F-5

Schedule A – Itemized Deductions

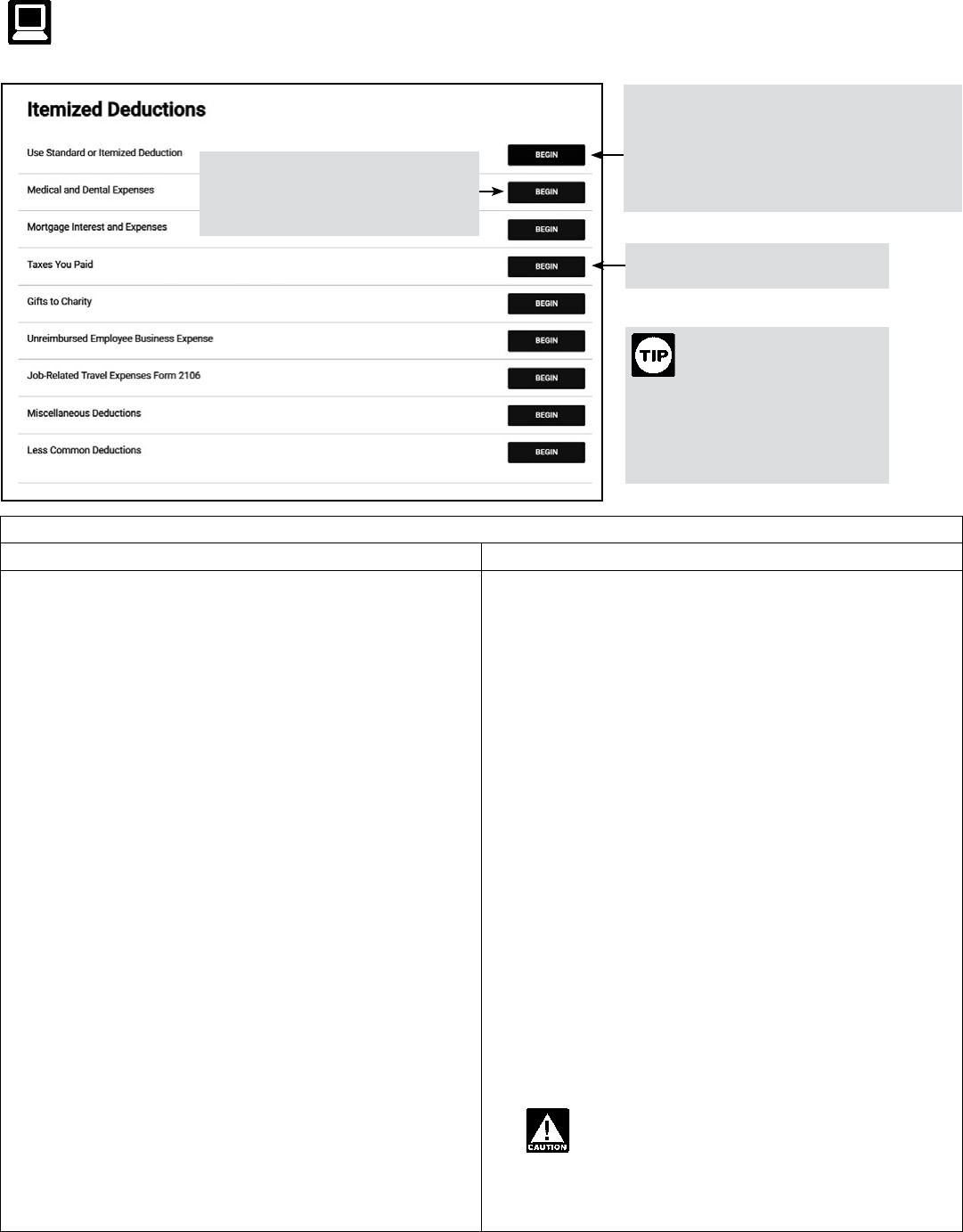

TaxSlayer Navigation: Federal Section>Deductions>Itemized Deductions>Medical and Dental Expenses

Schedule A Deductible and Nondeductible Medical Expenses

You can include: You can’t include:

• Bandages

• Birth control pills prescribed

by your doctor

• Body scan

• Braille books

• Breast pump and supplies

• Capital expenses for

equipment or improvements

to your home needed

for medical care (see

Worksheet A, Capital

Expense Worksheet, in Pub.

502)

• Diagnostic devices

• Expenses of an organ donor

• Eye surgery (to promote the

correct function of the eye)

• Fertility enhancement,

certain procedures

• Guide dogs or other animals

aiding the blind, deaf, and

disabled

• Hospital services fees (lab

work, therapy, nursing

services, surgery, etc.)

• Lead-based paint removal

• Legal abortion

• Legal operation to prevent

having children such as a

vasectomy or tubal ligation

• Long-term care contracts,

qualied

• Meals and lodging provided

by a hospital during medical

treatment

• Medical services fees (from

doctors, dentists, surgeons,

specialists, and other

medical practitioners)

• Medicare Part D premiums

• Medical and hospital

insurance premiums

• Nursing services

• Oxygen equipment and

oxygen

• Part of life-care fee paid to

retirement home designated

for medical care

• Physical examination

• Pregnancy test kit

• Prescription medicines

(prescribed by a doctor) and

insulin

• Psychiatric and

psychological treatment

• Social security tax, Medicare

tax, FUTA, and state

employment tax for worker

providing medical care (see

Wages for nursing services

below)

• Special items (articial limbs,

false teeth, eyeglasses,

contact lenses, hearing aids,

crutches, wheelchair, etc.)

• Special education for

mentally or physically

disabled persons

• Stop-smoking programs

• Transportation for needed

medical care

• Treatment at a drug or

alcohol center (includes

meals and lodging provided

by the center)

• Wages for nursing services

• Weight loss, certain

expenses for obesity

• Baby sitting and childcare

• Bottled water

• Contributions to Archer

MSAs (see Pub. 969)

• Diaper service

• Expenses for your general

health (even if following

your doctor’s advice)

such as——Health club

dues—Household help

(even if recommended by

a doctor)—Social activities,

such as dancing or

swimming lessons—Trip for

general health improvement

• Flexible spending account

reimbursements for medical

expenses (if contributions

were on a pre-tax basis)

• Funeral, burial, or cremation

expenses

• Health savings account

payments for medical

expenses

• Operation, treatment, or

medicine that is illegal under

federal or state law

• Life insurance or income

protection policies, or

policies providing payment

for loss of life, limb, sight,

etc.

• Maternity clothes

• Medical insurance included

in a car insurance policy

covering all persons injured

in or by your car

• Medicine you buy without a

prescription

• Nursing care for a healthy

baby

• Prescription drugs you

brought in (or ordered

shipped) from another

country, in most cases

• Nutritional supplements,

vitamins, herbal

supplements, “natural

medicines,” etc., unless

recommended by a medical

practitioner as a treatment

for a specic medical

condition diagnosed by a

physician

• Surgery for purely cosmetic

reasons

• Toothpaste, toiletries,

cosmetics, etc.

• Teeth whitening

• Weight-loss expenses not

for the treatment of the

treatment of obesity or other

disease

You can’t include in medical expenses amounts

you pay for controlled substances that aren’t legal under

federal law, even if such substances are legalized by state

law.

If MFS and spouse itemizes, taxpayer must

also itemize. Standard deduction can’t be

used. It doesn’t matter which spouse les

rst. Select “Use Standard or Itemized De-

duction” then select the option “Must itemize

because spouse itemized.”

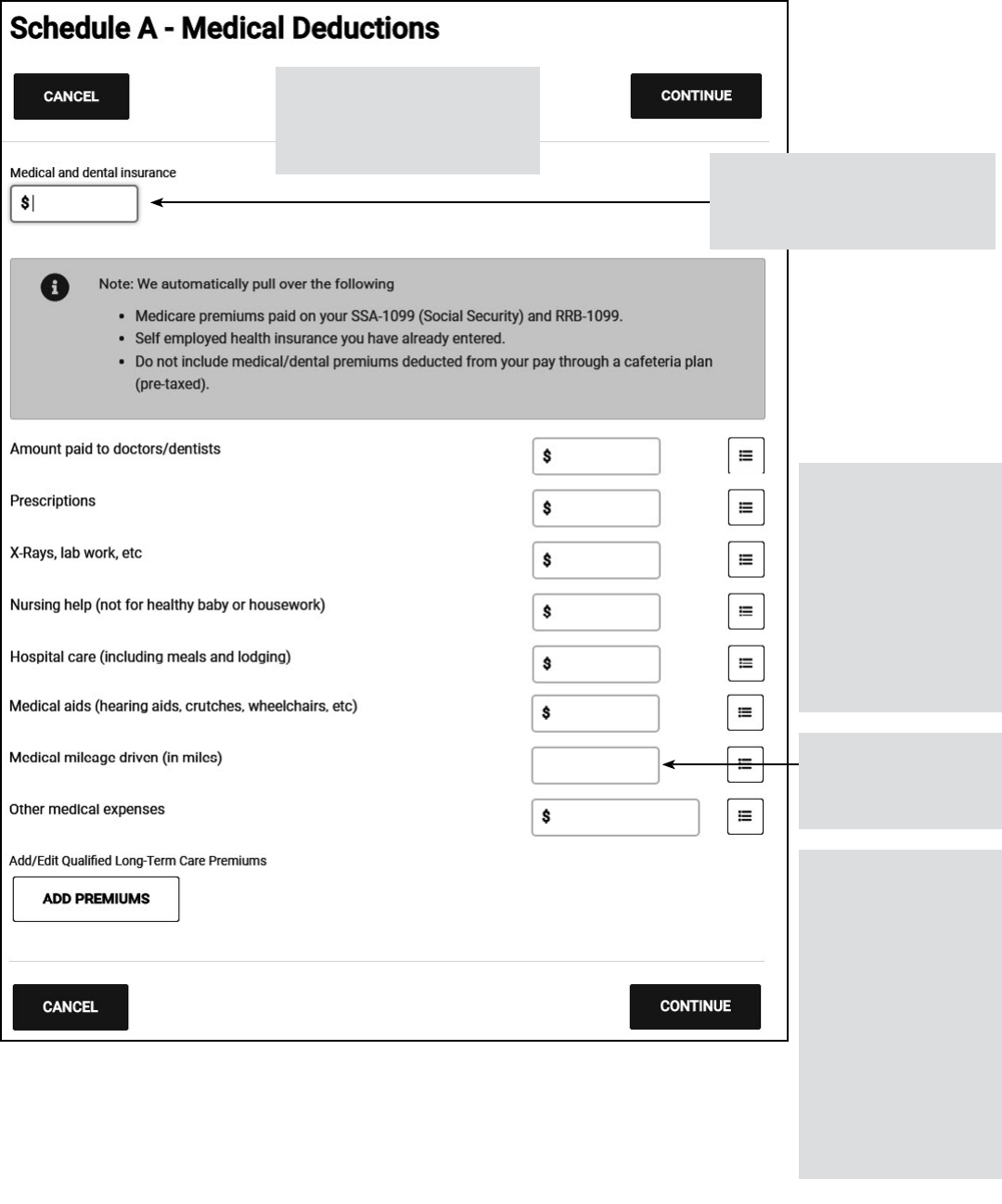

Select to enter medical expenses. Do

not include any medical insurance

included in the Self-Employed Health

Insurance Deduction.

Select to enter taxes not entered

elsewhere in the software.

Personal protective

equipment, such as masks,

hand sanitizer and

sanitizing wipes, for the primary

purpose of preventing the spread

of coronavirus are deductible

medical expenses.

F-6

Schedule A - Itemized Deductions (continued)

To enter multiple

expenses of a single

type, click on the small

calculator icon beside

the line. Enter the rst

description, the amount,

and Continue. Enter the

information for the next

item. They will be totaled

on the input line and

carried to Schedule A.

If taxpayer has medical insurance

through the Marketplace, remember

to adjust the total premium after the

PTC is calculated.

Taxpayers can deduct only the

amount of unreimbursed medical

and dental expenses that exceed

7.5% of their Adjusted Gross

Income (AGI).

Enter number of miles.

Standard mileage rate for

medical purposes is 16

cents per mile.

Qualied long-term care

premiums up to the

amounts shown below

can be included as medi-

cal expenses on Sched-

ule A, or in calculating

the self-employed health

insurance deduction.

• Age 40 or under: $450

• Age 41 to 50: $850

• Age 51 to 60: $1,690

• Age 61 to 70: $4,520

• Age 71 and over:

$5,640

The limit on premiums is

for each person.

Note: Medical and dental oor percentage is 7.5%. Some senior residences (nursing homes) have an

amount in the monthly cost which is a medical expense. Taxpayers can include in medical expenses

the cost of medical care in a nursing home, home for the aged or similar institution. This includes the

cost of meals and lodging if the principal reason for being there is to get medical care.

F-7

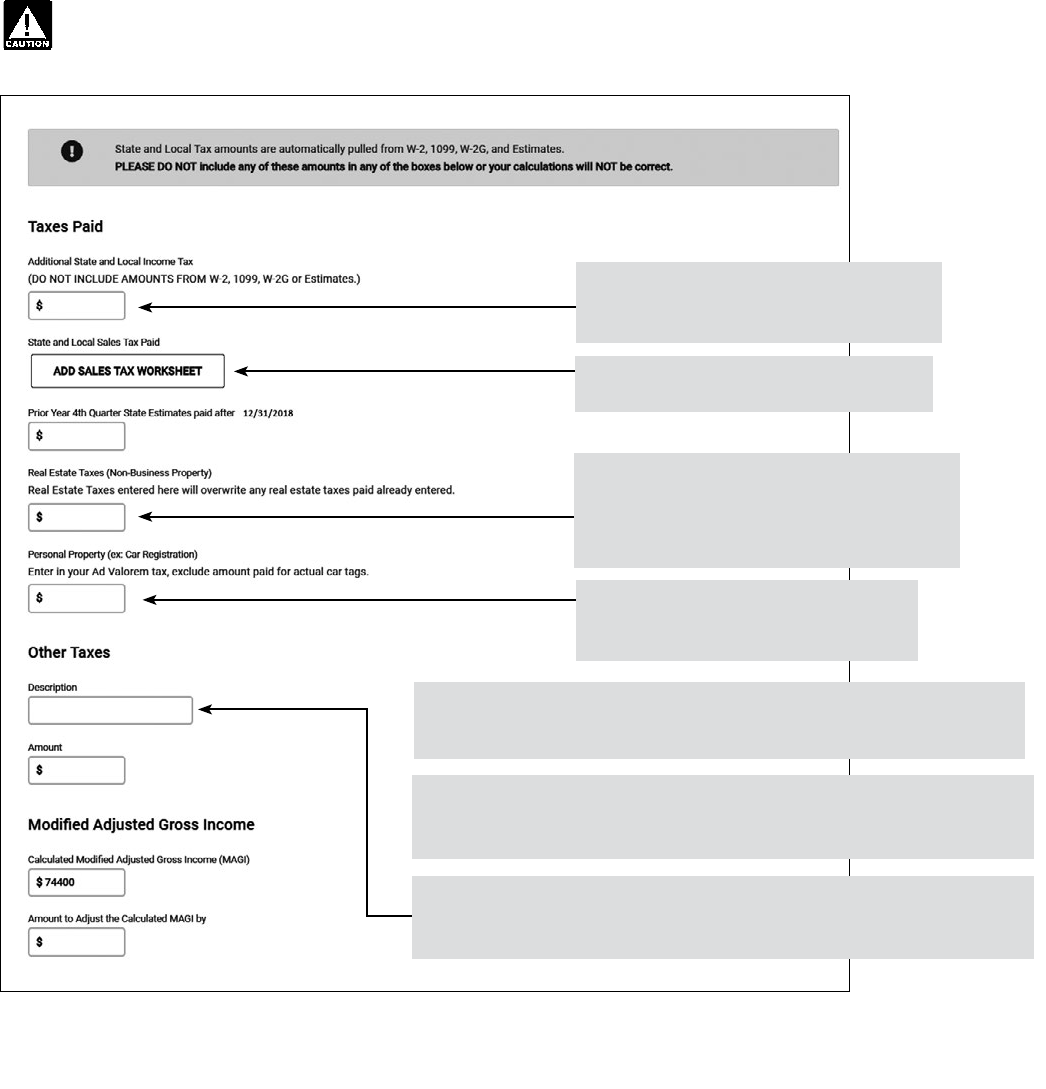

Schedule A - Taxes You Paid

The itemized deduction for state and local taxes and sales and property taxes is limited to a combined, total deduc-

tion of $10,000 ($5,000 if Married Filing Separately).

Enter amount paid with last year’s state

return and any other state and local income

tax payments not entered elsewhere.

Click here to open the sales tax worksheet.

See the next page for details.

If real estate taxes are only reported on Form

1098, enter them on the Mortgage Interest

Reported on the 1098 screen.

Otherwise, calculate the total real estate taxes

and enter in the Real Estate Taxes box.

Enter vehicle license registration fee

if based on value (ad valorem) under

Personal Property taxes.

If taxpayers purchased or sold a home in the tax year, they may not be

able to deduct all Real Estate Taxes. See Publication 17, “Real Estate

Taxes” section, for more information.

Taxes you cannot deduct: utilities, fees/licenses (drivers, marriage, dog);

assessments for improvements that increase property value; assessments

for services to the property (sewer, trash collection, etc.).

Note: The following items aren’t deductible on Schedule A: Federal income and excise taxes, Social Security or Medicare taxes,

federal unemployment (FUTA), railroad retirement taxes (RRTA), customs duties, federal gift taxes, per capita taxes, or foreign

real property taxes.

If taxpayers wish to deduct their foreign income taxes (instead of claiming

a credit) enter in Other Taxes and describe as “Foreign Income.”

F-8

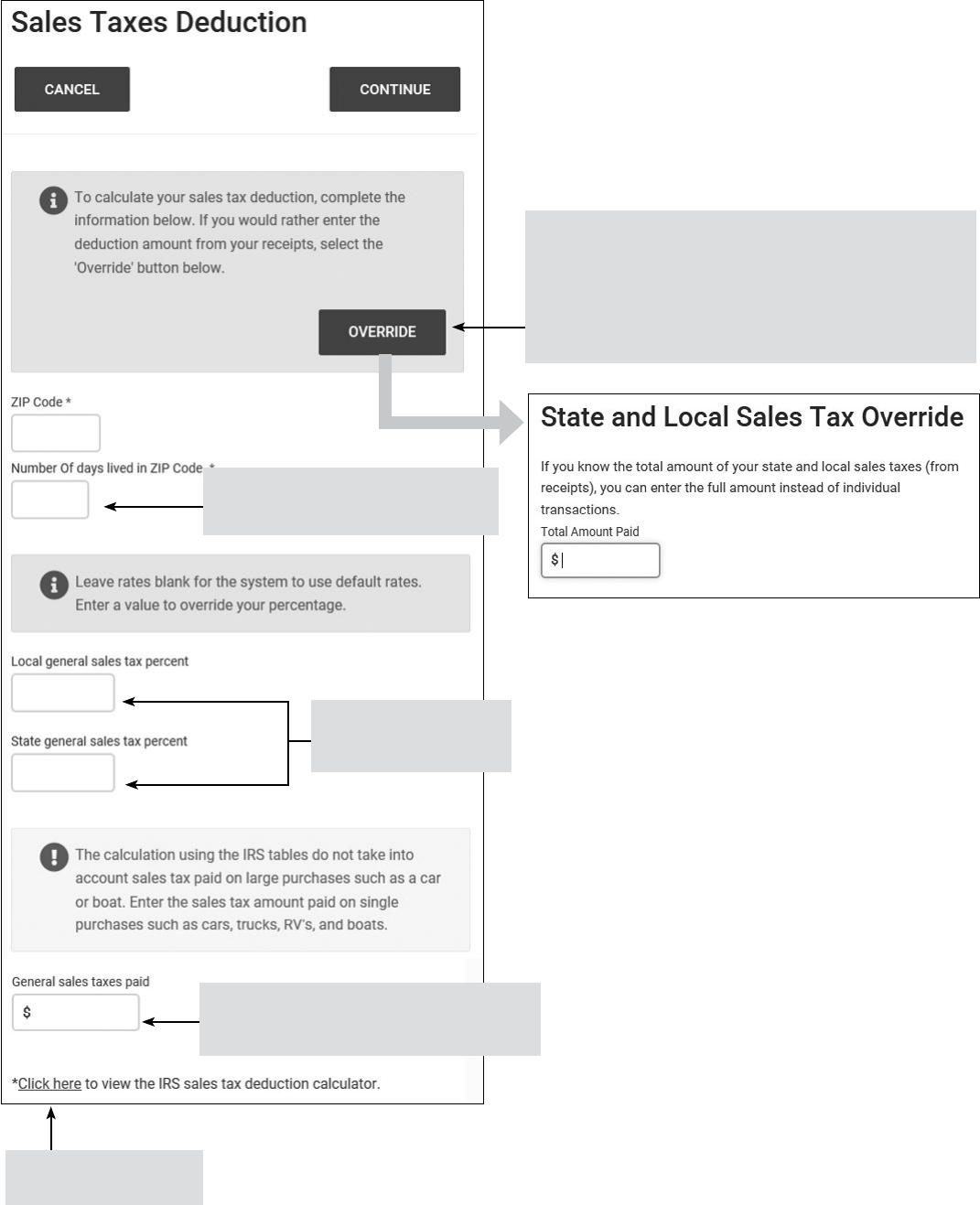

Schedule A - Sales Tax Deduction

If the taxpayer has a large amount of nontaxable income,

calculate their sales tax deduction using the IRS sales

tax deduction calculator. See the link to the IRS sales tax

deduction calculator at the bottom of the page. The calcu-

lator adds nontaxable income to AGI to give the taxpayer a

larger sales tax deduction. Use the override button to enter

the amount calculated.

If not using the override feature, enter

the ZIP code and number of days for

TaxSlayer to calculate the deduction.

Leave these blank if you

want the software to use

the default rates.

If not using the override feature, enter sales

tax here for large items (such as a car) if the

taxpayer purchased any during the year.

Link to the IRS sales tax

deduction calculator.

Note: If using the override feature, leave all other elds on the

Sales Tax Deduction screen blank.

F-9

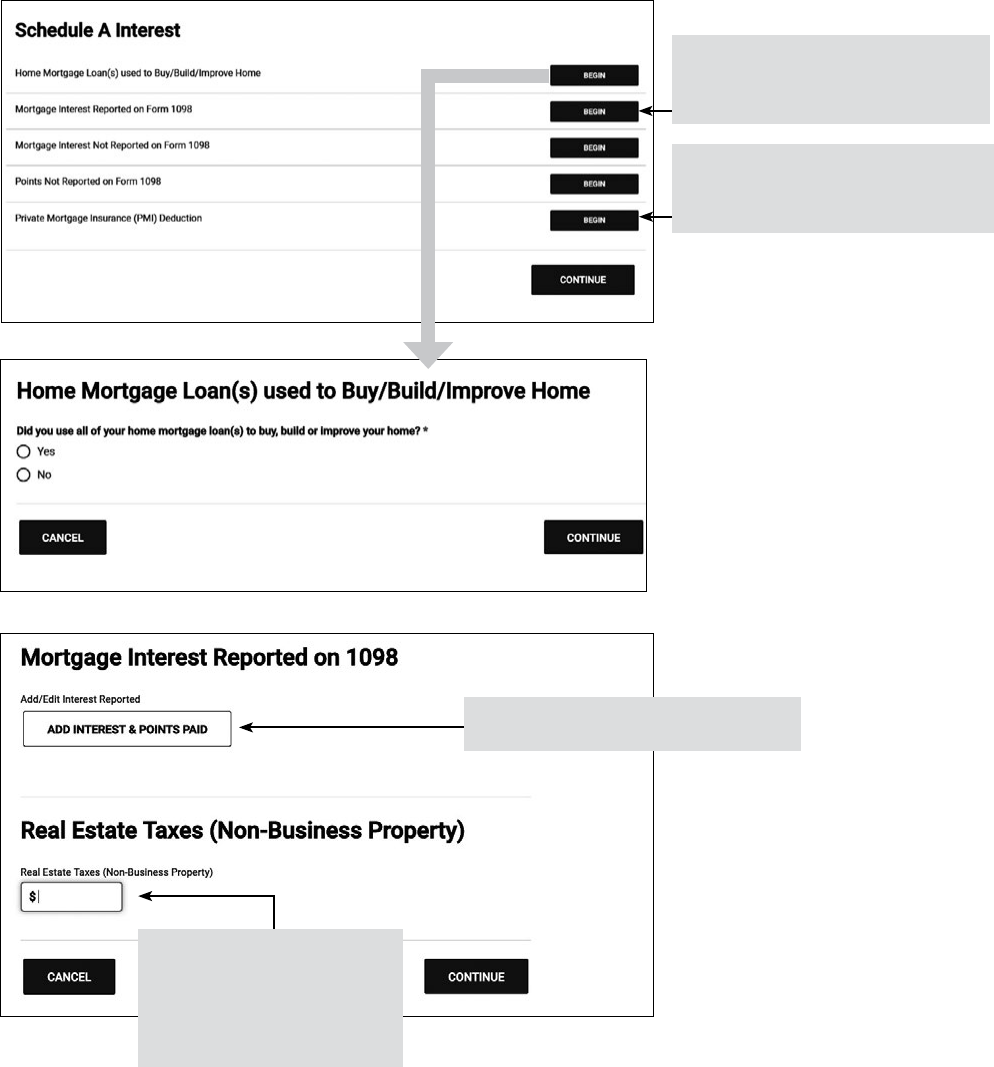

Schedule A - Itemized Deductions (continued)

Select for mortgage interest reported

on Form 1098. Enter amount from

Form 1098, Box 1 (and Box 2, if

applicable).

Note: The deduction for home equity debt is

disallowed as a mortgage interest deduction unless

the home equity debt was used to build, buy, or

substantially improve the taxpayer’s qualied

residence.

Note: A reverse mortgage is a loan where the

lender pays you (in a lump sum, a monthly

advance, a line of credit, or a combination of all

three) while you continue to live in your home. With

a reverse mortgage, you retain title to your home.

Depending on the plan, your reverse mortgage

becomes due with interest when you move, sell

your home, reach the end of a preselected loan

period, or die. Because reverse mortgages are

considered loan advances and not income, the

amount you receive isn’t taxable. Any interest

(including original issue discount) accrued on a

reverse mortgage is considered interest on home

equity debt and isn’t deductible.

For mortgage acquisition debt secured after

December 15, 2017, the amount of interest you

can deduct is on no more than $750,000 of debt

used to buy, build, or substantially improve your

principal home and a second home ($375,000

in the case of married taxpayers ling separate

tax returns) for tax years 2018 through 2025. If

the taxpayer secured a mortgage for acquisition

debt on or before December 15, 2017, the

new tax law doesn’t change the amount of

the deductible mortgage interest. Deductible

interest remains limited to mortgage interest on

up to $1 million ($500,000 MFS).

Points from renancing must be spread over

the life of the mortgage unless used to remodel

(see section in Publication 936, Home Mortgage

Interest Deduction, labeled “Points”). Enter loan

origination fee from closing statement as points

not reported on Form 1098 if not included as

points on Form 1098.

If there are multiple mortgages, make

additional Schedule A Interest entries.

Enter real estate taxes on the

1098 screen if all real estate

tax paid was reported on

the Form 1098. Otherwise,

enter on the Other Taxes Paid

screen.

Private mortgage insurance premiums

are deductible for 2021 and should

be entered on the Schedule A Interest

screen in TaxSlayer.

F-10

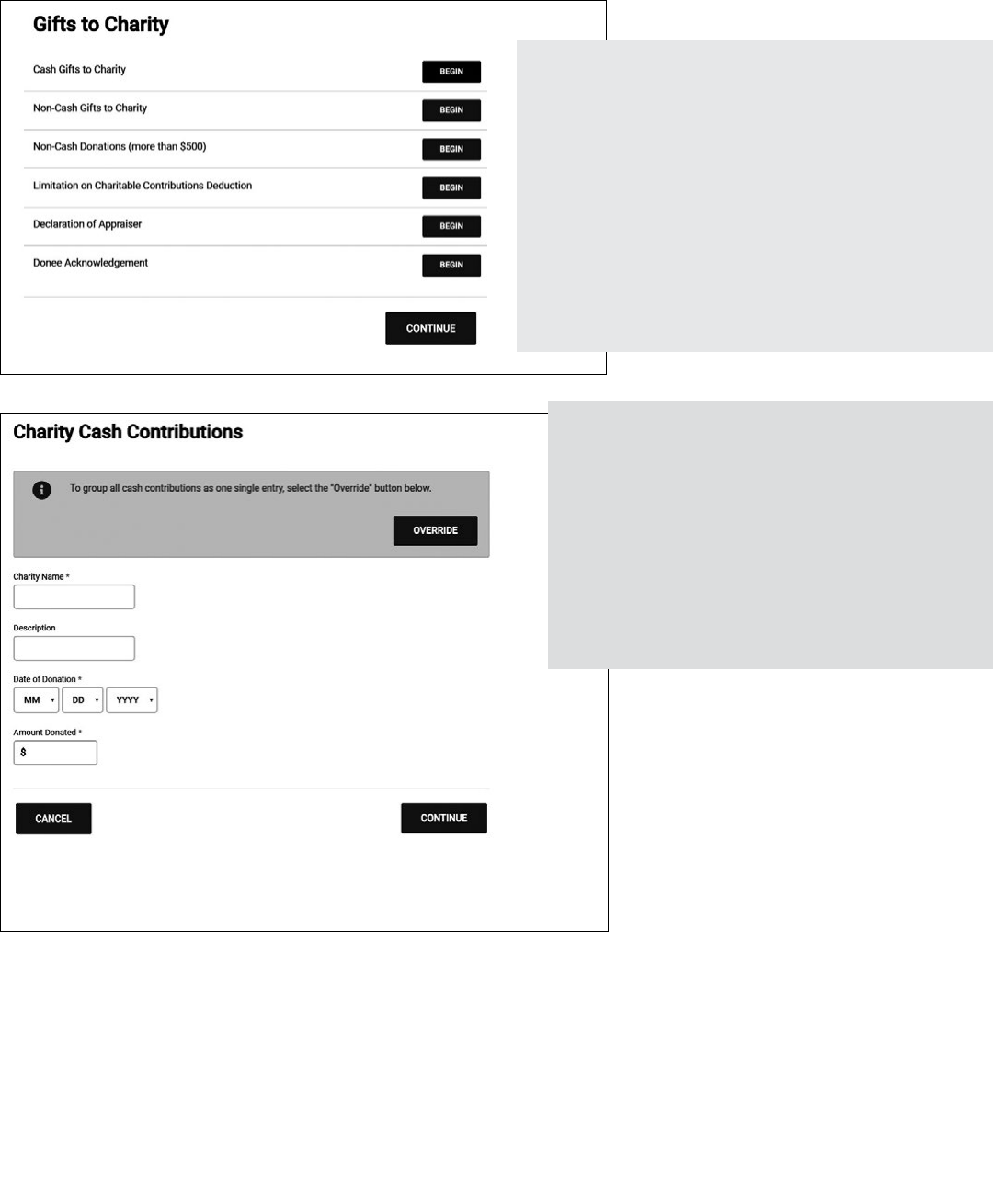

Schedule A - Itemized Deductions (continued)

These types of donations are not deductible: political; country club/fraternal lodge; chambers of commerce; raffle,

bingo, or lottery tickets; tuition; value of time/services; gifts to lobby groups; civic leagues, social clubs; labor unions,

homeowners association dues.

Note: The deduction for charitable contributions by taxpayers who do not itemize was modied by the Taxpayer Certainty and Disaster

Tax Relief Act of 2020. For tax year 2021, married couples ling a joint return may deduct up to $600 (all other lers are limited to

$300). Additionally, the deduction does not reduce adjusted gross income.

Note: Enter amounts given by cash or check under Cash Gifts

to Charity. For 2021 contributions up to 100% of AGI may be

deducted. See Publication 526 for denitions. Enter the value

of noncash items (including miles (14 cents per mile) driven in

service to a charity) donated under Noncash Gifts to Charity.

Be careful to list them separately.

If noncash contributions are greater than $500, Form 8283,

Noncash Charitable Contributions must be completed and this

form is Out of Scope (In Scope for Military certication).

Certain qualied contributions made for relief

eorts in disaster areas are not subject to the AGI limitation.

See Publication 976, Disaster Relief.

Note: Although you can’t deduct the value of your

services given to a qualied organization, you may be

able to deduct some volunteer expenses you pay in giving

services to a qualied organization. The amounts must be:

• Unreimbursed;

• Directly connected with the services;

• Expenses you had only because of the

services you gave; and

• Not personal, living, or family expenses.

F-11

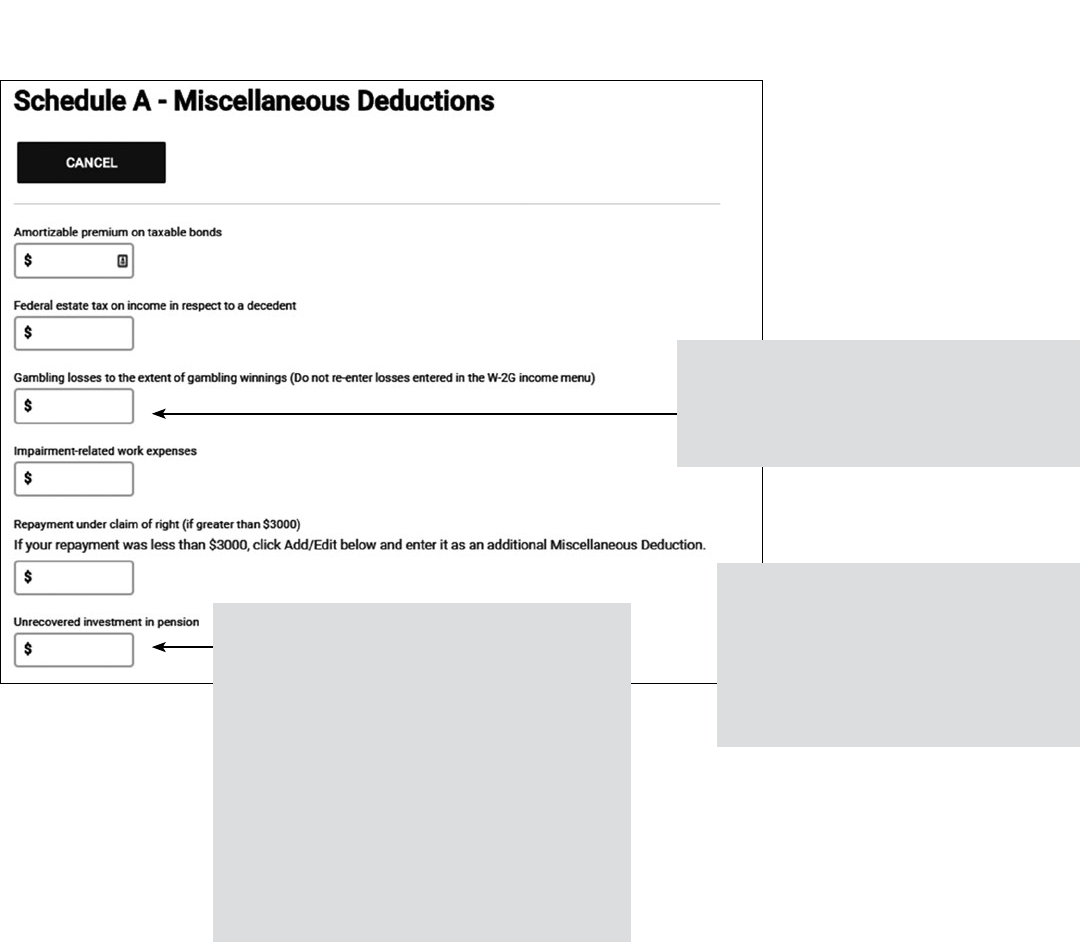

Schedule A - Miscellaneous Deductions

Gambling losses and expenses

incurred in gambling activities up to the

amount of winnings are deducted here. You

can’t deduct gambling losses that are more

than the taxpayer’s winnings.

Nondeductible expenses: commuting;

home repair; rent; loss from sale of

home; personal legal expenses;

lost/misplaced cash or property; nes/

penalties; safe deposit box rental; tax

return preparation; investment fees

and expenses.

Note: No miscellaneous itemized deductions will be allowed for job expenses and certain miscellaneous deductions subject to the

2% limitation. These expenses may be deductible on state returns.

A retired taxpayer who contributed to the cost

of an annuity can exclude from income a part

of each payment received as a tax-free return

of the investment. If the retired taxpayer dies

before the entire investment is recovered tax

free, any unrecovered investment can be de-

ducted on the retired taxpayer’s nal income

tax return in the unrecovered investment

pension box.

Note: Unrecovered Investment in pension = Total

Employee Contribution less amount recovered

using Simplied Method prior to death.