty Residential Insurance

Company

100%

Transatlantic Reinsurance Company

33.24%

Transatlantic Holdings, Inc.

100%

Putnam

Reinsurance Company

Trans Re Zurich

100%

American Home A ssurance Company

100%

American Pacific Insurance Company,

Inc.

93.33%

AIG Hawai i Technol ogy Solutions,

LLC

D

99.88%

AIG Hawaii

LTC

Solutions,

LLC

E

100%

AIG Hawaii Insurance Company, Inc.

100%

AIG Non-Life Holding Company (Japan),

Inc.

19.8%

Fuji Fire & Marine Insurance Company

Limited

100%

American Fuji Fire & Marine Insurance

Company

Fuji Life Insurance Company, Li mited

Fuji International Insurance Company,

Limited

100%

New Hampshi re Insurance Company

100%

New Hampshi re Indemnity Company, Inc.

100%

AIG National Insurance

Company, Inc.

100%

AI Network of Nevada, Inc.

American International Pacif ic

Insurance Company

American International South

Insurance Company

Granite State Insurance Company

Illinois National Insurance Co.

New Hampshi re Insurance Ser vi c es, Inc.

G

100%

Audubon Insurance Company

100%

Agency Management Corporation

100%

Audubon Indemnity Company

100%

The Gulf Agency, Inc.

F

100%

AIG General Insurance (Malaysia)

Berhad

100%

LSP

Holdings

LLC

100%

A100

LLC

100%

HSB

Group, Inc.

100%

The Hartford Steam Boiler Inspection and

Insurance Company

100%

American International Insurance Company of

Delaware

A.I.G.

Managi ng General Agency, I nc.

AIG Marketing, Inc.

100%

AIG Commercial Insurance Group, Inc.

100%

AIG Property Casualty Group, Inc.

100%

The Insurance Company of the

State of Pennsylvania

Landmark Insurance Company

AIG Casualty Company

AIG Commercial Insurance

Company of Canada

32.09%

21st

Century Insurance Group

O

100%

Commerce and Industry Insurance Company

13.76%

Eastgreen

, Inc.

99.96%

United Gua ranty

Ser v i ci os

Administrativos

, S. de

R.L.

de

C.V.

R

H

100%

AIG Aviation, Inc.

31.5%

American International Realty

Corp

.

I

100%

AIG

LS

Holdings

LLC

100%

AIG Life Set t l ement s

LLC

31.47%

Pi ne Street Real Estate Holdings

Corp

.

J

Q

40%

Kuwait

Reinsurance Company

(

K.S.C

)

99.999%

AIG United Guaranty Mexico,

S.A.

100%

AIG Hawaii Technologies, Inc.

19.72%

AIG

Metropol itana

Compani a

de

Seg uros

y

Reaseguros

S.A.

100%

A.I.

Risk Specialists Insurance, Inc.

100%

Risk Specialists Compani es, Inc.

K

S

60.96%

P.T.

Asuransi

AIU

Indonesia

100%

Morefar

Marketing, Inc.

80%

P.T.

AIG Life

100%

Union Excess Reinsurance Company, Ltd.

100%

American Life Insurance Company

100%

AIG

Hayat

Sigorta

A.S.

AIG Life (Ireland) Limited

AIG Life (Bulgaria)

ZZD

,

EAD

AIG Life

Asigurari

Romania

SA

AHICO

Elso

Amerikai

Magyar

Biztosito

Zrt

..

American Life Insurance Company

Gestora

de

Fondos

y

Pl anos

de

Pensiones

S.A.

ALICO

S.A.

ALICO

Compania

de

Seguros

de

Vida

S.A.

ALICO

Properties Inc., II

AIG Management (UK) Limited

Fondos

y

Pl anos

de

Pensiones

S.A.

First American Czech Insurance Company,

A.S.

International Investment Holding

Company Li mited (Russ ia)

Zeus Administration Ser vi c es Limited

AMSLICO

AIG Life

poist'ovna

a.s.

61.84%

American Life Insurance Company (Pakistan)

Limited

80.92%

American L ife and General Insurance Company

(Trinidad and Tobago) Ltd.

92.7853%

Seguros

Venezuel a,

C.A.

50%

Inversiones

Inverseg ven

,

C.A.

99.99%

Inversi ones

Interameri cana

S.A.

BB

100%

La

Interameri cana

Compania

de

Seguros

de

Vida

S.A.

90%

Alico

Compania

de

Seguros

de

Retiros

ALICO

Compania

de

Seguros

S.A.

100%

First American Polish Life Insurance and

Reinsurance Company

S.A.

74.875%

Pharaoni c

American L ife Insurance Company

27.5%

Hellenic

ALICO

Life Insurance Company Ltd.

99.99%

CJSC

American L ife Insurance

Company AIG Life

GG

100%

AIG Financi al Assurance Japan

K.K.

40%

UBB

-AIG Life Insurance Company

JSC

60%

IBCO

Gestao

de

Patrimonios

,

S.A.

100%

Phi l am

Insurance Company, Inc.

Phi l am

Plans, Inc.

Pacific Union Assurance Company

99.78%

The

Philippine

American L ife &

General Insurance Company

95%

Phi l am

Equitable Life Assurance Company, Inc.

W

100%

American I nternational Reinsurance Company,

Ltd.

100%

American International Assurance Company

Ltd.

60.96%

P.T.

Asuransi

AIA

Indonesia

100%

AIG Life Holdings (International)

LLC

49%

AIG Mexico

Seguros

Interameri cana

,

S.A.

de

C.V.

100%

AIG-

Cuidando

tu

Salud

,

S.A.

de

C.V.

100%

American I nternational Assurance

Company (Bermuda) Ltd.

100%

AIG Life Insurance (Vietnam)

Company Limi ted

AIG Globa l Investment Corporation

(Asia) Ltd.

AIA

(Bermuda) Ser vi c es, Inc.

Grand Design Development Limited

26%

Tata

AIG Life Insurance

Company Ltd.

100%

AIG Star Life Insurance Co., Ltd.

50%

AIG

Pow szechne

Towarzystwo

Emerytalne

S.A.

100%

Equitable Investment Co. (Hong Kong) Ltd.

100%

SEA Insurance Co. Limited

SEA Insurance

Sendi r i an

Berhad

50.01%

AIG Israel Insurance Company Ltd.

99.99%

La

Interameri cana

Compania

de

Seguros

Generales

S.A.

(Chile)

100%

Caravan Investment Inc.

51%

AIG Caspi an Insurance Company

49%

AIG Ukraine

100%

AIG Globa l Serv i ces, Inc.

100%

American I nternational Group

KK

15%

Rus s ian Reinsurance Company

OAO

51%

Uzbek

American I nsurance Company

100%

AIG Life International

Ltd.

American I nternational Assurance

Company (Australia) Ltd.

AIRCO

Finance Co. Ltd.

26%

Prime Property

Y.K.

100%

Gemini Property

Y.K.

NN

100%

AIU

North America, Inc.

AIG Federal Savings Bank

AIG Funding, Inc.

AIG Castle Holdings

LLC

AIG Castle Holdings II

LLC

AIG Life Insurance Company (Switzerland), Ltd.

American Security Life Insurance Company, Ltd.

Delaware American Life Insurance Company

100%

AIG

Pr i vat

Bank

AG

100%

AIG Trading Group, Inc.

100%

AIG International, Inc.

Y

MM

95.27%

Nan

Shan

Life Insurance Company, Ltd.

100%

AIG Vita

S.p.A.

95%

Agenvita

S.r.l.

20%

Prime Ocean

YK

AA

100%

Borderland Investments Limited

100%

AIG Life

Hellas

Represen tation and Consulting

Ser vi c es

50%

ALICO

AIGE

,

A.I.E.

60%

AIG

Kazakhstan

Insurance Company,

S.A.

100%

ZAO

"Master D"

51%

CJSC

AIG Life Insurance Company (Russia)

100%

ALICO

European Holdings Limited (Ireland)

99.99%

AIG Mexico,

Compania

de

Seguros

de

Vida

,

S.A.

de

C.V.

94.99%

AIG Colombia

Seguros

de

Vida

,

S.A.

99.99%

AIG Life

Osiguranje

A.D.O.

Beograd

100%

American I nternational Assurance

Bhd

LC

Ventura (

Tampines

)

Pt e

Ltd

64.55%

Metropol itan Land Company, Limited

100%

Virgo Property

YK

49%

P.C.

-

AIA

Co. Ltd.

84%

American I nternational Data

Centre

Limited

100%

AIG Clearing Corporation

T

U

V

LL

90%

ALICO

AIG Mutua l Fund Management Company

S.A.

CC

DD

EE

FF

BB

HH

II

JJ

KK

10%

AIG Edison Life Insurance Company

X

40%

American International Company, Limited

Z

Page 6 GAO-09-975 Troubled Asset Relief Program

Troubled Asset Relief ProgramTroubled Asset Relief Program

Page 7 GAO-09-975

100%

HPIS

Limited

100%

AIG Gl oba l Real Estate Investment

Corp

.

2%

AIG Mexico Indus trial I,

L.L.C.

100%

AIG Capi tal Corporation

E

100%

AIG Central Europe &

CIS

Insurance Holdings

Corporation

100%

AIG Bulgaria Insurance Company

EAD

AIG Czech Republic

pojistovna

,

a.s.

AIG Romania Insurance Company

S.A.

100%

AIU

Africa Holdings, Inc.

80%

AIG

Hayleys

Investment Holdings

(Private) Ltd.

100%

AIG

MEMSA

Holdings, Inc.

26%

Tata

AIG General Insurance

Company Limited

100%

AIG Lebanon

S.A.L.

AIG

Sigorta

A.S.

66.67%

AIG Kenya Insurance Company, Li mited

100%

AIU

Holdings

LLC

40%

UBB

-AIG Insurance and Reinsurance

Company

JSC

100%

AIG Global Investment

Corp

.

AIG Ports America, Inc.

AIG Securities Lending

Corp

.

100%

AIG Gl oba l Asset M anagement

Holdings

Corp

.

100%

AIG Consumer Finance Group, Inc.

99.92%

AIG Bank

Pol ska

S.A.

99.15%

AIG Retail Bank

Public Company Li mited

100%

AIG Consumer Finance Group

(Asia) Limited

Compani a

Financiera

Argentina

S.A.

67.23%

International Lease Finance Corporation

100%

AIG Finance Holdings, Inc.

100%

AIG Finance (Hong Kong), Li mited

G

100%

A.I.

Credit

Corp

.

100%

AIG Credit

Corp

.

100%

AIG Equipment Finance Holdings, Inc.

100%

AIG Commercial Equipment Finance, Inc.

AIG Rail Services, Inc.

100%

AIG

Retirement Ser v i ces,

Inc.

100%

SunA merica

Life Insurance Company

100%

AIG

SunA merica

Life Assurance Company

100%

AIG

SunA merica

Asset M anagement

Corp

.

100%

SunA merica

(Cayman) Insurance

Company, Ltd.

100%

SunA merica

Investments, Inc.

100%

AIG Advisor Group, Inc.

100%

First

SunA merica

Life

Insurance Company

SA

Affordable Housing,

LLC

33%

New California Life Holdings, Inc.

100%

Advantage Capital Corporation

American General Sec urities

Incorporated

Financial Service Corporation

Royal Alliance Associ ates, Inc.

SagePoi nt

Financial Advisors, Inc.

100%

American International Underwriters Overseas,

Ltd.

100%

AIG

Ireland Limi ted

AIG General Insurance (Thailand) Ltd

AIG General Insurance (Vi etnam)

Company Limited

AIG

Memsa

Insurance Company Ltd.

AIG

ReInsurance

Ser vi c es Office

AIG

Takaful

-

Enaya

B.S.C.

AIG Uganda Limited

AIG Urugua y

Compania

de

Seguros

S.A.

American Asiatic Underwriters, Limited

Amer ican Inter nati

onal Insurance Company

of Puerto Rico

American International

Under writ

er s

Over seas,

I.I.

Ameri can Inte

rnational Underwriters de

Colombia,

Lt

da

.

A

meric

an International

Under w

rit

ers

(Phi lippines

),

Inc.

Arabian American Insurance

Company (Bahrain)

E.C.

Informatica

y

Servicios

LA

T

EC

,

S.A.

S.

J

.

Zevlaris

Insurance Agency Co. Limited

Underwriters Adj

ustment Company, Inc

[Panama]

99.93%

La

Meridional

Compani a

Argentina de

Seg uros

S.A.

100%

Hayleys

AIG Insurance Company Ltd.

100%

AIG European Insurance Investments Inc.

100%

Ascot Corporate Name Limited

100%

Joh annesburg Insurance Holdings (

Pt y

)

Limited

100%

AIG Life South Africa Limited

AIG South Africa Limited

50%

Hellas

Insurance Co.

S.A.

20%

Uzbek i nv est

International Insurance

Company Li mited

50%

Inversi ones

Seg ucasai

,

C.A.

93.38%

C.A.

de

Seg uros

American International

95.02%

AIG

Brasil

Companhi a

de

Seg uros

S.A.

100%

Richmond Insurance Company

(Barbados) Ltd.

100%

Richmond Insurance Company Li mited

20.1%

El

Pacif ico

-

Per ua no

Suiza

Compani a

de

Seg uros

S.A.

61.99%

El

Pacif ico

Vida

Compani a

y

Reaseguros

C

100%

AIG Realty, Inc.

AIG Gl oba l Real Estate Asia

Pacific, Inc.

100%

Sierra Leasing Ltd.

100%

Aircraft

SPC

-9, Inc.

100%

Aircraft

SPC

-12, I nc.

100%

Whitney Leasing Limited

100%

AIU

Latin America Investments,

LLC

85.02%

Garanpl us

S.A.

de

C.V.

61.75%

AIG UK Holdings Ltd.

100%

AIG UK Financi ng Limited

100%

AIG UK Sub Holdings Limited

100%

AIG (UK) Limited

100%

AIG UK Ser v i ces Limited

100%

AIG

Germany Holding

GmbH

100%

Wurttember ger i sche

und

Badi sche

Versicherungs

-

AG

100%

DARAG

Deutsche

Versicherungs

-

und

Ruckversicherungs

-

Aktiengesel l schaft

A

100%

American General Finance, Inc. [IN]

100%

American General Financi al Serv i ces

of America, Inc. [DE]

100%

American General Home

Equity, Inc. [DE]

100%

American General Consumer

Discount Company

American General Financi al

Ser v i ces of Illi nois, Inc.

American General Financi al

Ser v i ces, Inc. [DE]

American General Financi al

Ser v i ces, Inc. [IN]

American General Financi al

Ser v i ces, I nc.[NC]

American General Financi al

Ser v i ces, Inc. [OH]

American General Financi al Serv i ces,

Inc. [SC]

American General Financi al

Ser v i ces, Inc. [TX]

American General Financi al

Ser v i ces, Inc. [WA]

Merit Life Insurance Co.

Ocean Finance and Mortgages Limited

Yosemite Insurance Company

100%

American General Finance Corporation [IN]

100%

American General Finance Services of

Alabama, Inc.

100%

MorEquity

, Inc. [NV]

100%

Wilmington Finance, Inc.

100%

AIU

Far East Insurance Holdings, Inc.

100%

AIU

Far East Holdings,

KK

35%

AIP

KK

94%

A.I.G.

Colombia

Seg uros

Generales

S.A.

100%

AIU

Insurance Company

100%

AIG General Insurance Company

China Limited

AIG General Insurance (Taiwan) Co., Ltd.

100%

UNAT

Direct Insurance

Management Limited

10%

Inversora

Pi ch i nch a

S.A.

Compani a

de

Financiami ento

Comercial

100%

AIG Holding A ndes 1, Inc

50%

Globa l Information Ser v i ces Ltd.

100%

Hospital Plan Insurance Ser v i ces

100%

AIG Travel, Inc.

99.99%

AIG

Seg uros

de Personas,

S.A.

99.99%

AIG Union

y

Desarrollo

,

S.A.

94.98%

AIG Egypt Insurance Company

S.A.E.

100%

SunA merica

Capital Services, Inc.

100%

American International Underwriters Corporation

B

D

F

51%

AIG

Uzbek i nv est

Limited

50%

Latin American Investment Gua rantee

Company, Ltd.

100%

AIG Gl oba l Trade & Political Risk

Insurance Company

100%

La

Seg uridad

de

Centroamerica

,

Compani a

de

Seg uros

S.A.

98.33%

La

Seg uridad

de

Centroamerica

,

Compani a

de

Fianzas

,

S.A.

T

99%

AIG Insurance (Guer nsey )

PCC

Limited

U

100%

Pacif ico

S.A.

Empresa

Pr estadora

de

Salud

V

99%

AIG Insurance (Guer nsey )

PCC

Limited

67%

AIG

General Insurance (Malaysia)

Berhad

W

100%

ZAO

AIG Insurance &

Reinsurance Company

AIG Europe (Netherlands)

N.V.

91.32%

AIG Europe,

S.A.

2.72%

AIG Europe Holdings Limited

X

100.00%

AIG Luxembourg Financi ng Limited

.

Y

100%

AIG Life Holdings (US), Inc.

100%

AGC

Life Insurance Company

100%

American General Life and Acci dent

Insurance Company

100%

AIG Life of Bermuda, Ltd.

100%

AIG Worldwide Life Insurance of

Bermuda, Ltd.

100%

American General Life Insurance

Company

100%

American General Property

Insurance Company of Florida

100%

AI Life Settlement, I nc.

American General

Bancassurance

Ser vi ces, Inc.

Knickerbocker

Corporation

100%

American General Property

Insurance Company

100%

AIG Life Holdings

(Canada),

ULC

100%

AIG Assurance Canada

100%

Rokl and

Limited

100%

American General Annuity Ser v i ce

Corporation

AIG Enterpri se Ser v i ces,

LLC

American General Equity Serv i ces

Corporation

American General Life Companies,

LLC

The Variable Annuity Life

Insurance Company

Pi ne Vermont Rei nsurance Company

100%

Volunteer Vermont Holdi ngs,

LLC

Volunteer Vermont Reassurance

Company

100%

AIG Financial Products

Corp

.

79%

Sorbier

Holding

Corp

.

90%

Banque

AIG

S.A.

100%

NF

One Hundred and Twenty-Three

Corp

.

100%

Applewood

Funding

Corp

.

AIG Energy, Inc

AIG Financi al Products (Australia) Ltd.

AIG Matched Fundi ng

Corp

.

AIG-

FP

Matched Funding

Corp

.

AIG-

FP

Private

Fudi ng

Corp

.

AIG-

FP

Private Funding (Cayman) L imited

Bi gnonne

Investments One

LLC

Bluew ood

Investment

LLC

DBY

One,

LLC

Hickory Holding

Corp

.

International Investment Company

(Bermuda) Limited

LSP

Senior Lendi ng

LLC

Orangewood

Investments

LLC

Yellowwood

Investment

LLC

100%

AIG-

FP

Pi nestead

Holidngs

Corp

.

100%

Albert i

Holding Company

Cedarstead

Investment

Corp

.

Pi nestead

Investment

Corp

.

Willowgrove

Finance Company L imited

100%

AIG-

FP

Pi nestead

Hol idng

III

Corp

.

100%

AIG-

FP

Investment Company (Bermuda) Limited

100%

AIG-

FP

Fundi ng (Cayman) Li mited

AIG-

FP

Special Finance (Cayman) L imited

NF

Thirteen (Cayman) L imited

100%

AIG-

FP

Capital Preserv ation

Corp

.

91%

Bullfinch Investments (Cayman) L imited

100%

Bittern Investments

Corp

.

100%

Flamebright

Investment Limited

100%

AIG Financial Products (Jersey) L imi ted

100%

Dukes

Corp

.

100%

Cloudview

(Cayman)

Limted

Skyview

(Cayman) Limi ted

Skyview3

(Cayman) Limi ted

100%

Stonel and

Limited

100%

Peachwood

Funding

Corp

.

100%

Peachwood

LLC

100%

Swallow Investments

LLC

100%

Brambling

Investments

LLC

100%

Pearwood

Fundi ng

Corp

100%

Pearwood

LLC

100%

Sorbier

Investment

Corp

.

79%

Lakevista

Holdings

Corp

.

21%

Lakevista

Corp

.

100%

AIG-

FP

Holdings

Corp

.

100%

TMS

Investments

LLC

100%

TMS

Sub

LLC

100%

Clarges

Fundi ng

LLC

79%

NF

Fifty-Eight

Corp

.

21%

Heathwood

Holding

Corp

.

100%

Heathwood

Corp

.

100%

AIG-

FP

Structured Finance (Cayman) Limi ted

H

I

J

M

O

P

Q

100%

AIG Life Insurance Company

of Canada

25.294%

Spi cer

Energy II

LLC

100%

Ambler Holding

Corp

.

R

100%

American General Assurance Company

100%

American General Indemnity Company

99%

AIGFP

NZ

Funding

LLC

100%

Avon Holdings

Corp

100%

Avon

LLC

100%

Avon Financi ng

Corp

.

10%

Elgibright

Investment Limited

100%

Nerine

Finance No. 3

100%

Highfield

Holding

Corp

.

100%

Highfield

LLC

99%

C

herrywood

Investments

LLC

K

100%

AIG Annuity Insurance Company

AIG Life Insurance Company

American International Life Assurance

Company of New York

The Uni ted States Life Insurance Company

in the City of New York

44%

Iris Energy,

LLC

L

S

N

Source: Schedule Y of the 2008 Annual Statements filed by AIG's insurance companies with NAIC.

Page 7 GAO-09-975

AIG was a large issuer of commercial paper, a mortgage lender, and

through AIG Financial Products Corporation (AIGFP)—a financial

products subsidiary that engaged in a variety of financial transactions,

including standard and customized financial products—a participant in the

derivatives market.

7

AIGFP has been a key source of AIG’s financial

difficulties. As of June 30, 2008, AIG’s business included an estimated $15

billion of outstanding commercial paper and the company sold CDS with

$447 billion gross notional exposure on CDOs.

8

Additionally, AIG

maintained a large securities lending program operated by its insurance

subsidiaries. The securities lending program allowed insurance

companies, primarily the life insurance companies, to lend securities in

return for cash collateral that was invested in residential mortgage-backed

securities (RMBS). This program was another major source of AIG’s

liquidity problems in 2008.

Aspects of AIG and its subsidiaries are regulated by federal and state

authorities. The Office of Thrift Supervision (OTS) is the consolidated

supervisor of AIG, which is a thrift holding company by virtue of its

ownership of AIG Federal Savings Bank. As the consolidated supervisor,

OTS is charged with identifying systemic issues or weaknesses and

ensuring compliance with regulations that govern permissible activities

and transactions.

9

In recent testimony, OTS said that it supervised and

assessed AIG as a conglomerate and communicated with other functional

regulators and supervisors that share jurisdiction over portions of the

conglomerate.

10

AIG’s domestic and life and property/casualty insurance

companies are regulated by the state insurance regulators in which these

companies are domiciled.

11

These state agencies regulate the financial

solvency and market conduct of these companies within their states and

7

Corporations primarily issue commercial paper, which are short-term promissory notes.

8

CDS are bilateral contracts that are sold over the counter and transfer credit risks from

one party to another. The seller, who is offering credit protection, agrees, in return for a

periodic fee, to compensate the buyer if a specified credit event, such as default, occurs.

CDOs are securities backed by a pool of bonds, loans, or other assets.

9

GAO, Financial Market Regulation: Agencies Engaged in Consolidated Supervision Can

Strengthen Performance Measurement and Collaboration, GAO-07-154 (Washington, D.C.:

Mar. 15, 2007).

10

See testimony of Scott M. Polakoff, Acting Director, Office of Thrift Supervision, before

Subcommittee on Capital Markets, Insurance, and Government Sponsored Enterprises,

House Committee on Financial Services, March 18, 2009.

11

The primary state insurance regulators include New York, Pennsylvania, and Texas.

Page 8 GAO-09-975 Troubled Asset Relief Program

they have the authority to approve or disapprove certain transactions

between an insurance company and its parent or its parent’s subsidiaries.

These agencies also coordinate the monitoring of companies’ insurance

lines among multiple state insurance regulators. For AIG in particular,

these regulators have reviewed reports on liquidity, investment income,

and surrender and renewal statistics; evaluated potential sales of AIG’s

domestic insurance companies; and investigated allegations of pricing

disparities.

In addition, Treasury’s purchase, management, and sale of assets under

TARP, including those associated with AIG, are subject to oversight by

SIGTARP. As part of its quarterly reports to Congress, SIGTARP has

provided information on federal assistance and the restructuring of the

federal assistance provided to AIG, as well as information on the

unwinding of AIGFP and the sale of AIG’s assets.

12

Recently, we and

SIGTARP have initiated a coordinated review of the federal governance

over institutions such as AIG where the government has provided

extraordinary assistance and has a significant ownership interest. The key

focus of this review includes the extent of government involvement in

management of such companies and the extent to which effective risk

management, internal controls, and monitoring are in place to protect and

balance the government’s interests in relation to corporate needs.

Overview of the Federal

Reserve’s and Treasury’s

Authorities

The Federal Reserve and Treasury provided assistance to AIG under the

following authorities:

• Section 13(3) of the Federal Reserve Act.

13

This provision allows the

Federal Reserve, in “unusual and exigent circumstances,” to authorize any

Federal Reserve Bank to extend credit in the form of a discount to

individuals, partnerships, or corporations when the credit is “indorsed or

otherwise secured” to the satisfaction of the Federal Reserve Bank, after

obtaining evidence that the individual, partnership, or corporation is

unable to secure adequate credit accommodations from other banking

institutions. The Federal Reserve has used this emergency authority in

12

SIGTARP: Office of the Inspector General for the Troubled Asset Relief Program,

Quarterly Report to Congress, July 21, 2009; SIGTARP: Office of the Inspector General for

the Troubled Asset Relief Program, Quarterly Report to Congress, April 21, 2009;

SIGTARP: Office of the Inspector General for the Troubled Asset Relief Program, Initial

Report to the Congress, February 6, 2009.

13

Section 13(3) of the Federal Reserve Act, as amended, codified at 12 U.S.C. § 343 (2006).

Page 9 GAO-09-975 Troubled Asset Relief Program

support of the government’s efforts to stabilize systemically significant

financial institutions, including AIG, and this is the same authority used for

various other Federal Reserve actions in the ongoing financial crisis.

• Emergency Economic Stabilization Act of 2008.

14

The act authorized

Treasury to establish TARP and to implement the program through a new

Office of Financial Stability within Treasury. Among other things, the act

grants Treasury broad, flexible authorities to purchase and insure troubled

assets from financial institutions. The act defines troubled assets to

include residential or commercial mortgages and securities based on such

mortgages. Troubled assets may also include any other financial

instrument (e.g., equities) that the Secretary of the Treasury, after

consultation with the Chairman of the Federal Reserve, determines is

necessary to purchase to promote financial market stability.

• The American Recovery and Reinvestment Act of 2009 (ARRA).

15

Provisions of this act amend and restate the executive compensation and

corporate governance provisions of the act.

The Federal Reserve and Treasury determined through analysis of

information provided by AIG and insurance regulators, as well as publicly

available information, that market events in September 2008 could cause

AIG to fail, which would pose systemic risk to financial markets.

16

Consequently, the Federal Reserve and Treasury took steps to ensure that

AIG obtained sufficient liquidity and could complete an orderly sale of its

operating assets, continue to meet its obligations, and close its investment

positions in its securities lending program and AIGFP. The Federal

Reserve explained that a major concern was public confidence in the

financial system and the economy. The Federal Reserve and Treasury said

that financial markets and financial institutions were experiencing

The Federal Reserve

and Treasury

Provided Assistance

to AIG to Limit

Systemic Risk to the

Financial Markets

14

Pub. L. No. 110-343, 122 Stat. 3765 (2008).

15

Pub. L. No. 111-5, Div. B, Title VII, 123 Stat. 115, 516 (2009).

16

As we said in our March 2009 testimony on credit default swaps, there is no single

definition for systemic risk. Traditionally, systemic risk was viewed as the risk that the

failure of one large institution would cause other institutions to fail. This micro-level

definition is one way to think about systemic risk. Recent events have illustrated a more

macro-level definition: the risk that an event could broadly affect the financial system

rather than just one or a few institutions. See, GAO, Systemic Risk: Regulatory Oversight

and Recent Initiatives to Address Risk Posed by Credit Default Swaps, GAO-09-397T

(Washington, D.C.: Mar. 5, 2009).

T

Page 10 GAO-09-975 Troubled Asset Relief Program

unprecedented strains resulting from the placing of Fannie Mae and

Freddie Mac under conservatorship; the failure of financial institutions,

including Lehman Brothers Holdings, Inc. (Lehman Brothers); and the

collapse of the housing markets. The Federal Reserve said that in light of

these events, a disorderly failure of AIG could have contributed to higher

borrowing costs, diminished availability of credit, and additional failures.

They concluded that a collapse of AIG would have been much more severe

than that of Lehman Brothers because of its global operations, large and

varied retail and institutional customer base, and different types of

financial service offerings. The Federal Reserve and Treasury said that a

default by AIG would have placed considerable pressure on numerous

counterparties and triggered serious disruptions in the commercial paper

market. Moreover, counterparties of AIGFP would no longer have

protection or insurance against losses if AIGFP, a major seller of CDS

contracts, defaulted on its obligations and CDO tranche values continued

to decline. The Federal Reserve intended the initial September 2008

assistance to enable AIG to meet these obligations to its counterparties

and begin the process of selling noncore business units in order to raise

cash to repay the credit facility and other liabilities.

17

However, AIG’s

continuing financial deterioration and instability in the financial markets

resulted in subsequent assistance by the Federal Reserve and Treasury in

November 2008 and March 2009 to support AIG’s liquidity and to avoid a

disorderly failure and facilitate an orderly sale of assets and maximum

repayment of federal financial assistance while mitigating disruptions in

the broader financial markets.

AIG’s Financial Problems

Mounted Rapidly in 2008

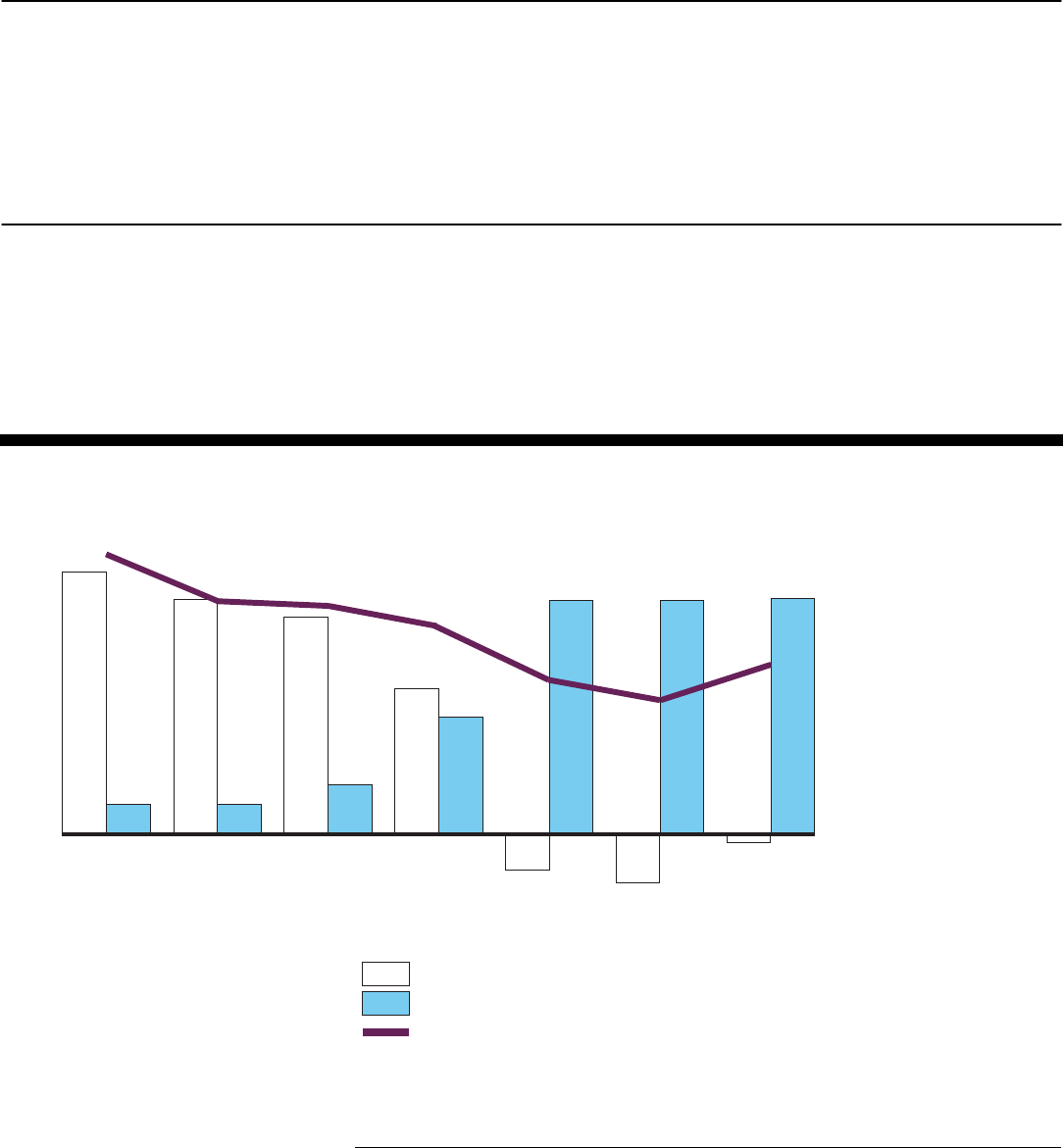

From July 2008 through early September 2008, AIG faced increasing

pressure on its liquidity following a downgrade in its credit ratings in May

2008 due in part to losses from its securities lending program (see fig. 2).

This deterioration followed liquidity strains earlier in the year, although

AIG was able to raise capital in May 2008 to address its needs. Specifically,

the declines in its securities lending reinvestment portfolio of RMBS assets

and declining values of CDOs against which AIGFP had written CDS

protection forced AIG to use an estimated $9.3 billion of its cash reserves

in July and August 2008 to repay securities lending counterparties that

terminated existing agreements and to post additional collateral required

17

The credit facility is a revolving loan created by FRBNY for the general corporate

purposes of AIG and its subsidiaries, including functioning as a source of liquidity to pay

obligations as they come due.

Page 11 GAO-09-975 Troubled Asset Relief Program

by the trading counterparties of AIGFP. AIG attempted to raise additional

capital in the private market in September 2008, but was unsuccessful. On

September 15, 2008, the rating agencies downgraded AIG’s debt rating,

which resulted in the need for an additional $20 billion to fund its added

collateral demands and transaction termination payments.

18

In addition,

AIG’s share price fell from $22.76 on September 8 to $4.76 per share on

September 15.

19

Following the credit rating downgrade, an increasing

number of counterparties refused to transact with AIG for fear that it

would fail. Also around this time, the insurance regulators decided they

would no longer allow AIG’s insurance subsidiaries to lend funds to the

parent company under a revolving credit facility that AIG maintained.

Furthermore, the insurance regulators demanded that any outstanding

loans be repaid and that the facility be terminated.

18

Moody’s Investors Service lowered AIG’s rating to A2 from Aa3, or by 2 notches. Standard

& Poor’s Ratings Services lowered its rating of AIG to A- from AA-, or by 3 notches. Fitch

Ratings reduced its rating of AIG to A from AA-, or 2 notches (see app. IV for ratings

definition).

19

AIG’s share price was quoted at $26.73 per share on the New York Stock Exchange on

July 1, 2008. The shares closed at $3.33 per share on September 30, 2008.

Page 12 GAO-09-975 Troubled Asset Relief Program

[This page left intentionally blank.]

Page 13 GAO-09-975 Troubled Asset Relief Program

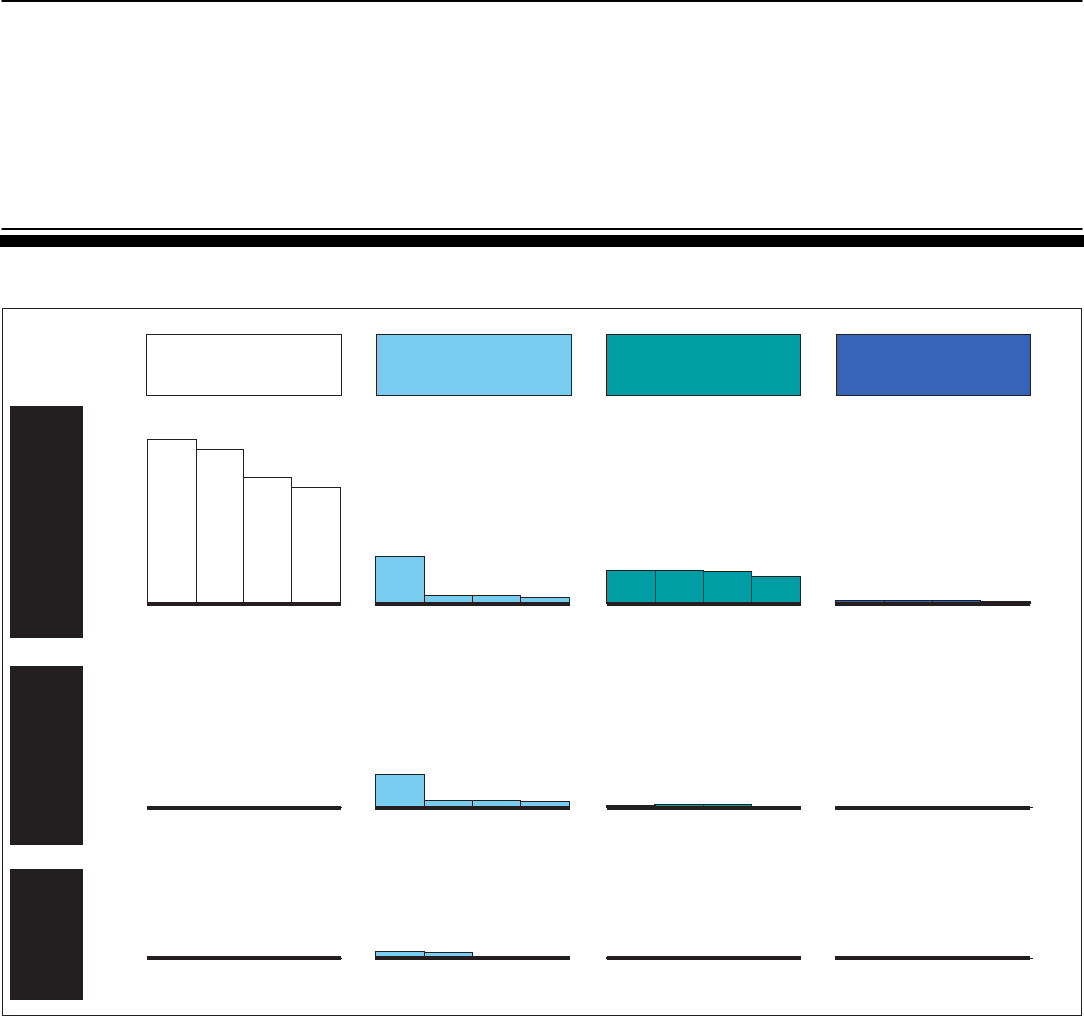

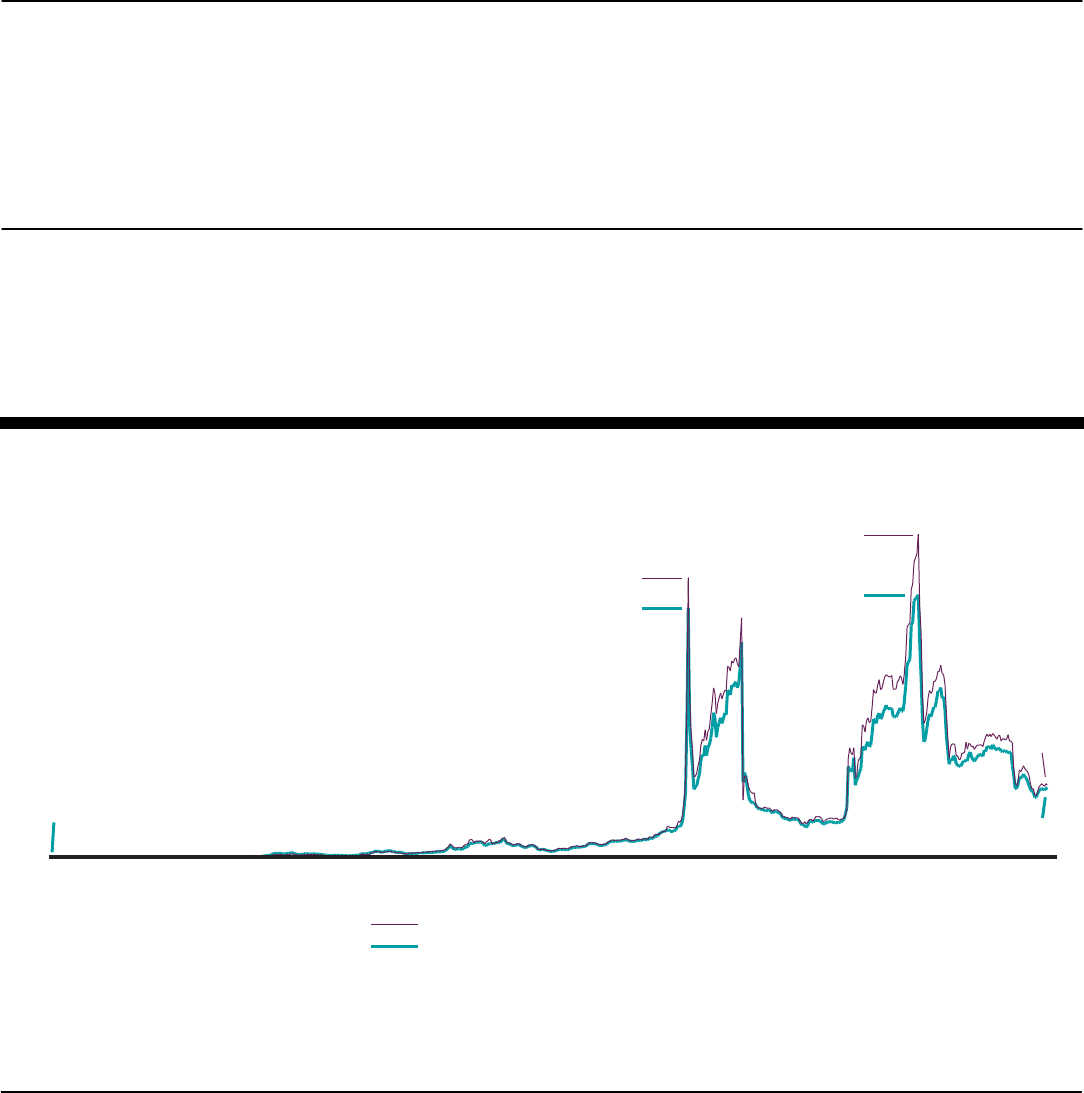

Figure 2: Timeline of AIG’s Financial Difficulties and Government Actions in Response to Market Turmoil, Fall 2007 to

September 30, 2008

Fall 2007: As conditions in the U.S.

housing market deteriorate, American

International Group Financial Products

Corporation (AIGFP) begins to lose

massive amounts of money on credit

default swaps (CDS) issued on

collaterized debt obligations (CDO).

Feb. 2008:

AIGFP

co-founder and

President

resigns after

the division

writes off $11.1

billion on CDS

.

Mar

.

2008: AIG

forms a compensa-

tion committee to

discuss AIGFP and

decides to offer

retention bonuses to

prevent defections

of key employees.

May 20:

AIG raises $20

billion in private

capital.

May 12:

Credit ratings

agencies

Standard &

Poor’s (S&P)

and Fitch

Ratings

(Fitch) each

downgrade

their ratings

on AIG.

May 23:

Credit ratings agency

Moody’s Investor

Service (Moody’s)

downgrades its

ratings on AIG.

Jan. - June 20: AIG experiences significant losses, primarily attributable to AIGFP and decreasing values in it

s

secur

itie

s, particularly in its securities lending portfolio, leading AIG’s need for large amounts of cash collateral. AIG

recognizes $8.9 billion in impairment charges in the first 6 months of the year, primarily related to residential

mortgage-backed securities (RMBS) and structured securities.

July - Aug 31: The super senior CDO

secur

itie

s protected by AIGFP’s super senior

CDS portfolio continue to decline and ratings

of CDO securities are downgraded, resulting

in AIGFP posting an additional $5.9 billion of

collateral. AIG does a strategic review of its

businesses and reviewing measures to

address the liquidity concerns in its securities

lending portfolio and address the ongoing

collateral calls on AIGFP’s super senior

multi-sector CDS por

tf

olio, which as of July

31, 2008, totals $16.1 billion.

Mar. 7:

Securities

and

Exchange

Commission

proposes a

ban on naked

short selling.

May 2:

Federal Reserve’s

Schedule 2 Term

Securities Lending

Facility-eligible collateral

expands to include

AAA-rated asset-backed

securities (ABS).

25201510530

Aug.

25201510530

July

25201510530

June

25201510530

May

25201510530

Apr.

25201510530

Mar.

25201510530

Feb.

25201510530

Jan.

AIG-related actions

Other market events

Page 14 GAO-09-975 Troubled Asset Relief Program

Sources: AIG, Federal Reserve, FRBNY, and Treasury.

Sept. 7: Fannie

Mae and Freddie

Mac are placed

in federal

conservatorship.

Early Sept.: Securities lending requirements and demands to return cash collateral to borrowers to address securities lending activities and continued declining values of

super senior CDO protected by CDS place increasing stress on the AIG parent company’s liquidity

.

S

ept. 8-12: AIG’s common stock price decline from $22.76 to $12.14. AIG reported that as of July 31, 2008, S&P’s, Moody’s, and Fitch’s had placed its senior long-term

debt on negative outlook.

Sept. 11 or 12: AIG approaches FRBNY with two concerns (1) AIG had lent out investment-grade securities for cash collateral, which was invested in illiquid mortgage-

backed securities. Consequently, AIG would not be able to liquidate its assets to meet the demands of its counterp

arties. Since AIG is not regulated by the Federal

Reserve, the agency is not aware of the company’s financial problems. (2) Because AIG is facing a downgrade in its credit rating the next week, it needs immediate

liquidity help.

Sept. 12: S&P places AIG on CreditWatch with negative implications and notes that upon completion of its revie

w, the agency could affirm the AIG parent company’s

current rating of AA- or lower the rating by one to three notches. AIG’s subsidiaries, International Lease Finance Corporation (ILFC) and American General Finance, Inc.

(AGF), are unable to replace all of their maturing commercial paper with new issuances of commercial paper. As a result, AIG advances loans to these subsidiaries to

meet their commercial paper obligations.

Sept. 1

3-14: AIG accelerates the process of attempting to raise additional capital and discusses capital injections and other liquidity measures with potential investors.

AIG also meets with Blackstone Advisory Services LP to discuss possible options. The Federal Reserve examines AIG to determine if it is

systemically important. This is