Spas and the Global

Wellness Market:

Synergies and Opportunities

M a y 2 0 1 0

Spas and the

Global Wellness Market:

Synergies and Opportunities

The Global Spa Summit gratefully acknowledges the support of our exclusive

sponsor who made the research and this report possible.

About Global Spa Summit

The Global Spa Summit (GSS) is an international organization that brings together leaders

and visionaries to positively impact and shape the future of the global spa and wellness

industry. Founded in 2006, the organization hosts an annual Global Spa Summit where

top industry executives gather to exchange ideas and advance industry goals. For more

information on the Global Spa Summit, please visit: www.globalspasummit.org.

About SRI International

Founded in 1946 as Stanford Research Institute, SRI International is an independent, non-

profit organization that performs a broad spectrum of problem-solving consulting and

research and development services for business and government clients around the world.

More information on SRI is available at: www.sri.com.

Copyright

The Spas and the Global Wellness Market report is the property of the Global Spa Summit

LLC. None of its content – in part or in whole – may be copied or reproduced without the

express written permission from the Global Spa Summit. Quotation of, citation from, and

reference to any of the data, findings, and research methodology from the report must be

credited to ―Global Spa Summit, Spas and the Global Wellness Market: Synergies and

Opportunities, prepared by SRI International, May 2010.‖ To obtain permission for

copying and reproduction, or to obtain a copy of the report, please contact the Global

Spa Summit by email: [email protected] or through:

www.globalspasummit.org.

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 SRI International

TABLE OF CONTENTS

Executive Summary ............................................................................................................ i

I. Overview .................................................................................................................... 1

A. Why GSS Is Studying the Wellness Market .......................................................................... 1

B. Research Methodology for This Study .................................................................................... 2

II. Wellness as a Concept ................................................................................................ 3

A. History of Wellness .................................................................................................................... 3

B. Defining Wellness ....................................................................................................................... 6

III. Wellness as an Industry .............................................................................................. 9

A. Drivers of the Growing Wellness Market ............................................................................ 10

B. Defining the Wellness Industry............................................................................................... 17

C. Measuring the Wellness Industry ........................................................................................... 23

IV. The Wellness Consumer............................................................................................ 25

A. Wellness Consumer Segments ................................................................................................ 25

B. Baby Boomer-Driven Market ................................................................................................. 28

C. A Large, Growing Set of Consumers .................................................................................... 30

D. Strong Consumer Interest in CAM Therapies ....................................................................... 32

V. Survey of Industry and Consumer Views on Wellness ............................................. 34

A. Survey Background and Methodology ................................................................................ 34

B. Industry and Consumer Awareness and Definitions of Wellness ..................................... 36

C. Industry Interest in Wellness as a Business Opportunity ................................................... 43

VI. Opportunities for Spas in the Wellness Industry ....................................................... 48

A. Tapping into Reactive/Treatment-Oriented Opportunities and Resources ................... 51

B. Tapping into Proactive/Wellness-Oriented Opportunities and Resources ................... 53

C. Tapping into Workplace Wellness Opportunities and Resources................................... 57

VII. Recommendations for Moving the Industry Forward ............................................... 59

Appendix A: Details on the History and Definitions of Wellness ................................... 68

A. A Timeline of the Evolution of Wellness ............................................................................... 68

B. Definitions of Wellness ............................................................................................................ 73

Appendix B: Estimates of the Size of Wellness-Related Markets .................................... 80

Appendix C: Research Framework ................................................................................. 82

A. Modes of Research and Levels of Rigor .............................................................................. 82

B. Different Audiences and Goals for Research in the Spa Industry ................................... 84

Appendix D: Bibliography .............................................................................................. 87

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 i SRI International

EXECUTIVE SUMMARY

Around the world, there is growing interest in changing the way we take care of

ourselves – not just our bodies, but also our minds, spirit, society, and planet. There is a

growing impetus for a paradigm shift, a switch from mere reactivity – trying to treat

or fix our problems – to a proactive and holistic approach to addressing and prevent

the root causes of our personal and societal ills. This is what the wellness movement is

all about.

Recognizing the opportunities that wellness presents for the spa industry, the Global

Spa Summit has commissioned SRI International to conduct an in-depth analysis of the

emerging global wellness market. The objectives of this study are:

To provide a rigorous investigation of the market and consumer forces driving the

growth of wellness services and products.

To collect some of the first ever primary data from industry and consumers about

their views on wellness.

To highlight key areas of opportunity and intersection where the spa industry can

take advantage of growth and partnership opportunities in myriad wellness-

related sectors.

To provide recommendations on how spas – both as a collective industry and as

individual business owners – can position themselves strategically to capitalize on

growing wellness lifestyle trends.

Wellness: The Concept, the Industry, and the Consumer

Wellness as a concept has a long, ancient tradition and body of knowledge behind it

Wellness is a modern word with ancient roots. As a modern concept, wellness has

gained currency since the 1950s, 1960s, and 1970s. Starting with a seminal, but little

known, book published by Dr. Halbert Dunn in 1961 (called High-Level Wellness), the

writings and leadership of an informal network of physicians and thinkers in the United

States have largely shaped the way we conceptualize and talk about wellness today.

The origins of wellness, however, are much older – even ancient. Aspects of the

wellness concept are firmly rooted in several intellectual, religious, and medical

movements in the 19

th

century United States and Europe. The tenets of wellness can

also be traced to the ancient civilizations of Greece, Rome, and Asia.

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 ii SRI International

Defining Wellness

There are a number of rigorous and well-thought-out definitions of wellness, developed over

time by the leading thinkers in the field. In fact, it was the process of attempting to define,

understand, and measure wellness during the 1950s-1970s that initially led to the

propagation of the concept in the modern era. However, like the term ―spa,‖ there is still no

universally accepted definition of the word ―wellness.‖

The World Health Organization’s definition of ―health‖ is a convenient, internationally

recognized description that captures the broad tenets of wellness. This definition – adopted by

the WHO in 1948 – was significant in the fact that it went beyond just the physical state of

freedom from disease and emphasized a positive state of being that includes mental and

social dimensions. It also laid the groundwork for much of the ongoing thinking about wellness

in the mid-20

th

century.

Health is a state of complete physical, mental and social well-being and not merely

the absence of disease or infirmity. ~Preamble to the Constitution of the WHO

While recognizing that there are regional variations in the concept of wellness, several

common threads stand out across the various definitions of wellness:

Wellness is multi-dimensional.

Wellness is holistic.

Wellness changes over time and along a continuum.

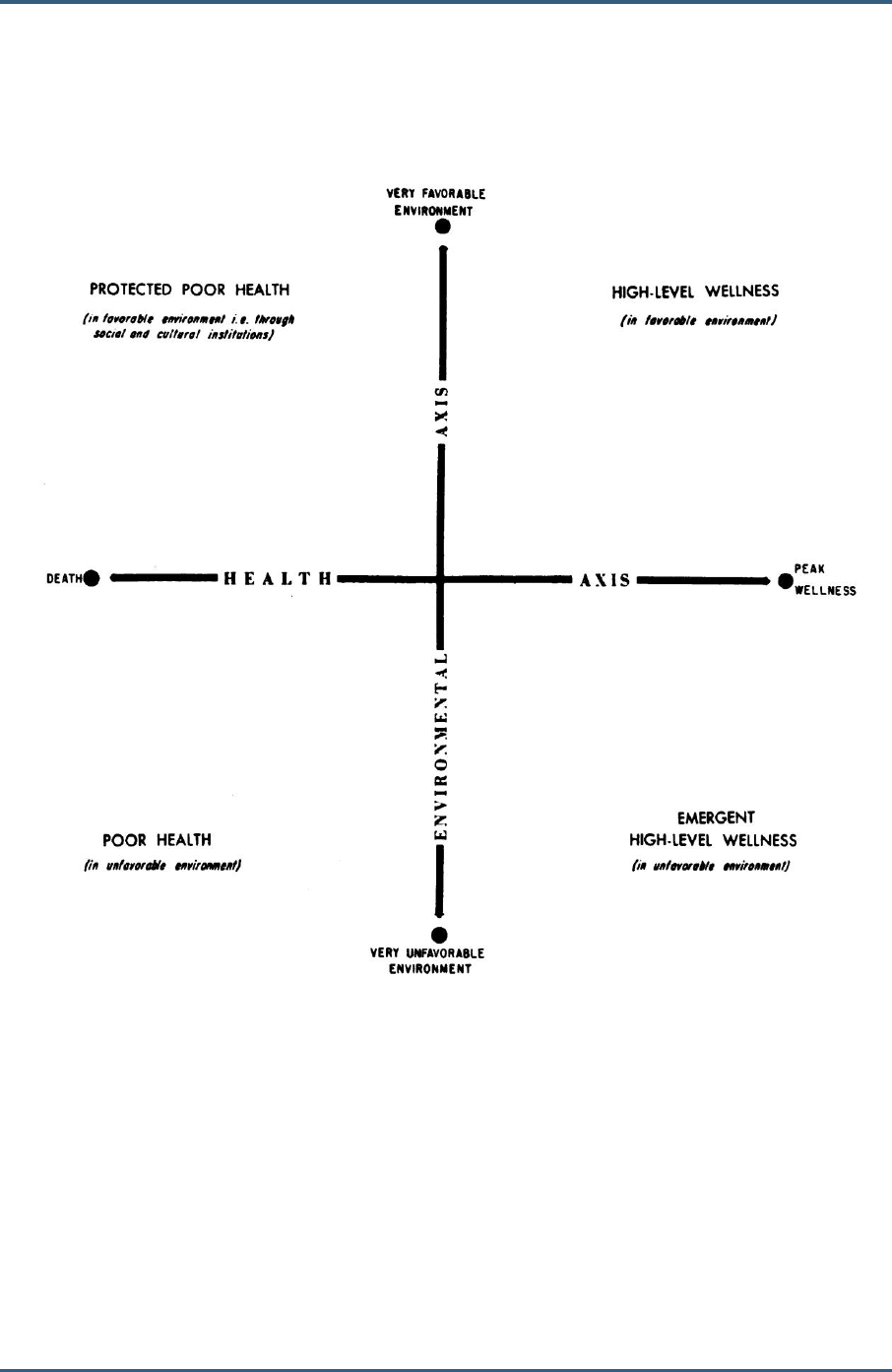

Wellness is individual, but also influenced by the environment.

Wellness is a self-responsibility.

The decision of whether or how to use the word ―wellness‖ in marketing is probably best left to

individual businesses to decide, based on their own business strategy and customer base.

However, it would also be beneficial for the spa industry to start thinking and talking about

wellness in a more coherent and harmonized manner. In the recommendations section of this

report, we provide guidance on some core principles of wellness that could be adopted by the

spa industry.

The burgeoning wellness industry includes proactive approaches to feeling better and

preventing sickness from developing

In the fields of economics and business, there is no clearly defined wellness industry,

although there is an emerging sense that such an industry does exist and is growing

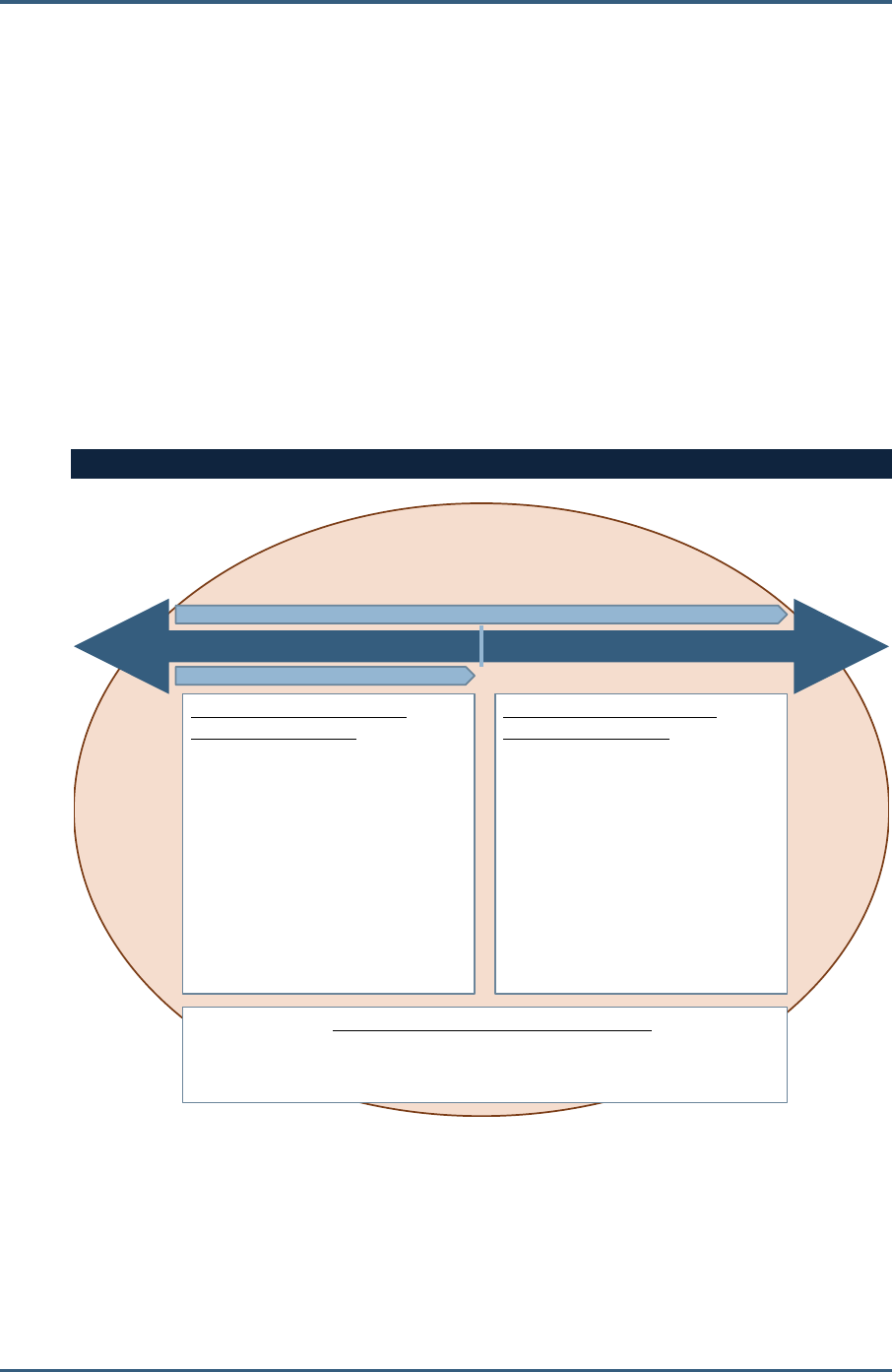

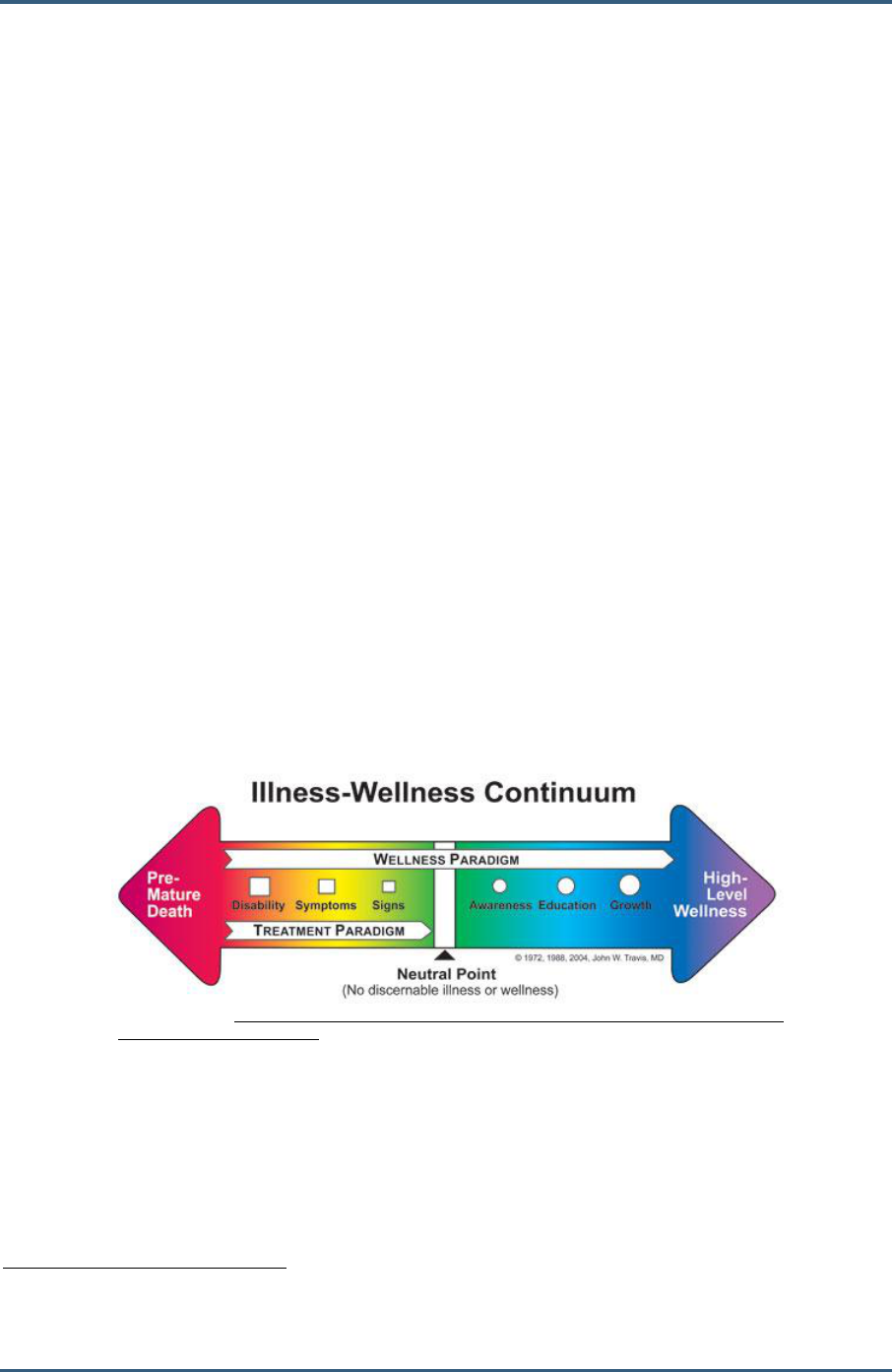

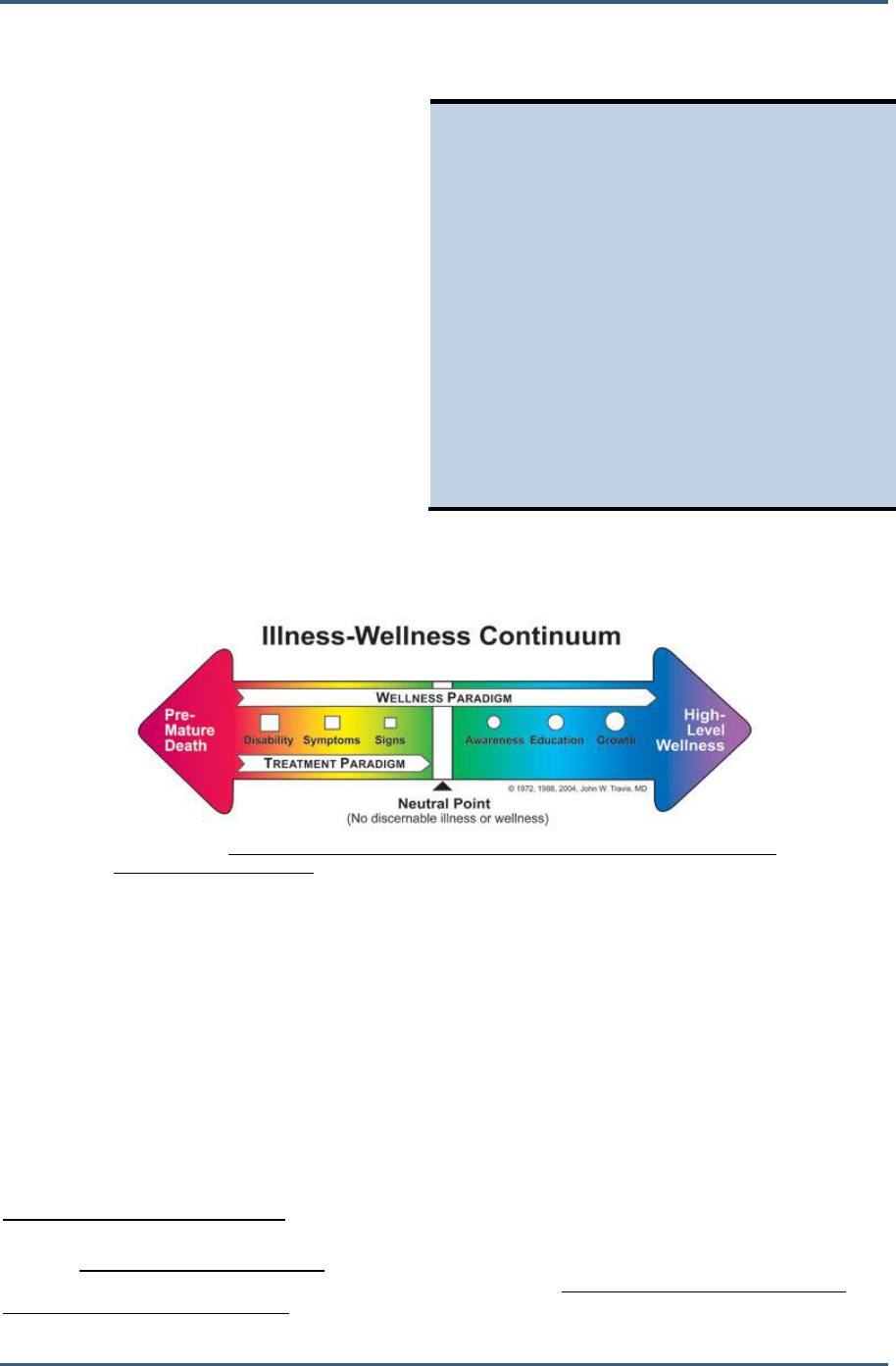

rapidly. An easy way to understand the wellness industry is to view it on a continuum.

On the left-hand side of the continuum are reactive approaches to health and wellness

– that is, mechanisms to treat or address existing illnesses or conditions. Conventional

medicine (which is sometimes called the ―sickness industry‖) would fall on the left-hand

side of the continuum. Addressing problems and curing diseases brings a person only

to the middle, or neutral point, of the continuum. To the right-hand side are proactive

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 iii SRI International

approaches to health and wellness – that is, things that enhance quality of life,

improve health, and bring a person to increasingly optimum levels of well-being.

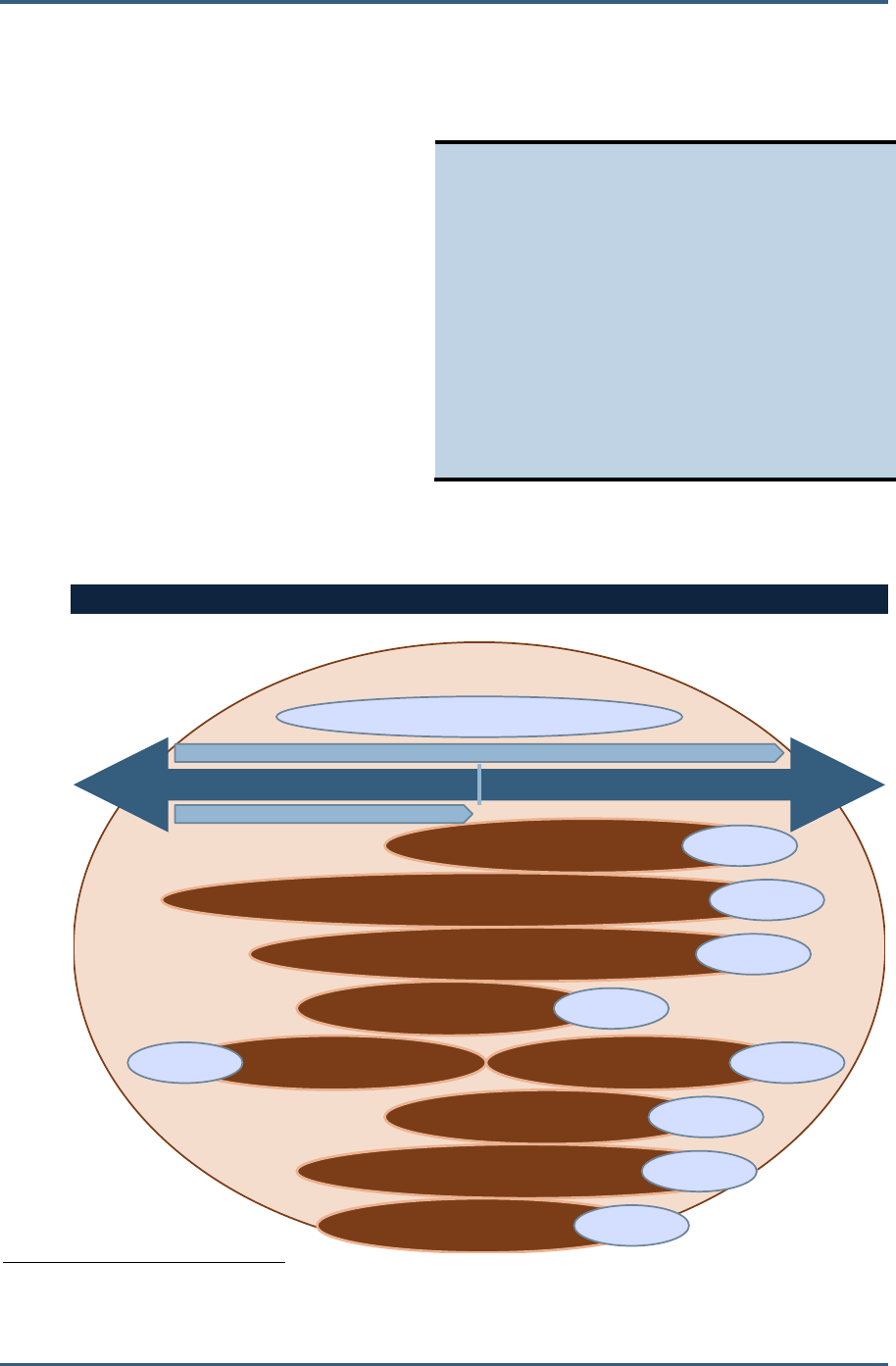

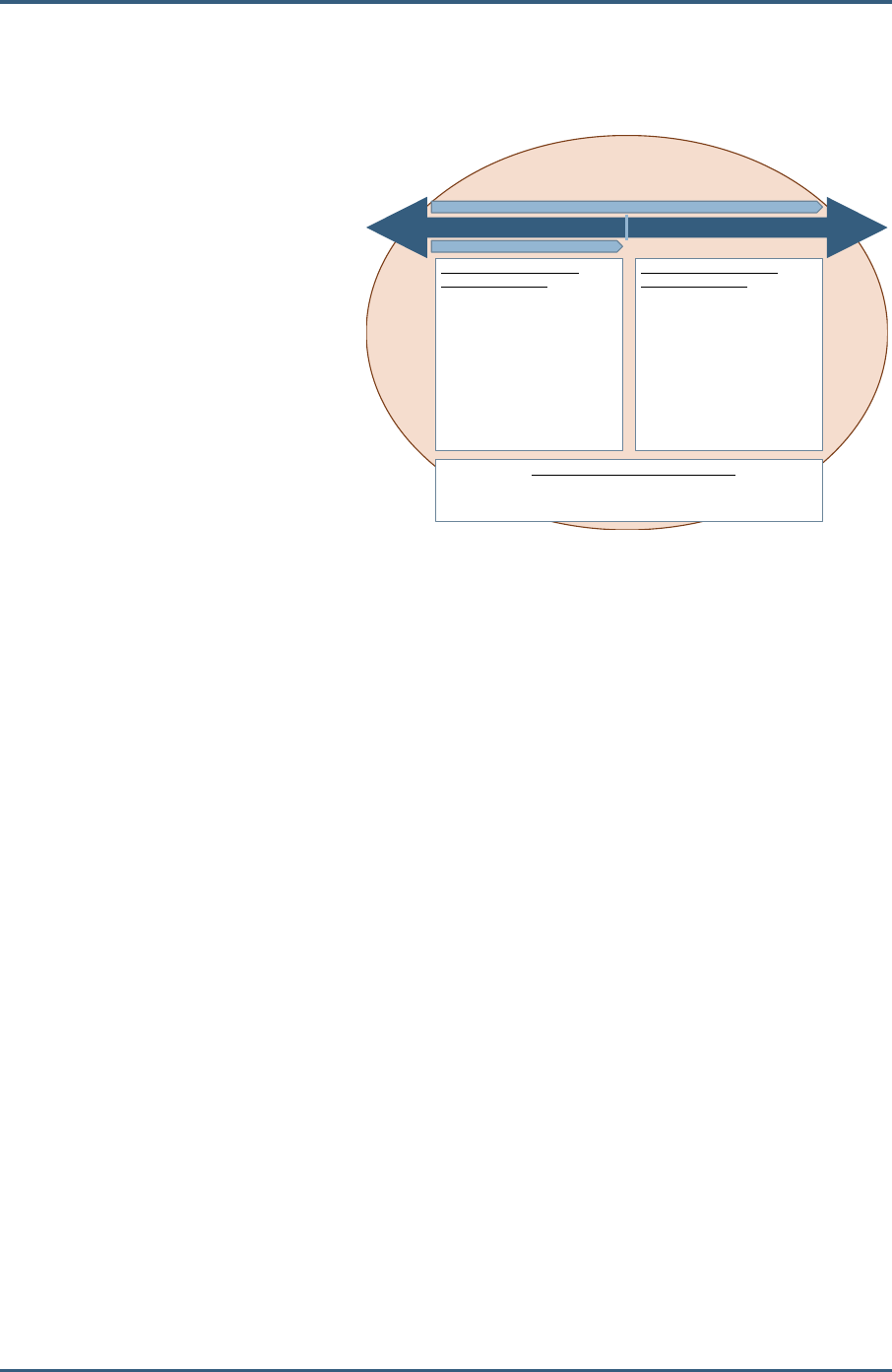

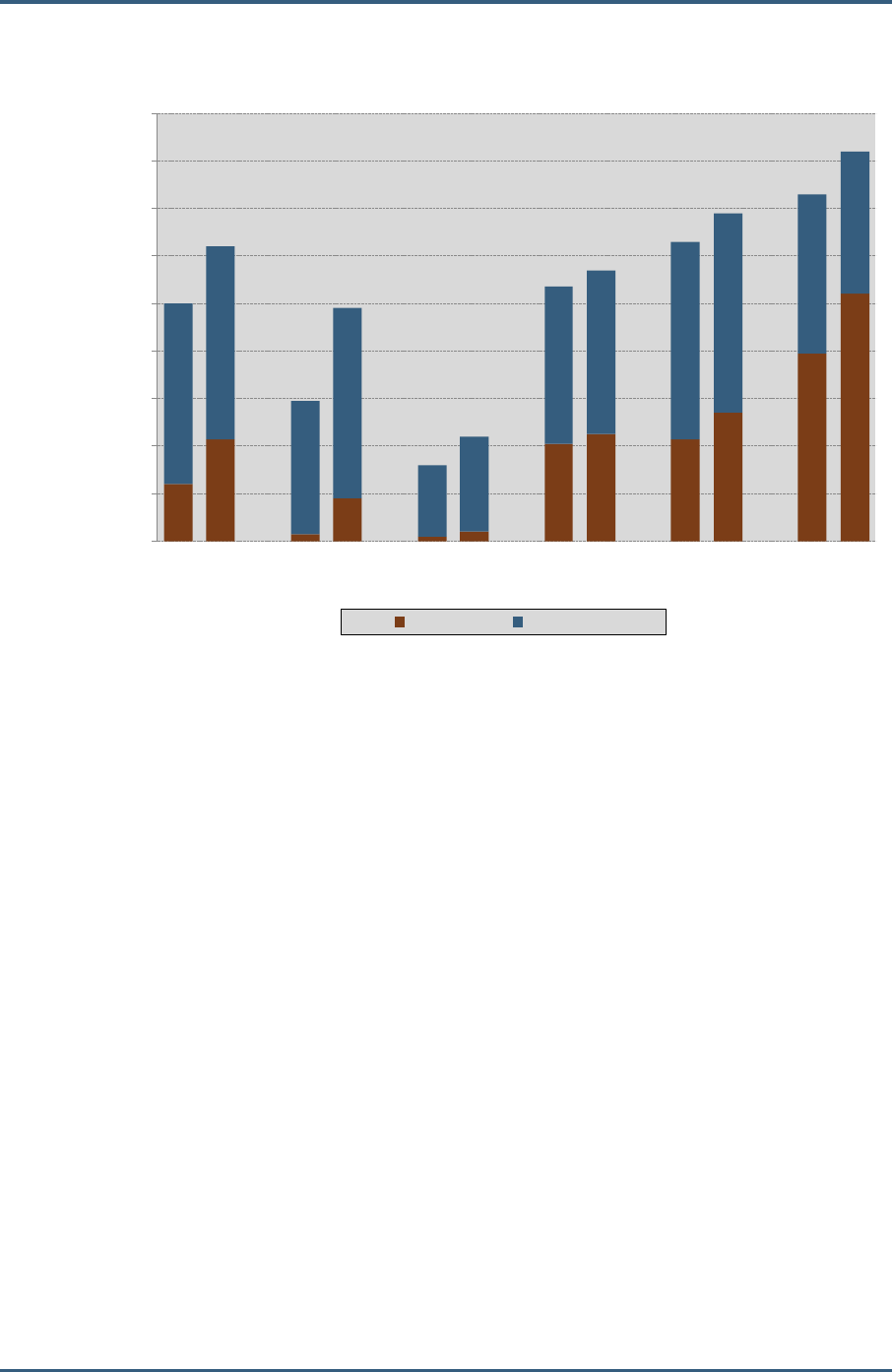

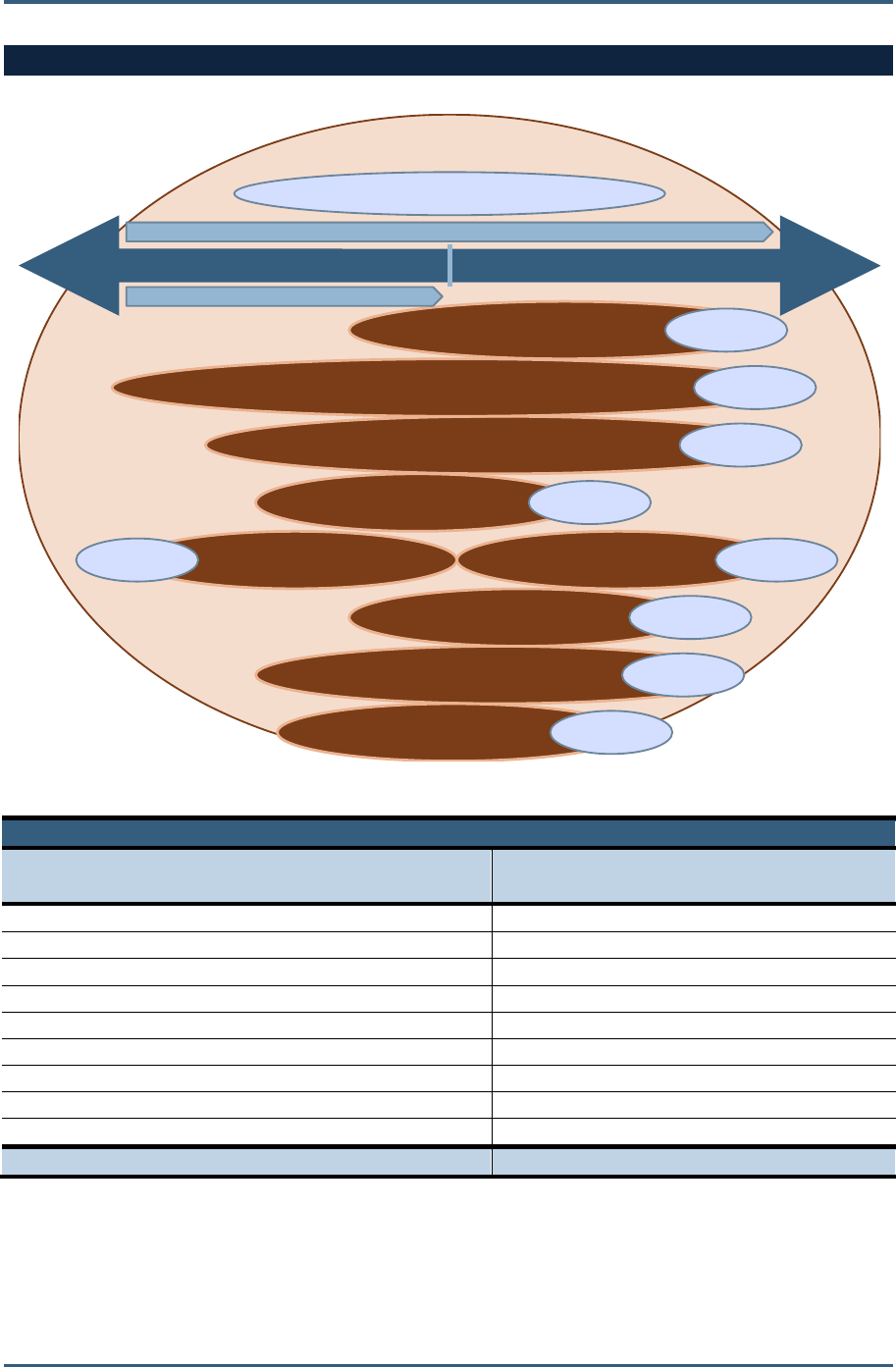

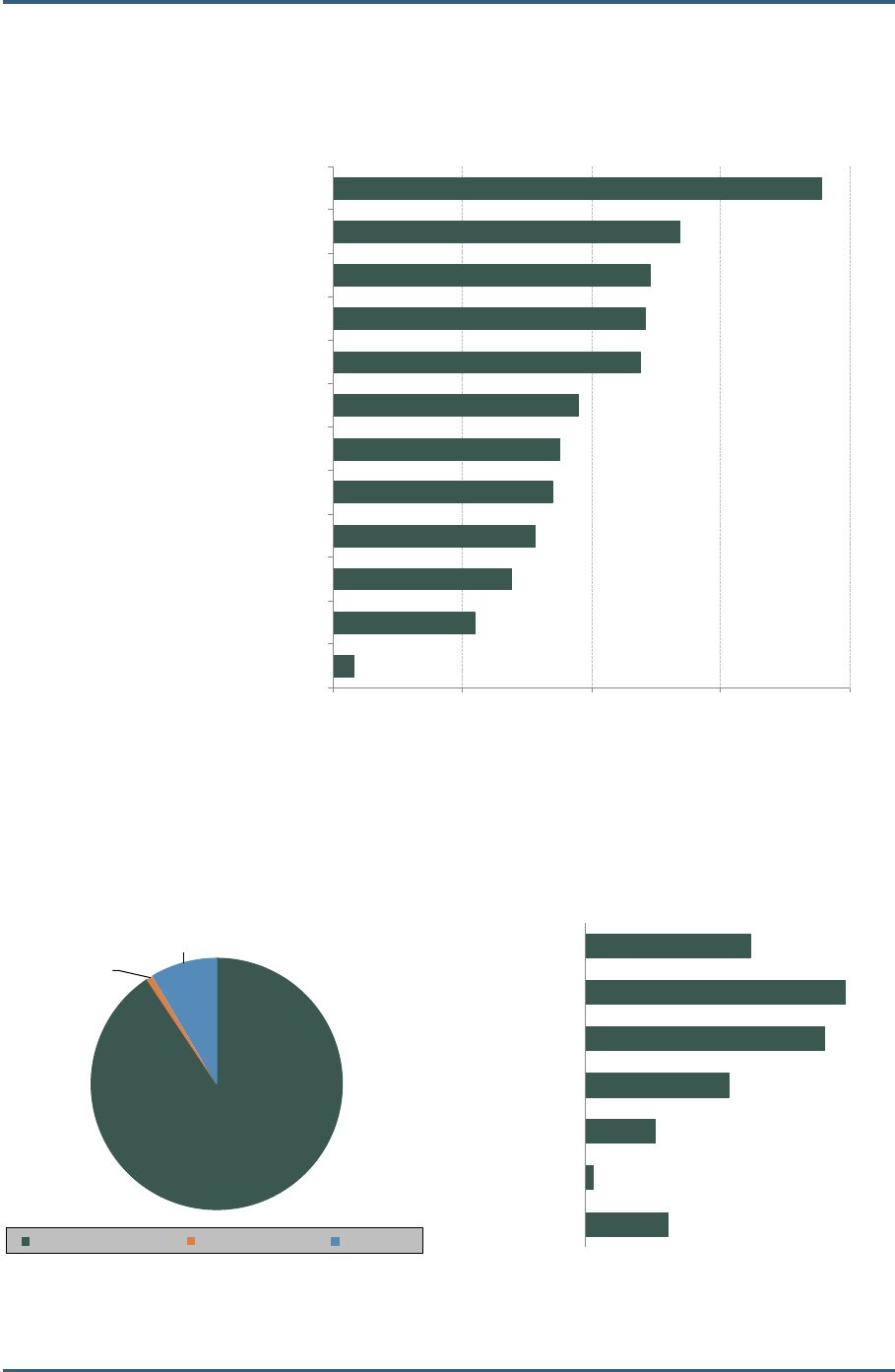

SRI has developed for this study a

model of the wellness industry that

includes nine industry sectors, and

each sector is depicted along the

wellness continuum.

1

SRI estimates

conservatively that the wellness

industry cluster represents a market of

nearly $2 trillion dollars globally. All

of the wellness sectors have direct

market interactions with the core spa

industry, and they present high-

potential opportunities for the spa

industry to pursue new wellness-oriented business ventures, investments, and

partnerships beyond the menu of products and services traditionally offered at spas.

Estimated Global Market Size of the Wellness Industry Cluster

1

The continuum concept used in this model of the wellness cluster is adapted from Dr. John W. Travis’ wellness-

illness continuum, detailed in Appendix A.

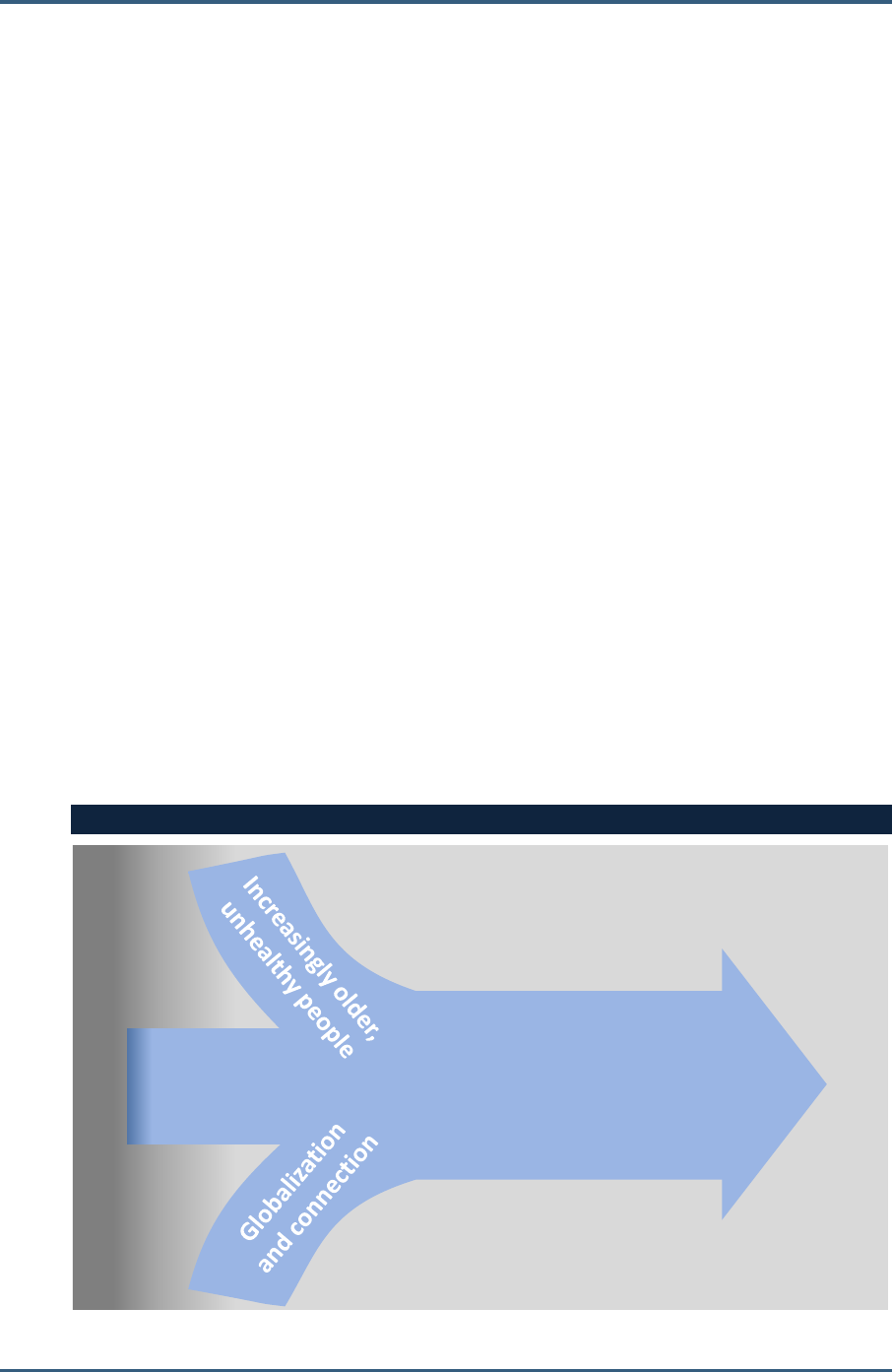

Drivers of the Growing Wellness Industry

Several major trends are driving the growth of

wellness as an industry. These trends not only

directly impact the spa industry and its customers,

but also are opening new opportunities for spas to

play a leading role in a paradigm shift toward

more proactive ways of taking care of ourselves.

Increasingly older, unhealthy people

Failing medical systems

Globalization and connection

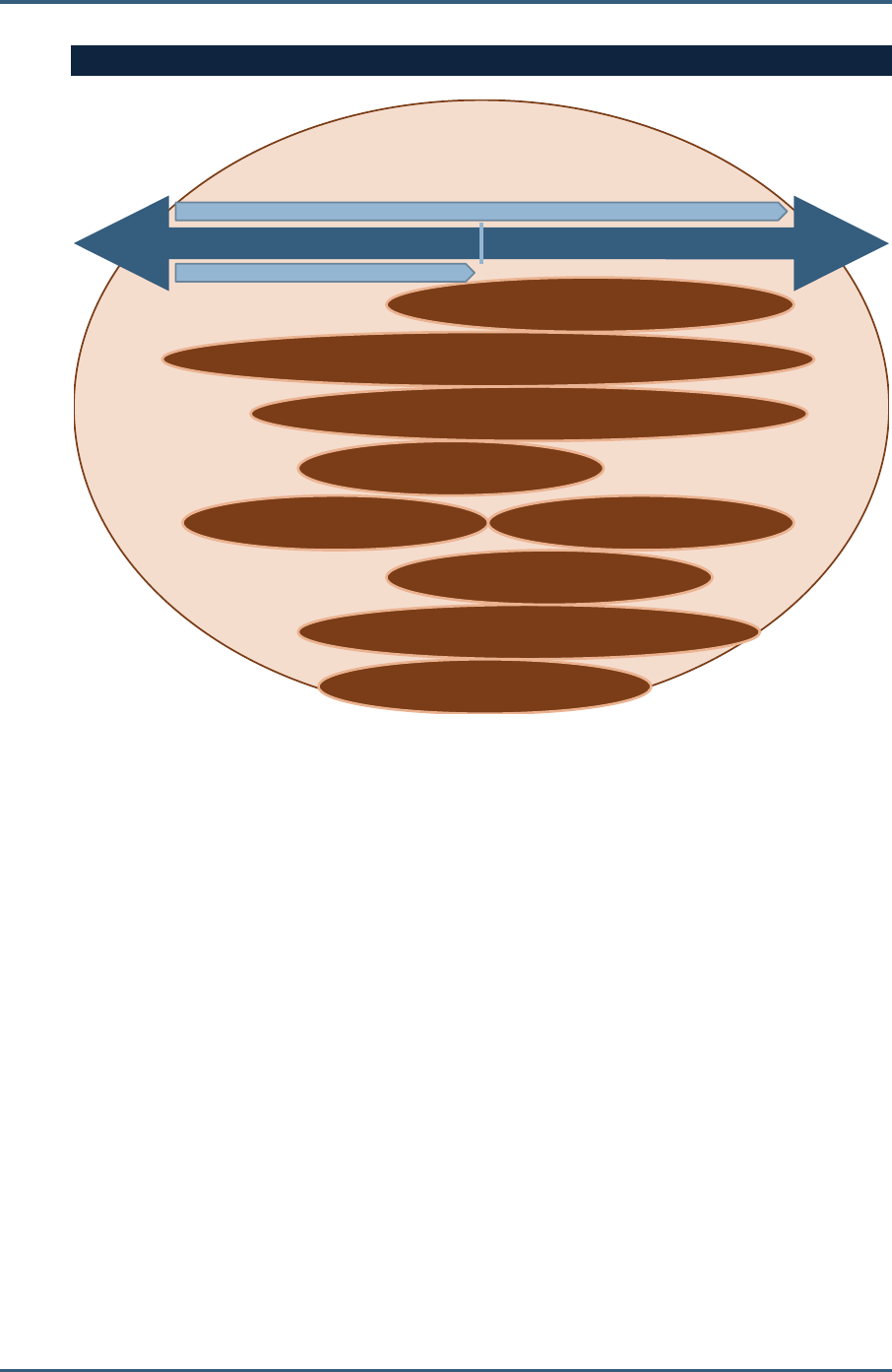

Conventional,

Medically-Oriented

Approaches

(to solve problems)

Integrated,

Wellness-Oriented

Approaches

(to improve quality of life)

Fitness & Mind-Body

Spa

Healthy Eating/Nutrition & Weight Loss

Preventive/Personalized

Health

Complementary & Alternative Medicine

Beauty & Anti-Aging

Treatment Paradigm

Wellness Paradigm

Reactive Proactive

The Wellness Cluster

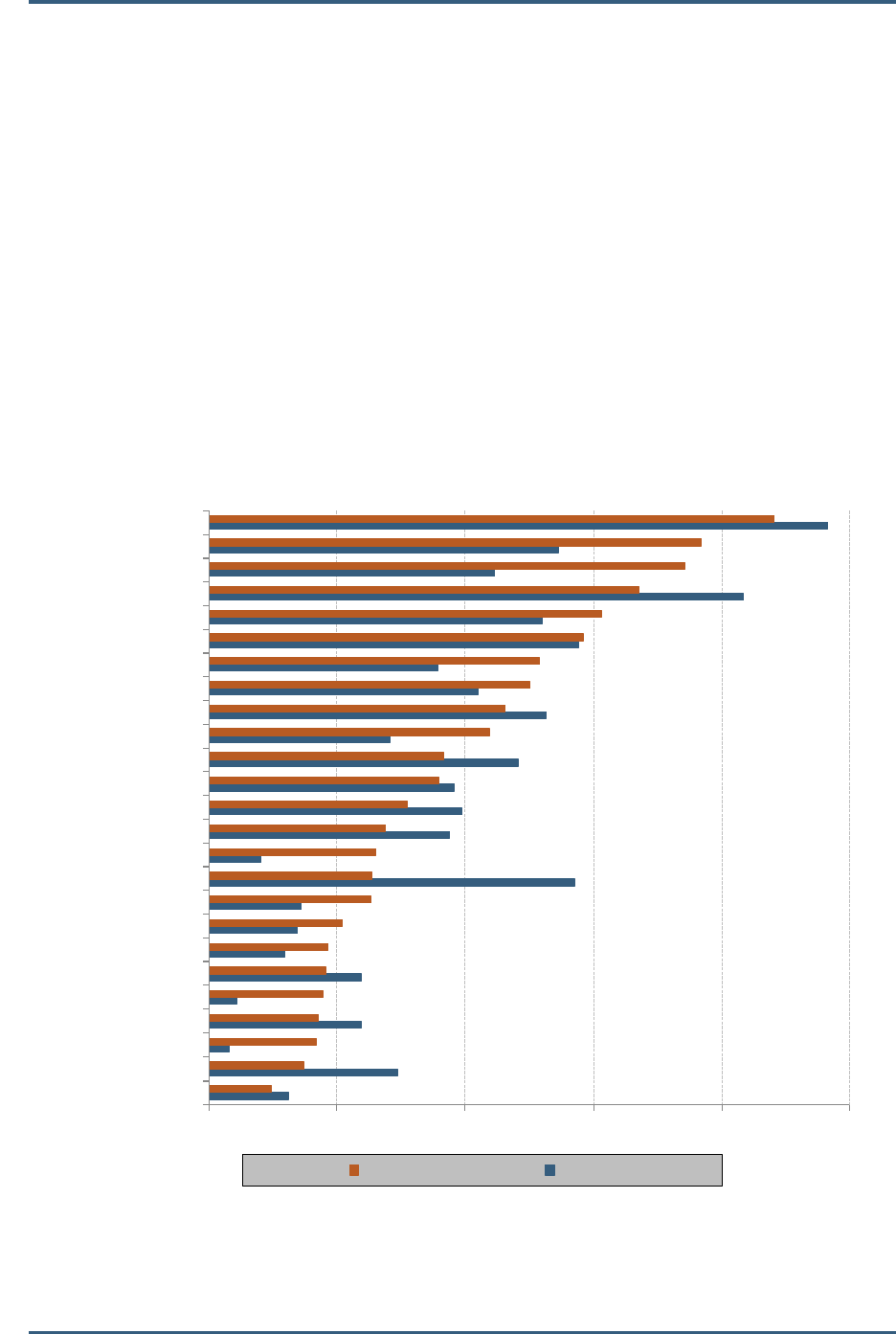

Workplace Wellness

Medical Tourism Wellness Tourism

$276.5

$390.1

$679.1

$113.0

$243.0

$50.0 $106.0

$60.3

$30.7

(US$ billions)

A $1.9 trillion global market

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 iv SRI International

The consumer market for wellness is large and growing, and the potential market is even

larger

Anecdotal evidence – from leading stakeholders and thinkers in the spa industry and

the broader wellness cluster – suggests that the ―Baby Boomer‖ generation has been

and is currently the core consumer group driving the growth of the wellness industry.

However, there is also a large and growing younger generation of consumers

interested in wellness products and services, as well as a large, as-yet unstudied and

untapped local market for wellness in Asia, Latin America, and other regions around

the world.

Wellness consumers are not a niche market – their number is already large and

growing. In fact, SRI estimates that there are already about 289 million wellness

consumers in the world’s 30 most industrialized and wealthiest countries. Like the wellness

industry, wellness consumer segments can also be viewed on a continuum:

Health and Wellness Consumer Segments

Sickness reactors,

not active spa-goers

Wellness focused, moderate-to-active spa-goers

Periphery

Mid-level

Core

―Entry level‖ health and

wellness consumers

Aspire to be more

involved in health and

wellness, but their

behaviors do not yet

follow their aspirations

Are mostly ―reactive‖

rather than ―proactive‖

when it comes to matters

of health and wellness

Moderately involved in a

health and wellness

lifestyle

Tend to follow some of

the trends set by the Core

Purchase large amounts

of both conventional and

health and wellness-

specific products

Still somewhat concerned

with price and

convenience, but also

driven by knowledge and

experience

Most involved in a health

and wellness lifestyle

Serve as trendsetters for

other consumers

Health and wellness is a

major life focus for them

Driven by sustainability,

authenticity, and local

sources

Source: GMDC and The Hartman Group, Consumer Shopping Habits for Wellness and Environmentally Conscious Lifestyles Study:

Insights for Health, Beauty and Wellness, September 12, 2009, http://www.pacific.edu/Documents/ school-

pharmacy/acrobat/Consumer%20Shopping%20Habits%20for%20Wellness%20-%20Presentation.pdf.

Survey of Industry and Consumer Views on Wellness

SRI and GSS developed two short surveys that were distributed to spa stakeholders

and consumers around the world. These surveys queried industry members (319

respondents) and consumers (1,077 respondents) about their views on wellness – both

as a concept and as a trend – in relationship to business planning, purchasing patterns,

and lifestyle.

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 v SRI International

Industry and Consumer Awareness and Definitions of Wellness

Eighty-three percent of industry respondents are using the term ―wellness‖ in their

businesses, and almost all consumer respondents are aware of the term.

Industry and consumers tend to define wellness in similar ways, and both groups

relate the following words and phrases most closely with wellness: quality of life,

physical fitness, happiness, balance, relaxation, emotional balance, stress

reduction, and spa. However, consumers rank ―mental health‖ and ―medical health‖

among their top ten terms associated with wellness, while industry members rank

―holistic health‖ and ―spiritual health‖ in their top ten.

Eighty-one percent of consumer respondents stated that they are ―extremely‖ or

―very interested‖ in improving their personal wellness. When seeking to enhance

their wellness, consumer respondents said they are most likely to exercise, eat

better, and visit a spa. The placement of exercise and eating better at the top of

the list indicates an opportunity for spas to add or enhance their service offerings

in the areas of fitness and nutrition.

Seventy-one percent of consumer respondents said they would be ―much more

likely‖ or ―somewhat more likely‖ to visit a spa if they learned that a series of

research studies demonstrated that spa treatments deliver measurable health

benefits.

Industry Interest in Wellness as a Business Opportunity

Eighty-nine percent of industry respondents see wellness as an important future

driver for the spa industry.

Eighty-two percent of industry respondents indicated that they have taken steps to

respond to the wellness movement over the last five years, and among this group,

91% also reported that these changes have yielded growth in revenues.

Nine out of 10 industry respondents plan to make wellness-related investments in

the next 5-10 years. Almost all of them believe their business will see growth from

these investments, and 70% expect their wellness-related investments to lead to

more than 10% revenue growth.

Opportunities for Spas in the Wellness Industry

Spas are already providing wellness, even if they don’t recognize it or claim it. The

tradition of spa as a place for healing, renewal, relaxation, and ―feeling well,‖

positions the spa industry as one of the most logical sectors to take advantage of (and

help lead) the wellness movement. Wellness also provides an opportunity to reshape

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 vi SRI International

the image of spa, to regroup after the global recession, and to position spa as an

investment or an essential element in maintaining a healthy lifestyle.

There are a number of

business opportunities for the

spa industry to pursue along

the wellness continuum.

While some opportunities

will require long-term effort

and investment, others

simply require spa owners

and investors to make small

adjustments to their service

offerings and reexamine

their marketing approaches

and customers with a new,

wellness-oriented viewpoint.

Tapping into Reactive/Treatment-Oriented Opportunities and Resources

1. Partner with conventional medical establishments to deliver complementary

and integrated healing services to medical patients (such as massage,

hydrotherapy, etc.), delivered at medical centers or through referral networks.

Spas can also develop specialized treatment packages tailored for specific

patient profiles (such as cancer, diabetes patients, etc.) or package appearance

and confidence-enhancing spa and beauty services/products for seriously ill

patients, to boost their mood, self-image, and positivity about recovery.

2. Partner with the medical industry to encourage and conduct evidence-based

research, and explore ways for individual spas to support specific research

studies.

3. Partner with the medical tourism industry to create complementary services for

medical tourists in the pre-op, post-op, and recovery phases; deliver medical

tourism services at spas; and create integrated spa, beauty, and wellness

packages for the companions traveling with medical tourists.

Tapping into Proactive/Wellness-Oriented Opportunities and Resources

1. Repackage existing offerings and develop new offerings to define and market

spas as a wellness necessity, especially by drawing upon traditional/culturally-

based healing therapies; educating consumers on the therapeutic benefits of these

treatments; and placing greater emphasis on partnering services with products that

Conventional,

Treatment-Oriented

Approaches

(to solve problems)

Integrated,

Wellness-Oriented

Approaches

(to improve quality of life)

Treatment Paradigm

Wellness Paradigm

Reactive Proactive

Wellness Opportunities

Reactive/Treatment-Oriented

Opportunities for Spa:

Partner with conventional medical

establishments to deliver

complementary and integrated

healing services

Partner with the medical industry to

conduct evidence-based research

Partner with the medical tourism

industry to create complementary

services

Proactive/Wellness-Oriented

Opportunities for Spa:

Repackage and develop new

offerings to define and market

spas as a wellness necessity

Help consumers understand and

select the spa’s wellness offerings

Position spas as the center of

integrated/holistic approaches to

wellness

Provide continuity of care to

customers

Workplace Wellness Opportunities for Spa:

Deliver executive health services

Manage general wellness of employees

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 vii SRI International

have therapeutic value, that promote healthy aging and self image, and that can

help a client continue to feel and look well after leaving the spa.

2. Help consumers understand and select the spa’s wellness offerings by utilizing

wellness assessment tools to create individually tailored packages of

services/products and by reframing spa offerings within the context of the

different dimensions of wellness.

3. Position spas as the center of integrated/holistic approaches to wellness by

creating integrated wellness packages that include spa services, personal training,

mind-body services, nutrition counseling, life coaching, healthy aging and self-

image-boosting beauty services/products, and so on. Take spa out of its usual

―box‖ or niche – bring spa services into new physical locations, make spa and

wellness services accessible to different consumer segments, and develop

specialized services that target specific consumer markets.

4. Provide continuity of care to customers by building long-term relationships

through wellness membership programs or wellness/life coaching services.

Tapping into Workplace Wellness Opportunities and Resources

1. Deliver executive health services, such as executive health assessments or

executive retreats, and package wellness services and lifestyle counseling with

these programs.

2. Manage general wellness of employees by developing corporate membership

programs or by delivering wellness-related spa services at the workplace.

Recommendations for Moving the Industry Forward

1. Develop a harmonized understanding of wellness terminology and concepts in

relation to the spa industry, to reduce consumer confusion. Although it is not

necessary for all spa stakeholders to define wellness in exactly the same way, we

recommend that the industry begin thinking and talking about wellness organized

around a few core principles:

Wellness is multi-dimensional and holistic, incorporating dimensions of physical,

mental, emotional, spiritual, social, and environmental wellness.

Wellness can be envisioned and explained by the illness-wellness continuum.

Wellness is consumer-driven.

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 viii SRI International

2. Promote and support ongoing conversations on wellness in the spa industry (and

with other wellness sectors) to keep abreast of a rapidly growing and changing

wellness market. The Global Spa Summit and/or other regional/international

associations present ideal platforms and can organize ongoing wellness symposiums;

invite leading thinkers and organizations in the wellness industry to educate the spa

industry; take dialogue and discussion to the regional level; and facilitate dialogue

with the beauty/anti-aging, fitness, and conventional medical sectors.

3. Build a body of evidence-based consumer research that connects spa to wellness.

Consumer research sponsored by regional or country industry associations and

focusing on wellness consumers within specific markets and regions would be of benefit

to many spa stakeholders.

4. Facilitate and publicize evidence-based/scientific research on wellness

approaches. For the conventional medical community to widely accept, recommend,

and prescribe spa-based treatments, they will need to ―see the data‖ delivered by

rigorously designed clinical trials, and then see the data duplicated in additional,

similar trials. With the medical community on board, employers, insurers, and public

health officials are likely to follow suit, which will offer spas increased access to

insurance reimbursement and wellness programs funded by employers and

governments. The spa industry can facilitate more scientific research by:

Making more accessible the existing evidence-based research studies on the

benefits of spa and alternative therapies.

Encouraging more clinical studies by reaching out to the medical and research

community.

Offering a global research award for original research on the health

benefits/effects of spa-related treatments.

5. Support new industry research to raise awareness of and attract investment in

wellness opportunities. Industry research areas that could be supported or facilitated

by GSS or other organizations include:

Financial benchmarks and metrics for spa and wellness-related sectors.

Case studies of successful wellness-oriented business models.

Spa industry size and economic impact studies at the regional and country

levels.

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 ix SRI International

6. Connect with wellness-related public sector tourism and public health

organizations to leverage their resources. The spa industry would be well served by

seeking to forge a closer connection and dialogue with government agencies that are

overseeing key wellness segments:

Building an ongoing dialogue, at the industry level, with global tourism

organizations (e.g., WTO, WTTC) about the role of spas in the medical and

wellness tourism markets.

Reaching out to regional tourism organizations and ministries, to leverage the

promotion and brand-building that has been done at the country/regional

levels.

Making connections with public health authorities, such as government-funded

medical research institutions.

7. Teach spa therapists to understand and promote wellness. The GSS and other

industry organizations could work with major spa therapist training schools to provide

guidance on new curriculum that would address wellness concepts and teach spa

therapists how to educate their customers in holistic wellness principles and behaviors.

8. Educate spa management on wellness concepts and business savvy. Industry

leaders could work more closely with the handful of spa management training

programs/universities that exist to help shape the curriculum to reflect future market

needs – for example, incorporating a ―wellness theory‖ component into the

coursework; providing additional education on trends and operational approaches in

other wellness-related sectors (e.g., fitness, medicine, corporate wellness, healthy

aging/beauty, etc.); and providing more extensive coursework on business

development, promotion, and marketing.

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 1 SRI International

I. OVERVIEW

Around the world, there is growing interest in changing the way we take care of

ourselves – not just our bodies, but also our minds, spirit, society, and planet. In fact,

experts urge that such a paradigm shift needs to occur if we are to successfully

address major problems facing our world in the coming years. They call for a switch

from mere reactivity – trying to treat or fix our problems – to a proactive and holistic

approach to address and prevent the root causes of our personal and societal ills.

That is what the wellness movement is all about. However, despite growing popularity,

wellness concepts have not yet reached mainstream recognition and acceptance. And

ironically, as wellness practices are spreading, fundamentally preventable problems

like obesity, poor nutrition, and other chronic diseases like heart disease and cancer

are growing even more rapidly.

Many in the spa industry dismiss ―wellness‖ as merely a passing fad confined to a

small market of Western, affluent consumers. That is not the case. First, wellness as a

concept has a long and ancient tradition and body of knowledge behind it. Second,

the consumer market for wellness is large and growing, and the potential market is

even larger. Third, a paradigm shift in our economy and society toward wellness-

oriented approaches will be imperative to the future health and longevity of our

population and our planet. Hopefully, this shift is inevitable.

A. Why GSS Is Studying the Wellness Market

At recent Global Spa Summits, the theme of wellness has emerged as one of the most

talked-about and important trends shaping the spa industry’s future. The importance

of wellness for the industry was underscored in the 2009 GSS Delegate Survey, which

found that delegates perceive the preventive health segment as offering the biggest

opportunity for their future business, and that preventive healthcare ranks as one of

the two greatest forces influencing their spa businesses moving forward. In this survey,

46% of delegates also reported that, among potential partners, they are most

interested in collaborating with the healthcare industry.

The 2010 Global Spa Summit has a theme of ―bridges worth building,‖ focusing on

nurturing and capitalizing on the growing linkages across the spa, beauty, medical,

and other sectors. In support of this theme, SRI International was commissioned by the

Global Spa Summit to conduct an in-depth analysis of the emerging global wellness

market and the opportunities it presents for the spa industry. The objectives of this

study are:

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 2 SRI International

To aggregate and synthesize the fragmented and emergent body of research

studies and data that currently exists on wellness-related topics, and to present this

information in an easy-to-read and usable format for busy spa industry leaders.

To collect some of the first ever primary data from industry and consumers about

their views on wellness – both as a concept and as a trend – with the goal of

identifying areas where ongoing research is needed.

To help spa industry leaders collect and synthesize their own, collective body of

experience and knowledge on the topic of wellness, and, through discussion at the

industry level, to transform these disparate opinions into a consensus-based set of

opportunities and recommendations.

To provide a rigorous investigation of the market and consumer forces driving the

growth of wellness services and products, with the goal of exploring how the spa

industry ―fits‖ in relation to the broader wellness market.

To highlight key areas of opportunity and intersection where the spa industry can

take advantage of growth and partnership opportunities in myriad wellness-

related sectors.

To provide recommendations on how spas – both as a collective industry and as

individual business owners – can position themselves strategically to capitalize on

growing wellness lifestyle trends.

B. Research Methodology for This Study

To develop the analysis for this study, SRI conducted extensive primary and secondary

research. We first conducted an extensive literature review of the major studies,

reports, data, and qualitative assessments available on market trends in key wellness

lifestyle sectors (such as health/medicine, beauty, fitness, etc.), as well as on the

broader wellness industry and concept.

Desk research was supplemented by over 30 interviews conducted with industry

leaders in the spa industry, industry leaders in other wellness lifestyle sectors, related

industry associations and organizations, and leading organizations and ―thinkers‖ on

the concept of wellness.

In addition to the interviews, the SRI team, in partnership with GSS, developed two

short surveys that were distributed more broadly to spa stakeholders and consumers

around the world. The questionnaires queried industry and consumers about their views

on wellness – both as a concept and as a trend – in relationship to business planning,

purchasing patterns, and lifestyle.

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 3 SRI International

II. WELLNESS AS A CONCEPT

A. History of Wellness

Wellness is a modern word with ancient roots. As a modern concept, wellness has

gained currency since the 1950s, 1960s, and 1970s. The writings and leadership of

an informal network of physicians and thinkers in the United States have largely

shaped the way we conceptualize and talk about wellness today.

The origins of wellness, however, are much

older – even ancient. Aspects of the wellness

concept are firmly rooted in several

intellectual, religious, and medical movements

in 19

th

century United States and Europe. The

tenets of wellness can also be traced to the

ancient civilizations of Greece, Rome, and Asia. Historical traditions have indelibly

influenced the modern wellness movement, and details regarding the history of

wellness as a concept and as a term are provided in Appendix A.

Ancient Antecedents of Wellness

Modern definitions of wellness typically focus on holistic or integrated approaches to

health; staying well (or the prevention of sickness); self-responsibility for one’s health

and well-being; and the idea that a person’s physical, mental, and spiritual aspects

should work in harmony. These tenets are clearly not new, and in fact have their

According to the Oxford English

Dictionary, the first written appearance

of the word wellness in the English

language was in 1654.

3,000-

2,000

BC

Traditional Chinese Medicine (TCM), one of the oldest systems of medicine in the world, develops.

Influenced by ancient philosophies of Taoism and Buddhism, it applies a holistic perspective to

achieving health and well-being through the cultivation of harmony within one’s life. Therapies that

evolve out of TCM – such as acupuncture, herbal medicine, qi gong, tai chi – are not only still in

practice, but are also increasingly being integrated into Western medical practices.

3,000-

1,500

BC

Ayurveda originated as an oral tradition and was recorded in the Vedas, four sacred Hindu texts.

Ayurveda is holistic and strives to create harmony between the body, mind, and spirit, maintaining a

balance that prevents illness and contributes to a long, healthy life. Ayurveda’s regimens are tailored

to each person's unique constitution, taking into account his or her needs for nutrition, exercise, personal

hygiene, social interaction, and other lifestyle elements. From India also originated mind-body-spirit

traditions such as yoga and meditation, which are increasingly practiced in modern, Western cultures.

500-

300

BC

Ancient Greek physician Hippocrates – considered to be the father of Western medicine – is

possibly the first physician to focus on preventing sickness instead of just treating disease, and also

argued that disease is product of diet, lifestyle, and environmental factors.

50

BC

Ancient Roman medicine emphasized the prevention of disease over curing disease and adopted

the Greek belief that disease was a product of diet and lifestyle. Ancient Rome had a highly

developed public health system, and the extensive system of aqueducts, sewers, and public baths

helped prevent the spread of germs and maintain the health of the population.

Timeline of Wellness

Ancient Antecedents of Wellness

Note: A more extensive version of this timeline, including sources, is provided in Appendix A.

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 4 SRI International

origins in ancient healing practices and medical traditions that date back thousands of

years. The ancient cultures of China, India, Greece, and Rome (among others) had a

very sophisticated understanding of how to maintain health, and they tended to

emphasize a ―whole person‖ or ―harmonious‖ approach to staying well. Today, the

concept of wellness appears to be coming full-circle, with modern iterations of ancient

practices – such as ayurveda, acupuncture, yoga, meditation, and so on – growing

increasingly popular around the world and becoming central components of wellness-

oriented approaches to health.

19

th

Century Intellectual and Medical Movements

In the 19

th

century, new intellectual movements, spiritual philosophies, and medical

practices proliferated in the United States and Europe. A number of alternative

healthcare methods that focus on self-healing, holistic approaches, and preventive

care – including homeopathy, osteopathy, chiropractic, and naturopathy – were

founded during this era and gained widespread popularity in both Europe and the

United States. Other new philosophies were more spiritually oriented (such as the

―mind-cure movements,‖ including New Thought and Christian Science) and were

instrumental in the modern era in propagating the idea that one of the primary

sources of physical health is one’s mental and spiritual state of being.

1790s Homeopathy was developed by German physician Samuel Christian Hahnemann and uses natural

substances to promote the body’s self-healing response.

Timeline of Wellness

19

th

Century Intellectual & Medical Movements

1860s German priest Sebastian Kneipp promoted his own healing system (―Kneipp Cure‖), combining

hydrotherapy with herbalism, exercise, nutrition, and spirituality.

1870s Mary Baker Eddy, founder of Christian Science, began practicing spiritual healing.

Osteopathy was founded by Andrew Taylor Still, emphasizing a noninvasive, holistic approach.

1890s Horace Fletcher, a health food faddist, emphasized proper chewing of food and a low-protein diet.

1900s John Harvey Kellogg directed the Battle Creek Sanitorium in Michigan (U.S.) and espoused a healthy

diet, exercise, fresh air, hydrotherapy, and ―learning to stay well.‖

1910 Carnegie Foundation’s Flexner Report sets the stage for the rise of modern, evidence-based, disease-

oriented medicine.

Chiropractic was founded by Daniel David Palmer, focusing on the body’s structure and functioning.

Naturopathy, originating in Europe and then spreading to the U.S., emphasizes the body’s ability to

heal itself through dietary and lifestyle changes, herbs, massage, and joint manipulation.

The New Thought Movement emerged, and Phineas Quimby developed theories about mentally-

aided healing.

Austrian philosopher Rudolf Steiner developed the spiritual movement of anthroposophy along with a

holistic and wellness-focused system of anthroposophical medicine.

1880s Swiss physician Maximilian Bircher-Benner, ran a Swiss sanitorium, pioneered nutritional research

and advocated a balanced diet of fruit and vegetables.

YMCA, one of the world’s oldest wellness organizations, adopted its triangle logo and the principle

of developing body, mind, and spirit.

Austrian F.X. Mayr developed his own detoxification and therapeutic dietary modification program

(―Mayr Therapy‖).

Note: A more extensive version of this timeline, including sources, is provided in Appendix A.

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 5 SRI International

While a few of the beliefs espoused by the thinkers behind these movements have

been discredited or would seem ―wacky‖ today, these movements did popularize

ideas about regaining or maintaining one’s health through diet, exercise, and other

lifestyle measures. The philosophies embodied in these 19

th

century movements – that

a healthy body is a product of a healthy mind and spirit – are now considered to be

precursors to today’s popular wellness and self-help movements. In addition, although

these medical approaches fell out of favor with the rise of modern, evidence-based

medicine in the mid-20

th

century, several of them are now regaining favor within the

mainstream medical community and the general public.

20

th

Century Popularization of Wellness

Our modern use of the word ―wellness‖ dates to the 1950s and a seminal – but little

known – work by physician Halbert L. Dunn, called High-Level Wellness (published in

1961). Although Dunn’s work received little attention at the time, his ideas were later

embraced and expanded upon in the 1970s by an informal network of individuals in

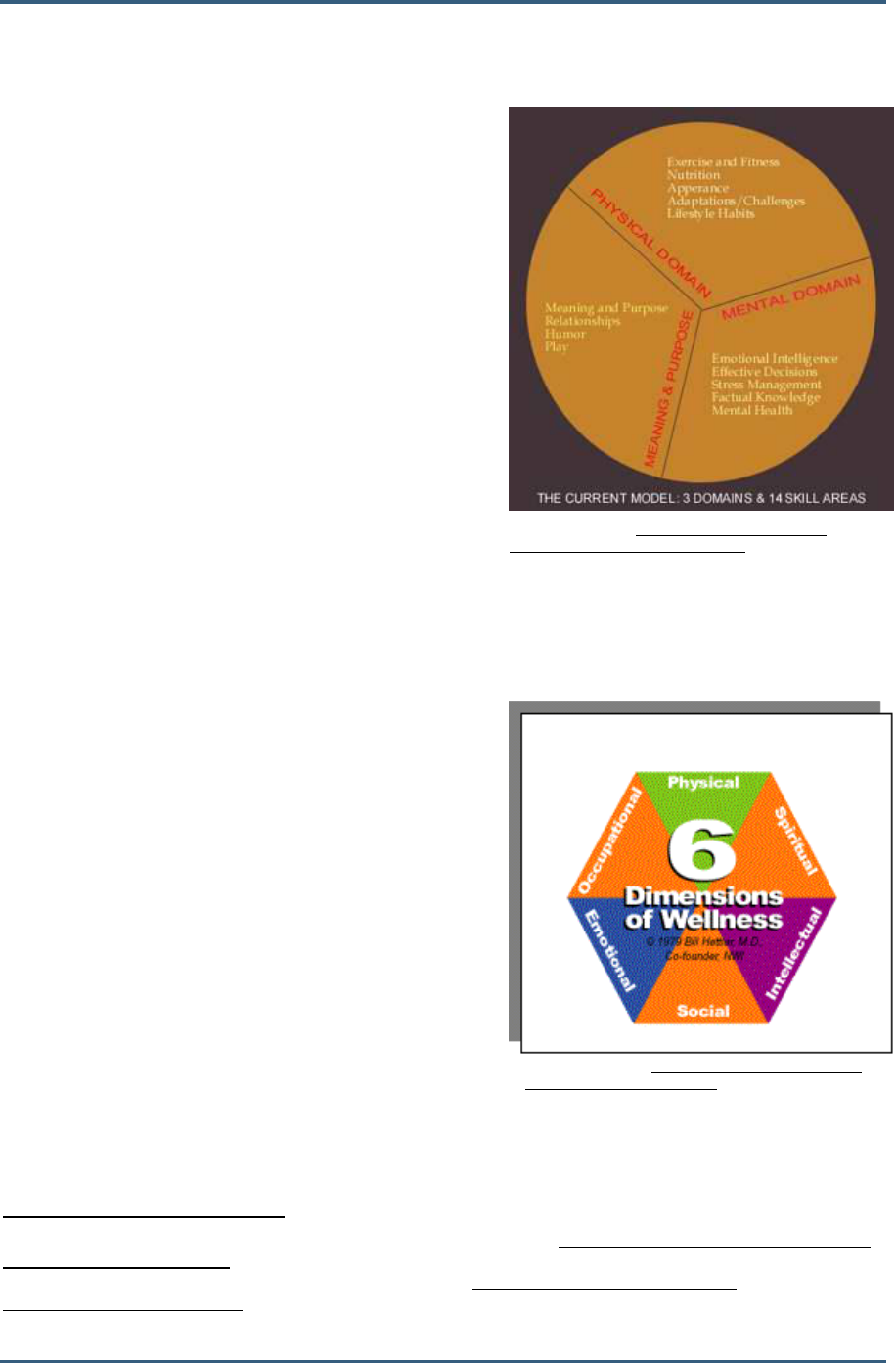

the United States, including Dr. John W. Travis, Don Ardell, Dr. Bill Hettler, and others.

These ―fathers of the wellness movement‖ created their own comprehensive definitions

and models of wellness, developed new wellness assessment tools, and wrote and

spoke actively on the concept of wellness. Travis, Ardell, Hettler, and their associates

were responsible for creating the world’s first wellness center, developing the first

1950s-

1960s

Physician Halbert L. Dunn presented his idea of ―high level wellness‖ in a series of 29 lectures, and

then published these talks in a book called High Level Wellness. Dunn is known as the ―father of the

wellness movement,‖ and his work subsequently caught the attention of – and was further

developed by – several other physicians and intellectuals.

Timeline of Wellness

20

th

Century Popularization of Wellness

Note: A more extensive version of this timeline, including sources, is provided in Appendix A.

1970s Dr. John W. Travis, who was influenced by Dunn’s writings, founded the world’s first wellness center

in California, developed a 12-dimension wellness assessment tool (the Wellness Inventory, 1975), and

wrote and published The Wellness Workbook (1977). These are still in use today as foundational tools

for wellness development.

Don Ardell, also influenced by Dunn’s work, published in 1977 his book High Level Wellness: An

Alternative to Doctors, Drugs, and Disease, borrowing the title and concepts from Dunn. Ardell wrote 12

other books on wellness has been a leading figure in the wellness movement for over three

decades, speaks at numerous health and wellness conferences, and publishes a weekly newsletter, the

Ardell Wellness Report.

The University of Wisconsin-Stevens Point (UWSP) drew upon wellness materials from John W.

Travis started the first university-based campus wellness center. Campus wellness programs

became popular and spread throughout the United States in the 1970s and 1980s, and these were

influential in the spread of the wellness movement.

Dr. Bill Hettler of UWSP built on John W. Travis’ materials and created his own Lifestyle Assessment

Questionnaire, as well as a six-dimensional model of wellness. Along with his colleagues at UWSP,

Hettler organized the National Wellness Institute in 1977 and the first National Wellness

Conference in 1978.

1980s-

2000s

As the wellness movement spread, businesses in the United States began developing workplace

wellness programs, the spa and fitness industries experienced rapid growth, and a number of

celebrities and self-help experts started bringing wellness concepts to a mainstream audience;

however, these developments have not yet coalesced under the banner of the wellness industry.

1950s J.I. Rodale is one of the first advocates of organic farming in the U.S. and begins publishing

Prevention magazine, a pioneering publication in promoting alternative/preventive health.

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 6 SRI International

university campus wellness center, and establishing the National Wellness Institute and

National Wellness Conference in the United States.

The popularization of the wellness concept during the 1970s and 1980s led to the

spread of worksite wellness programs at major corporations, as well as to the

development of government-sponsored programs to promote healthier lifestyles in a

number of U.S. states and cities. The modern concept of wellness also spread to

Europe, where the German Wellness Association (Deutscher Wellness Verband, DWV)

and the European Wellness Union (Europäischen Wellness Union, EWU) were founded

in 1990. Although the ideas of the true wellness pioneers (Dunn, Travis, Ardell, Hettler,

and so on) still have not reached the mainstream or achieved mass recognition, new

theories about healthy-living, self-help, well-being, fitness, diet, and spirituality

continue to proliferate today. Many of the medical and self-help experts who promote

these ideas in today’s popular media (largely in the United States) – ranging from

Michael Roizen

1

, Mehmet Oz

2

, and Andrew Weil

3

to Deepak Chopra

4

Stephen

Covey

5

, and Wayne Dyer

6

– can be linked to the wellness movement.

B. Defining Wellness

There are a number of rigorous and well-

thought-out definitions of wellness,

developed over time by the leading

thinkers in the field. In particular, each of

the ―founding fathers of wellness‖ has

developed his own wellness definition and

model (see Appendix A for details). In fact, it was the process of attempting to define,

understand, and measure wellness during the 1950s-1970s that initially led to the

propagation of the concept in the modern era. As such, this report will not attempt to

craft a new definition of wellness for the spa industry, but will instead briefly

summarize several of the best-known and most respected definitions, as well as the

varying views on wellness across different regions of the world. While recognizing that

there are regional variations in the concept of wellness (discussed in Appendix A),

1

American physician, chief wellness officer at the Cleveland Clinic, developer of the ―Real Age‖ concept, and

award-winning author.

2

Turkish-American surgeon and promoter of alternative medicine, author of a number of award-winning books

on health topics, frequent contributor to the Oprah Winfrey Show, and host of his own television talk show.

3

American physician known for establishing and popularizing the field of integrative medicine and author of

several best-selling books on healthy eating, aging, and related topics.

4

Indian-American physician, promoter of alternative and mind-body medicine, and author of over 45 books on

New Age spirituality and alternative medicine.

5

Author of the best-selling book The Seven Habits of Highly Effective People.

6

American self-help ―guru,‖ lecturer, and author of over 30 books (such as The Power of Intention).

Wellness is:

The state of being well or in good health.

(Oxford English Dictionary)

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 7 SRI International

several common threads stand out across the various definitions of wellness. These

include:

Wellness is multidimensional: Most of the

leading definitions of wellness include a

model that presents anywhere from 2 to

14 or more dimensions, which frequently

include physical, mental, spiritual, and

social dimensions.

Wellness is holistic: Wellness is a broader concept than physical health or fitness,

focusing on the well-being of the whole person. It is not simply the absence of

physical disease, but an approach that emphasizes all aspects of a person – body,

mind, and spirit – working in harmony.

Wellness changes over time and along a continuum: Wellness is not a static state or

an end-point, but rather is often depicted on a continuum representing the optimum

levels of wellness that an individual attempts to achieve and maximize throughout

his or her life.

Wellness is individual, but also influenced by the environment: Wellness is a process

pursued on the individual level, by engaging in healthy behaviors and practices

that promote personal well-being. However, personal wellness is also influenced

by the conditions or environment in which one lives. With the increasing emphasis

today on environmental problems, there is also increasing attention on the

environmental, external, cultural, and global aspects of wellness.

Wellness is a self-responsibility: Although sick people typically rely on medical

doctors for treatment to fix a problem and return to good health, most advocates

of wellness philosophies emphasize each individual’s responsibility to take charge

of one’s own health and to engage in behaviors that will proactively prevent illness

and promote a higher level of health and well-being.

Health is:

A state of complete physical, mental and

social well-being and not merely the

absence of disease or infirmity.

(World Health Organization)

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 8 SRI International

There are a number of terms and concepts that are associated or equated with the

wellness movement, but which are in fact distinct ideas. These related terms, and brief

definitions, are encapsulated in the following box.

Wellness-Related Terms

Health: Is commonly defined as the presence or absence of disease, or the soundness/vigor of body or

mind. The World Health Organization’s definition (adopted in 1948) – ―Health is a state of complete

physical, mental and social well-being and not merely the absence of disease or infirmity‖

7

– is

significant in the fact that it goes beyond just the physical state of freedom from disease and

emphasizes a positive state of being that includes mental and social dimensions.

Preventive Medicine: The goal of preventive medicine ―is to protect, promote, and maintain health and

well-being and to prevent disease, disability, and death. Preventive medicine specialists [are

specialists who] have core competencies in biostatistics, epidemiology, environmental and occupational

medicine, planning and evaluation of health services, management of health care organizations,

research into causes of disease and injury in population groups, and the practice of prevention in

clinical medicine.‖

8

Integrative (or Integrated) Medicine: Combines treatments from conventional/mainstream medicine and

complementary and alternative medicine (CAM) for which there is high-quality scientific evidence of

safety and effectiveness.

9

Holistic Health: Is ―an approach to life. Rather than focusing on illness or specific parts of the body, [it]

considers the whole person and … emphasizes the connection of mind, body, and spirit. The goal is to

achieve maximum well-being … [and] people accept responsibility for their own level of well-

being.‖

10

Holistic Medicine: Is ―the art and science of healing that addresses care of the whole person – body,

mind, and spirit. The practice of holistic medicine integrates conventional and complementary therapies

to promote optimal health, and prevent and treat disease by addressing contributing factors.‖

11

Personalized Medicine: Involves the systematic use of information about individual patients – especially

genetic and molecular analysis – to optimize the treatment or prevention of disease. The aim is ―to

achieve optimal medical outcomes by helping physicians and patients choose the disease management

approaches likely to work best in the context of a patient’s genetic and environmental profile.‖

12

7

World Health Organization, Preamble to the Constitution of the World Health Organization as adopted by the

International Health Conference, New York, 19-22 June, 1946; signed on 22 July 1946 by the representatives of

61 States (Official Records of the World Health Organization, no. 2, p. 100) and entered into force on 7 April

1948, http://www.who.int/about/definition/en/print.html, accessed March 28, 2010.

8

―What Is Preventive Medicine?‖ American Board of Preventive Medicine Website, https://www.theabpm.org/

aboutus.cfm, accessed March 31, 2010.

9

―What Is CAM?‖ National Center for Complementary and Alternative Medicine, National Institutes of Health

Website, http://nccam.nih.gov/health/whatiscam/overview.htm, accessed March 31, 2010.

10

Suzan Walter, ―Holistic Health,‖ The Illustrated Encyclopedia of Body-Mind Disciplines, Ed. Nancy Allison, The

Rosen Publishing Group, 1999, http://ahha.org/articles.asp?Id=85, accessed March 28, 2010.

11

―Frequently Asked Questions,‖ American Holistic Medicine Association Website,

http://www.holisticmedicine.org/displaycommon.cfm?an=1&subarticlenbr=5, accessed March 28, 2010.

12

―Personalized Medicine 101,‖ Personalized Medicine Coalition Website, http://www.

personalizedmedicinecoalition.org/sciencepolicy/personalmed-101_overview.php, accessed April 10, 2010.

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 9 SRI International

Wellness-Related Terms (continued)

Public Health: Is ―the science and art of preventing disease, prolonging life, and promoting health

through the organized efforts and informed choices of society, organizations, public and private,

communities, and individuals."

13

Public health efforts typically focus on prevention of disease, health

education, and reduction of risk factors at the societal (not individual) level.

Health Promotion: The WHO defines health promotion as ―the process of enabling people to increase

control over their health and its determinants, and thereby improve their health.‖

14

The concept is most

commonly applied in the public health or public policy context, but is also now linked with worksite-

based health and wellness programs.

Health Education: ―Comprises consciously constructed opportunities for learning involving some form of

communication designed to improve health literacy, including improving knowledge, and developing

life skills which are conducive to individual and community health.‖

15

13

C.E.A. Winslow, ―The Untilled Fields of Public Health,‖ Science, n.s. 51 (1920), p. 23 (as cited in Wikipedia

entry on ―Public Health,‖ accessed April 10, 2010).

14

World Health Organization, The Bangkok Charter for Health Promotion in a Globalized World, Geneva,

Switzerland: WHO, 2005, http://www.who.int/healthpromotion/conferences/6gchp/

hpr_050829_%20BCHP.pdf.

15

World Health Organization, Health Promotion Glossary, Geneva, Switzerland: WHO, 1998,

http://www.who.int/hpr/NPH/docs/hp_glossary_en.pdf.

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 10 SRI International

III. WELLNESS AS AN INDUSTRY

A. Drivers of the Growing Wellness Market

Much like the word ―spa,‖ the word ―wellness‖ has seen increasing usage, especially

for marketing and advertising purposes, without regard for its deeper meaning. This

has led many spa, health, and other professionals to dismiss it as just another passing

fad. However, like the word spa, wellness is grounded in a solid historical tradition

and body of knowledge, and trends indicate that it is becoming a major societal force.

In many ways, the thinkers behind the wellness theories and models developed in the

19

th

and 20

th

centuries were merely ahead of their time.

While wellness, as a word and a concept, is only hazily understood by most

mainstream consumers, the many challenges society faces today are driving people to

explore new wellness-related products and services as they realize a need to find a

better way to take care of themselves. Recognition and acceptance of wellness-

related theories and practices is growing rapidly, even if these are not formally

labeled under the wellness banner.

Below, we summarize three megatrends driving the growth of wellness as an industry.

These trends not only directly impact the spa industry and its customers, but are also

opening new opportunities for spas to play a leading role in the paradigm shift that

the leaders of the wellness movement have recommended over the last several

decades.

Megatrends Driving Growth of the Wellness Industry Cluster

Growing

Wellness

Market

Failing

medical

systems

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 11 SRI International

Increasingly older, unhealthy people

The United Nations describes the aging of

our population as ―unprecedented.‖

16

In the

populations of the more developed

countries, older people (60 and older)

began to outnumber children (under 15) in 1998. Worldwide, older people are

expected to outnumber children for the first time in 2047. By 2050, the United Nations

predict that 22% of the world’s population will be over 60, double the percentage in

2007.

17

Within this population of 60 and over, the fastest growing group is that of 80

and over. With age typically comes decreasing physical health and mounting medical

costs.

The increasing number and proportion of the aged within the world’s population

foreshadows greater numbers of older and, potentially, sicker people in need of care,

as well as fewer younger, able-bodied family members and/or workers available to

care for them. Indications are that these numbers and proportions will also start to

grow faster in less developed regions, forcing these countries to deal with increased

demand for care without the economic resources of the more developed regions.

Leading the wave of the aging in the North America, Europe, Japan, and other

countries are the famous Baby Boomers,

18

who vocally demand to have their needs

met and are willing to experiment with new ways to solve their problems.

It is also a sicker world. Although people are

living longer, they are more likely to be

living with and dying from a chronic illness,

frequently caused, in part, by their own

behaviors and lifestyles. According to the

World Health Organization, in 2005, these

chronic diseases were the major cause of

death and disability worldwide.

19

Conditions

such as cardiovascular diseases (mostly heart attack and stroke), diabetes, obesity,

cancer, and respiratory diseases accounted for almost 60% of the 57 million deaths

annually and 46% of the global burden of disease.

20

Deaths from these diseases are

16

United Nations, World Population Ageing 2007, http://www.un.org/esa/population/publications/WPA2007/

wpp2007.htm, p. xxvi.

17

Ibid.

18

Baby Boomers are persons born in the post-World War II ―baby boom‖ in both North America and Europe, as

well as Japan, Australia, and New Zealand, roughly 1946-1964.

19

World Health Organization, Information sheet: Facts related to chronic diseases and the WHO global strategy

on diet, physical activity and health, 2003, http://www.who.int/dietphysicalactivity/media/en/gsfs_general.pdf.

20

The WHO global burden of disease (GBD) measures burden of disease using the ―disability-adjusted life

year‖ or DALY. This measure combines years of life lost due to premature death and years of life lost due to

“It is an older world.”

(Halbert L. Dunn)

“The world has a problem: It is getting hot,

flat, and crowded … How we address these

interwoven global trends will determine a

lot about the quality of life on earth in the

twenty-first century.”

(Thomas L. Friedman)

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 12 SRI International

expected to increase by 17% over the next 10 years, largely because of the aging

population and an increased exposure to risk factors.

As the world has become more industrial and more urbanized, and as food markets

have become more global, diets have become less healthy, lifestyles less active, and

smoking more prevalent. These behaviors often lead to obesity, high blood pressure,

high glucose levels, and high cholesterol, which, either alone or in combination, are the

major causes of chronic diseases such as those listed in the table below.

Causes of Chronic Diseases

Modifiable Risk Factors

Intermediate Risk Factors

Major Chronic

Diseases

Smoking

Physical

activity

Diet

Stress

Alcohol

High blood

pressure

High glucose

levels

High

cholesterol

Obesity

Chronic heart disease,

stroke

Cancer

Diabetes

Respiratory disease

Source: Adapted from WEF/PWC, Working Towards Wellness, 2007, http://www.weforum.org/pdf/Wellness/report.pdf, Figure 4.

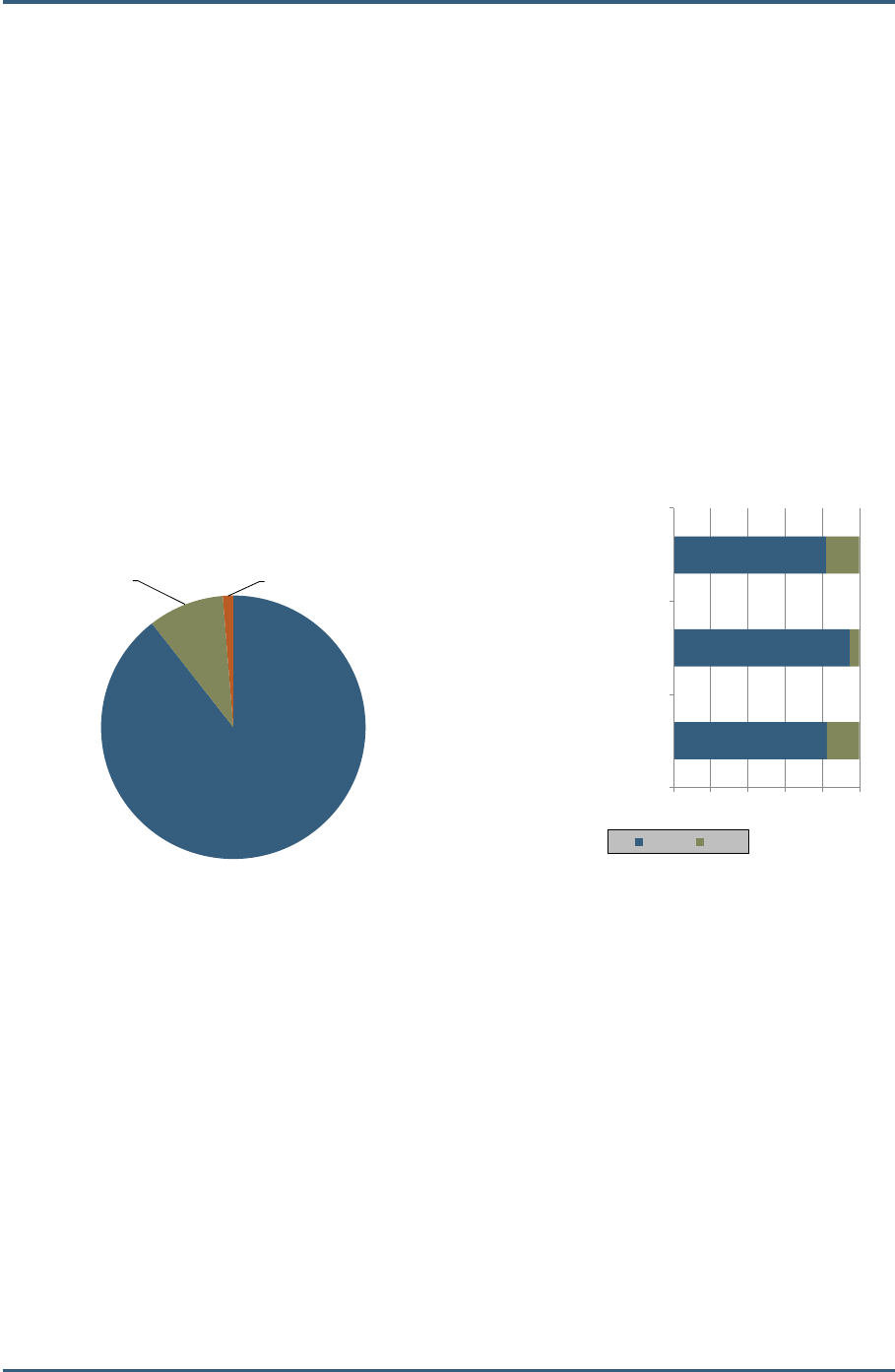

Obesity, which contributes to cancer, heart disease, diabetes, and respiratory disease,

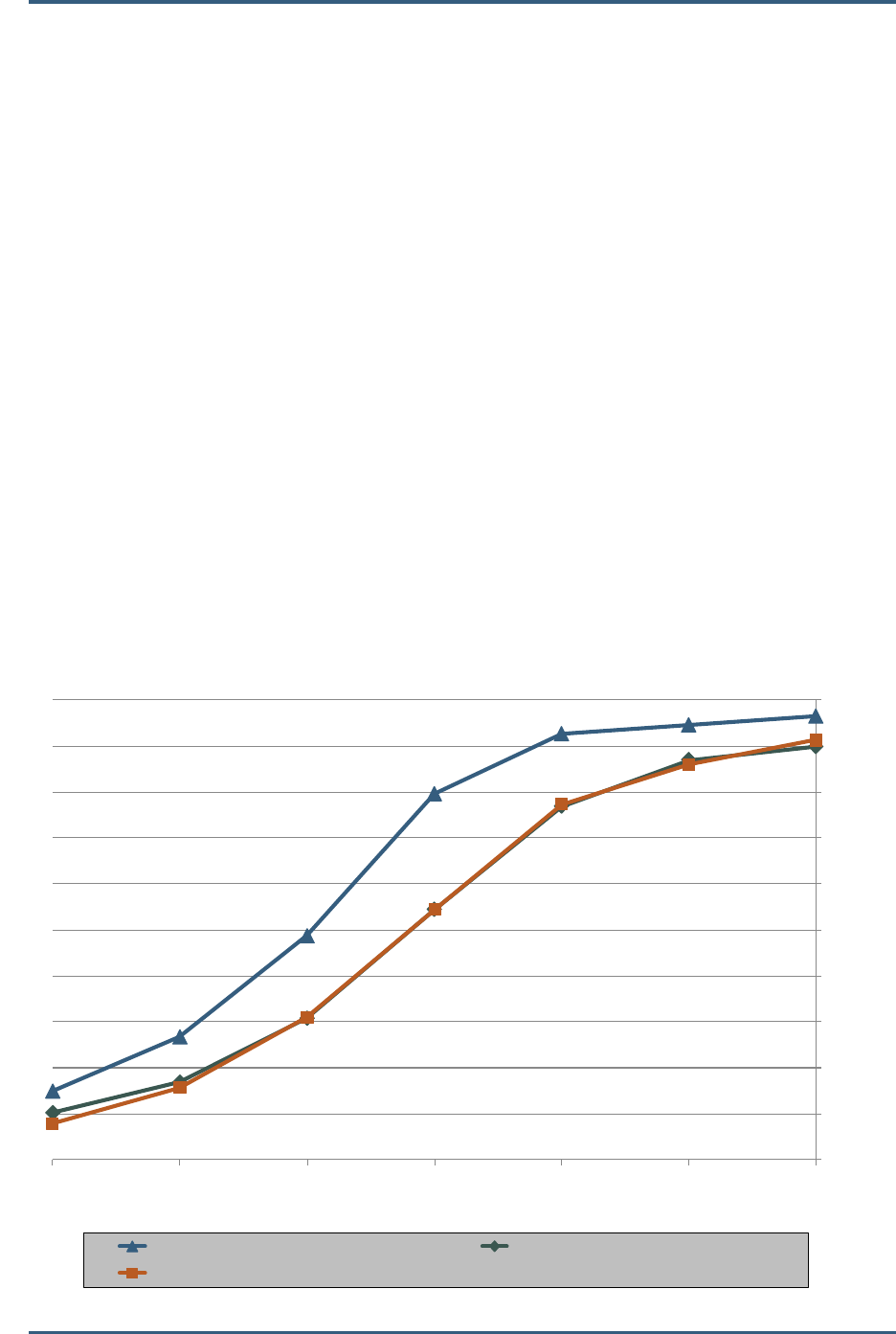

is a worldwide problem. More than half the adults in Brazil, the United Kingdom, and

the United States are overweight or obese, and rates are expected to increase (see

the graph below).

The burden of disease for a chronic illness can be high and long-lasting, as people live

for many years in ill-health, requiring extensive medical services, before finally dying.

The mind-boggling point, though, is that a well-established body of research

demonstrates that these diseases and their costs in suffering and dollars are largely

preventable with changes in diet, increased levels of physical activity, and abstinence

from smoking. Up to 80% of cases of coronary heart disease, 90% of type 2 (adult-

onset) diabetes cases, and one-third of cancers can be avoided by changing to a

healthier diet, increasing physical activity, and stopping smoking.

21

time lived in states of less than full health. The DALY metric was developed in the original GBD 1990 study to

assess the burden of disease consistently across diseases, risk factors, and regions.

21

WHO, Information sheet: Facts related to chronic diseases.

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 13 SRI International

In addition to broader health issues, concerns about ―the limits to growth‖ with regards

to energy resources and environmental sustainability have become mainstream, and, in

many instances, governments, businesses, and consumers are changing their behaviors

to address these. A snapshot of this reaction is captured by the rise of the LOHAS

market and the LOHAS consumer.

In addition to growing environmental concerns, today’s consumers are also suffering

from the mounting pressures of our modern society: increasingly hectic schedules; a

lack of true leisure time; the pressures of being in constant contact with the office,

family, and friends by email, mobile phone, or PDA (even while on vacation); a

constant barrage of information and external stimulation through multiple media

(television, radio, Internet, and so on). These kinds of pressures not only increase stress,

but also contribute to unhealthy behaviors, such as poor eating habits, lack of sleep,

and lack of exercise – ultimately contributing to the rise of chronic, preventable

conditions like obesity. In response, some people are starting to take a step back,

reassess how they live their lives, and look for more inner fulfillment and deeper

meaning in their lives.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2005

2015

2005

2015

2005

2015

2005

2015

2005

2015

2005

2015

% of population ages 15 and over

Percent of population (ages 15 and over) who are overweight or obese

(BMI ≥ 25 kg/m

2

)

Obese

Overweight

Brazil

China India

South Africa

UK

US

Source: WHO data, adapted from WEF/PWC, Working Towards Wellness, Figure 6.

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 14 SRI International

Failing medical systems

Globally, health systems are failing to meet

the challenges of caring for a growing

number of aging and chronically ill patients.

From region to region, specific problems vary

but mainly involve widespread problems with

cost, availability, and quality of care, as well

as an ongoing emphasis on treating rather

than preventing sickness. As the world’s

population grows older and sicker over the long term, medical systems seem less and

less able to care for them. Consumers, healthcare providers, and governments are

increasingly looking for a better way.

The current healthcare industry model,

based on the paradigm of conventional

Western medicine, is increasingly seen to be

broken – a model that costs too much and

delivers too little. A 2007 survey by the

Kaiser Family Foundation and Pew Global

Attitudes Project, conducted in 47 countries

around the world, found that people ranked

concerns about health a close second, behind financial issues, when asked to name the

most important problems that they and their families currently face. In one country out

of two, personal illness, health-care costs, poor quality care, or other health issues

were the top personal concerns of over one-third of the population surveyed.

22

And

yet, spending on health is increasing. In 2002, the cumulative health spending of 24

OECD countries was $2.7 trillion; this is expected to more than triple to $10 trillion by

2020.

23

The World Health Organization’s World Health Report 2008 describes three trends

that contribute to problems in what it calls ―conventional healthcare,‖ and what others

have dubbed the ―sickness industry‖

24

:

1. Hospital-centrism: An excessive focus on care delivered in hospitals and by

specialists, which is expensive. While high-income countries are most likely to face

this issue, middle- and low-income countries are following in their footsteps, with

the numbers of medical specialists increasing rapidly.

22

Kaiser Family Foundation and Pew Global Attitudes Project, A Global Look at Public Perceptions of Health

Problems, Priorities, and Donors: The Kaiser/Pew Global Health Survey, 2007, http://www.kff.org/kaiserpolls/

upload/7716.pdf, p. 14.

23

PWC, HealthCast 2020, p. 3.

24

Paul Zane Pilzer in The Wellness Revolution, and others.

“Conventional approaches are failing,

even in the most advanced nations of

the world – throughout Europe, Asia,

the Middle East, Australia, Canada and

the United States.”

(PricewaterhouseCoopers)

“At the current rate of consumption and at

the current level of thinking, the healthcare

organizations of today will be unable to

meet demand in the future. Our health

systems will be unsustainable.”

(PricewaterhouseCoopers)

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 15 SRI International

2. Fragmented and fragmenting care: Medical specialists are more likely to focus on a

narrow section of a patient’s health rather than taking a holistic approach to the

patient, his or her family, and environment. Public or private programs aimed at

preventing or controlling a condition – such as obesity, diabetes, cancer, or heart

disease – also focus solely on the issue of choice, to the exclusion of other factors

that may contribute to wellness or illness.

3. Commercialization: As patients are frustrated with the inability of ―official‖ health

systems (i.e., services and facilities provided by governments or reimbursed by

insurance), other providers enter the less regulated market for out-of-the-patient’s-

pocket services. While some providers offer valuable, needed services, others take

advantage of less regulation and desperate situations to provide less than

effective care at less than fair prices.

In describing these trends, the WHO states, ―At the same time, the health sector lacks

the expertise to mitigate the adverse effects on health from other sectors and make

the most of what these other sectors can contribute to health.‖

25

Perhaps in reaction to

these widespread problems, many industry and thought leaders interviewed for this

study referred to a growing sense of ―self-responsibility‖ among individuals with

regard to maintaining their own health, stemming from a realization that the current

healthcare system is failing them and cannot be trusted to take care of them. This may

be driving people to engage in proactive healthy behaviors and to investigate

alternative forms of healthcare.

For instance, in the United States, many

prominent medical experts, frustrated by

the shortcomings of their tools and training,

have begun to investigate alternative

treatments and preventive techniques and

are submitting these methods to the

rigorous investigation of the scientific method. Meanwhile, in 1991 the U.S. National

Center for Complementary and Alternative Medicine was established (as part of the

government-funded National Institutes of Health) and in 2010 will spend $129 million

to study the effectiveness of complementary and alternative treatments, including, but

not limited to: acupuncture, osteopathy, traditional Chinese medicine and other herbal

medicines, massage, tai chi, yoga, meditation, and mindfulness-based interventions.

26

Globally, as witnessed by the focus of recent WHO reports mentioned above,

governments and public health officials are also seeking better solutions and seeking

25

WHO, World Health Report 2008, p. xiv.

26

―About NCCAM,‖ National Center for Complementary and Alternative Medicine, National Institutes of Health

Website, http://nccam.nih.gov/about/, accessed April 9, 2010.

“Few would disagree that health systems

need to respond better – and faster – to

the challenges of a changing world.”

(World Health Organization)

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 16 SRI International

to tap into prevention. Employers are also entering the fray, mainly in response to

three factors:

The looming cost increases presented by aging, sedentary, and chronically-ill

employees, both in terms of healthcare expenses and lost productivity, threaten to

undermine profits.

The active workforce, especially in the OECD countries, accounts for 54% of the

global population and are easier to target, given the amount of time they spend in

the workplace.

Well-documented evidence indicates, conservatively, that workplace wellness

programs – if implemented correctly – yield a return on investment of as much as

3:1 or more.

27

Globalization and connection

As the costs and time needed to move

people, products, and information continue

to shrink, we are all exposed to more of

everything. With regards to health and

wellness, this contraction of the globe has

both negative and positive effects.

On the negative side, the World Health Organization talks about a worldwide

―nutrition transition,‖ whereby more people around the world are eating diets high in

total energy, fats, salt, and sugar, brought about, in part, by increased production,

promotion, and marketing of processed foods.

28

In developed countries, a growing

number of consumers – who tend to be highly educated and wealthy – have begun to

reject this transition and to return to healthier ways of eating. These consumers’ habits

are not mainstream, although they may presage a coming global trend.

Immigration and migration to cities is leading to more urban lifestyles, accompanied

by fewer opportunities for exercise and less time to prepare healthy food. For the

educated elite, these transitions can lead to increased business travel and the endless

business day, where the worker is expected to be ―on call,‖ in multiple time zones,

accessible by cell phone and PDA.

On a more positive note, the contraction of time and space inherent in more connection

opportunities leads to a greater exposure for different approaches to healthcare and

to wellness. Aspiring scientists, physicians, and nurses from less-developed countries

27

WEF/PWC, Working towards Wellness, p. 16.

28

WHO, Information sheet: Facts related to chronic diseases.

“It is a shrinking world.”

(Halbert L. Dunn)

Spas and the Global Wellness Market Synergies and Opportunities

© Copyright Global Spa Summit 2010 17 SRI International

come to more developed countries to study, bringing about a cross-pollination as they

bring their health and wellness traditions with them, and returning to their home

countries with Western knowledge and expertise. Travelers are exposed to local

practices, and immigrants living in new countries bring the healing tools of their culture.

Moreover, a patient may travel to India from the West to receive cheaper

―traditional‖ cardiac care, perhaps from an Indian physician trained in the United

States, and be introduced to ayurveda and yoga while there.