____________________

VIII. Privacy — GLBA

Gramm-Leach-Bliley Act

(Privacy of Consumer Financial Information)

Introduction

Title V, Subtitle A of the Gramm-Leach-Bliley Act

(“GLBA”)

1

governs the treatment of nonpublic personal

information about consumers by financial institutions. Section

502 of the Subtitle, subject to certain exceptions, prohibits a

financial institution from disclosing nonpublic personal

information about a consumer to nonaffiliated third parties,

unless (i) the institution satisfies various notice and opt-out

requirements, and (ii) the consumer has not elected to opt out

of the disclosure. Section 503 requires the institution to

provide notice of its privacy policies and practices to its

customers. Section 504 authorizes the issuance of regulations

to implement these provisions.

In 2000, the Board of Governors of the Federal Reserve

System (“Board”), the Federal Deposit Insurance Corporation

(“FDIC”), the National Credit Union Administration

(“NCUA”), the Office of the Comptroller of the Currency

(“OCC”), and the former Office of Thrift Supervision

(“OTS”), published regulations implementing provisions of

GLBA governing the treatment of nonpublic personal

information about consumers by financial institutions.

2

Title X of the Dodd-Frank Act Wall Street Reform and

Consumer Protection Act (“Dodd-Frank Act”)

3

granted

rulemaking authority for most provisions of Subtitle A of

Title V of GLBA to the Consumer Financial Protection

Bureau (“CFPB”) with respect to financial institutions and

other entities subject to the CFPB’s jurisdiction, except

securities and futures-related companies and certain motor

vehicle dealers. The Dodd-Frank Act also granted authority

to the CFPB to examine and enforce compliance with these

statutory provisions and their implementing regulations with

respect to entities under CFPB jurisdiction.

4

In December

2011 the CFPB recodified in Regulation P, 12 CFR Part

1016, the implementing regulations that were previously

issued by the Board, the FDIC, the Federal Trade

Commission (“FTC”), the NCUA, the OCC, and the former

OTS.

5

1

15 U.S.C. Sections6801-6809.

2

The NCUA published its final rule in the Federal Register on May 18, 2000

(65 FR 31722). The Board, the FDIC, the OCC, and the former OTS

jointly published their final rules on June 1, 2000 (65 FR 35162).

3

Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, Pub.

L. No. 111-203, Title X, 124 Stat. 1983 (2010).

4

Dodd-Frank Act Sections 1002(12)(J), 1024(b)-(c), and 1025(b)-(c); 12

U.S.C. Sections5481(12)(J), 5514(b)-(c), and 5515(b)-(c). Section

1002(12)(J) of the Dodd-Frank Act, however, excluded financial

institutions’ information security safeguards under GLBA section 501(b)

from the CFPB’s rulemaking, examination, and enforcement authority.

The regulation establishes rules governing duties of a financial

institution to provide particular notices and limitations on its

disclosure of nonpublic personal information, as summarized

below.

• A financial institution must provide notice of its privacy

policies and practices, and allow the consumer to opt out

of the disclosure of the consumer’s nonpublic personal in-

formation to a nonaffiliated third party if the disclosure is

outside of the exceptions in sections 13, 14, or 15 of the

regulation. If the financial institution provides the con-

sumer’s nonpublic personal information to a nonaffiliated

third party under the exception in section 13, it must pro-

vide notice of its privacy policies and practices to the con-

sumer. Under the exception in section 13, the financial

institution must also enter into a contractual agreement

with the third party that prohibits the third party from dis-

closing or using the information other than to perform ser-

vices for the institution or functions on the institution’s

behalf, including use under an exception in sections 14 or

15 in the ordinary course of business to carry out those

services or functions. If the financial institution complies

with these requirements, it is not required to provide an

opt out notice.

• Regardless of whether a financial institution shares non-

public personal information, the institution must provide

notice of its privacy policies and practices to its custom-

ers.

• A financial institution generally may not disclose con-

sumer account numbers to any nonaffiliated third party

for marketing purposes.

• A financial institution must follow redisclosure and reuse

limitations on any nonpublic personal information it re-

ceives from a nonaffiliated financial institution.

In general, the privacy notice must describe a financial

institution’s policies and practices with respect to collecting

and disclosing nonpublic personal information about a

consumer to both affiliated and nonaffiliated third parties.

Also, the notice must provide a consumer a reasonable

opportunity to direct the institution generally not to share

nonpublic personal information about the consumer (that is, to

“opt out”) with nonaffiliated third parties other than as

permitted by exceptions under the regulation (for example,

sharing for everyday business purposes, such as processing

transactions and maintaining customers’ accounts, and in

response to properly executed governmental requests). The

5

76 FR 79025 (Dec. 21, 2011). Pursuant to GLBA, the FTC retains

rulemaking authority over any financial institution that is a person described in

12 U.S.C. Section5519 (with certain statutory exceptions, the FTC generally

retains rulemaking authority for motor vehicle dealers predominantly engaged

in the sale and servicing of motor vehicles, the leasing and servicing of motor

vehicles, or both).

FDIC Consumer Compliance Examination Manual — April 2021 VIII–1.1

____________________

VIII. Privacy — GLBA

privacy notice must also provide, where applicable under the

Fair Credit Reporting Act (“FCRA”), a notice and an

opportunity for a consumer to opt out of certain information

sharing among affiliates.

Section 728 of the Financial Services Regulatory Relief Act of

2006 required the four federal banking agencies (the Board,

the FDIC, the OCC, and the former OTS) and four additional

federal regulatory agencies (the Commodity Futures Trading

Commission (“CFTC”), the FTC, the NCUA, and the

Securities and Exchange Commission (“SEC”)) to develop a

model privacy form that financial institutions may rely on as a

safe harbor to provide disclosures under the privacy rules.

On December 1, 2009, the eight federal agencies jointly

released a voluntary model privacy form designed to make it

easier for consumers to understand how financial institutions

collect and share nonpublic personal information.

6

The final

rule adopting the model privacy form was effective on

December 31, 2009.

On October 28, 2014, the CFPB published a final rule

amending the requirements regarding financial institutions’

provision of their annual disclosures of privacy policies and

practices to customers by creating an alternative delivery

method that financial institutions can use under certain

circumstances.

7

The amendment was effective immediately

upon publication. The alternative delivery method allows a

financial institution to provide an annual privacy notice by

posting the annual notice on its web site, if the financial

institution meets certain conditions.

As of December 4, 2015, section 75001 of the Fixing

America’s Surface Transportation Act

8

(“FAST Act”)

amended section 503 of GLBA to establish an exception to the

annual privacy notice requirements whereby a financial

institution that meets certain criteria is not required to provide

an annual privacy notice to customers. The amendment was

effective upon enactment.

There are fewer requirements to qualify for the exception to

providing an annual privacy notice pursuant to the FAST Act

GLBA amendments than there are to qualify to use the

CFPB’s alternative delivery method; any institution that meets

the requirements for using the alternative delivery method is

effectively excepted from delivering an annual privacy notice.

6

74 FR 62890.

7

79 FR 64057.

8

Fixing America’s Surface Transportation Act of 2015, Pub. L. No. 114-94

(2015), 129 Stat. 1312 (2015).

Definitions and Key Concepts

In discussing the duties and limitations imposed by the

regulation, a number of key concepts are used. These concepts

include “financial institution”; “nonpublic personal

information”; “nonaffiliated third party”; the “opt out” right

and the exceptions to that right; and “consumer” and

“customer.” Each concept is briefly discussed below. A more

complete explanation of each appears in the regulation.

Financial Institution: A “financial institution” is any

institution the business of which is engaging in activities that

are financial in nature or incidental to such financial activities,

as determined by section 4(k) of the Bank Holding Company

Act of 1956. Financial institutions can include banks,

securities brokers and dealers, insurance underwriters and

agents, finance companies, mortgage bankers, and travel

agents.

9

Nonpublic personal information: “Nonpublic personal

information” generally is any information that is not publicly

available and that:

• a consumer provides to a financial institution to obtain a

financial product or service from the institution;

• results from a transaction between the consumer and the

institution involving a financial product or service; or

• a financial institution otherwise obtains about a consumer

in connection with providing a financial product or

service.

Information is publicly available if an institution has a

reasonable basis to believe that the information is lawfully

made available to the general public from government records,

widely distributed media, or legally required disclosures to the

general public. Examples include information in a telephone

book or a publicly recorded document, such as a mortgage or

security interest filing.

Nonpublic personal information may include individual items

of information as well as lists of information. For example,

nonpublic personal information may include names, addresses,

phone numbers, social security numbers, income, credit score,

and information obtained through Internet collection devices

(i.e., cookies).

There are special rules regarding lists. Publicly available

information would be treated as nonpublic if it were included

9 Certain functionally regulated subsidiaries, such as brokers, dealers, and

investment advisers, are subject to GLBA implementing regulations issued

by the SEC. Other functionally regulated subsidiaries, such as futures

commission merchants, commodity trading advisors, commodity pool

operators, and introducing brokers in commodities, are subject to GLBA

implementing regulations issued by the CFTC. Insurance entities may be

subject to privacy regulations issued by their respective state insurance

authorities.

VIII–1.2 FDIC Consumer Compliance Examination Manual — April 2021

VIII. Privacy — GLBA

on a list of consumers derived from nonpublic personal

information. For example, a list of the names and addresses of

a financial institution’s depositors would be nonpublic

personal information even though the same names and

addresses might be published in local telephone directories,

because the list is derived from the fact that a person has a

deposit account with an institution, which is not publicly

available information.

However, if the financial institution has a reasonable basis to

believe that certain customer relationships are a matter of

public record, then any list of these relationships would be

considered publicly available information. For instance, a list

of mortgage customers from public mortgage records would

be considered publicly available information. The institution

could provide a list of such customers, and include on that list

any other publicly available information it has about those

customers without having to provide notice or opt out.

Nonaffiliated third party: A “nonaffiliated third party” is any

person except a financial institution’s affiliate or a person

employed jointly by a financial institution and a company that

is not the institution’s affiliate. An “affiliate” of a financial

institution is any company that controls, is controlled by, or is

under common control with the financial institution.

Opt Out Right and Exceptions:

The Right—Consumers must be given the right to “opt out”

of, or prevent, a financial institution from disclosing nonpublic

personal information about them to a nonaffiliated third party

unless an exception to that right applies. The exceptions are

detailed in sections 13, 14, and 15 of the regulation and

described below.

As part of the opt out right, consumers must be given a

reasonable opportunity and a reasonable means to opt out.

What constitutes a reasonable opportunity to opt out depends

on the circumstances surrounding the consumer’s transaction,

but a consumer must be provided a reasonable amount of time

to exercise the opt out right. For example, it would be

reasonable if the financial institution allows 30 days from the

date of mailing a notice or 30 days after customer

acknowledgement of an electronic notice for an opt out

direction to be returned. What constitutes a reasonable means

to opt out may include check-off boxes, a reply form, or a toll-

free telephone number. It is not reasonable to require a

consumer to write his or her own letter as the only means to

opt out.

The Exceptions

Exceptions to the opt out right are detailed in sections 13, 14,

and 15 of the regulation. Financial institutions need not

comply with opt-out requirements if they limit disclosure of

nonpublic personal information:

• Section 13: To a nonaffiliated third party to perform

services for the financial institution or to function on its

behalf, including marketing the institution’s own products

or services or those offered jointly by the institution and

another financial institution. The exception is permitted

only if the financial institution provides an initial notice of

these arrangements and by contract prohibits the third

party from disclosing or using the information for other

than the specified purposes. However, if the service or

function is covered by the exceptions in section 14 or 15

(discussed below), the financial institution does not have

to comply with the disclosure and confidentiality

requirements of section 13.

• Section 14: As necessary to effect, administer, or enforce a

transaction that a consumer requests or authorizes, or

under certain other circumstances relating to existing

relationships with customers. Disclosures under this

exception could be in connection with the audit of credit

information, administration of a rewards program, or

provision of an account statement.

• Section 15: For specified other disclosures that a financial

institution normally makes, such as to protect against or

prevent actual or potential fraud; to the financial

institution’s attorneys, accountants, and auditors; or to

comply with applicable legal requirements, such as the

disclosure of information to regulators.

Consumer and Customer:

The distinction between consumers and customers is

significant because financial institutions have additional

disclosure duties with respect to customers. Under the

regulation, all customers are consumers, but not all consumers

are customers.

A “consumer” is an individual, or that individual’s legal

representative, who obtains or has obtained a financial product

or service from a financial institution that is to be used

primarily for personal, family, or household purposes.

A “financial service” includes, among other things, a

financial institution’s evaluation or brokerage of information

that the institution collects in connection with a request or an

application from a consumer for a financial product or service.

For example, a financial service includes a lender’s evaluation

of an application for a consumer loan or for opening a deposit

account even if the application is ultimately rejected or

withdrawn.

Consumers who are not customers are entitled to an initial

privacy and opt out notice before the financial institution

shares nonpublic personal information with nonaffiliated third

parties outside of the exceptions in sections 13, 14, and 15.

Consumers who are not customers are entitled to an initial

privacy notice before the financial institution shares nonpublic

personal information with a nonaffiliated third party under the

FDIC Consumer Compliance Examination Manual — April 2021

VIII–1.3

VIII. Privacy — GLBA

exception in section 13. Under the exception in section 13, the

financial institution must also enter into a contractual

agreement with the third party that prohibits the third party

from disclosing or using the information other than to perform

services for the institution or functions on the institution’s

behalf, including use under an exception in sections 14 or 15

in the ordinary course of business to carry out those services or

functions. If a financial institution complies with these

requirements, it is not required to provide an opt out notice.

A “customer” is a consumer who has a “customer

relationship” with a financial institution. A “customer

relationship” is a continuing relationship between a consumer

and a financial institution under which the institution provides

one or more financial products or services to the consumer that

are to be used primarily for personal, family, or household

purposes.

• For example, a customer relationship may be established

when a consumer engages in one of the following

activities with a financial institution:

° maintains a deposit or investment account;

° obtains a loan;

° enters into a lease of personal property; or

° obtains financial, investment, or economic advisory

services for a fee.

Customers are entitled to initial and annual privacy notices

regardless of the information disclosure practices of their

financial institution unless an exception to the annual privacy

notice requirement applies.

There is a special rule for loans. When a financial institution

sells the servicing rights to a loan to another financial

institution, the customer relationship transfers with the

servicing rights. However, any information on the borrower

retained by the institution that sells the servicing rights must

be accorded the protections due any consumer.

• Note that isolated transactions alone will not cause a

consumer to be treated as a customer. For example, if an

individual purchases a bank check from a financial

institution where the person has no account, the individual

will be a consumer but not a customer of that institution

because he or she has not established a customer

relationship. Likewise, if an individual uses the ATM of a

financial institution where the individual has no account,

even repeatedly, the individual will be a consumer, but not

a customer of that institution.

Financial Institution Duties

The regulation establishes specific duties and limitations for a

financial institution based on its activities. Financial

institutions that intend to disclose nonpublic personal

information outside the exceptions in sections 13, 14, and 15

will have to provide opt out rights to their customers and to

consumers who are not customers. All financial institutions

have an obligation to provide initial and annual notices of their

privacy policies and practices to their customers (unless an

exception to the annual privacy notice requirement applies)

and to provide an initial notice to consumers who are not

customers before disclosing nonpublic personal information to

a nonaffiliated third party other than under sections 14 and 15.

All financial institutions must abide by the regulatory limits on

the disclosure of account numbers to nonaffiliated third parties

and on the redisclosure and reuse of nonpublic personal

information received from nonaffiliated financial institutions.

A brief summary of financial institution duties and limitations

appears below. A more complete explanation of each appears

in the regulation.

Notice and Opt Out Duties to Consumers:

Before a financial institution discloses nonpublic personal

information about any of its consumers to a nonaffiliated third

party, and an exception in section 14 or 15 does not apply,

then the financial institution must provide to the consumer:

• an initial notice of its privacy policies and practices;

• an opt out notice (including, among other things, a

reasonable means to opt out); and

• a reasonable opportunity, before the financial institution

discloses the information to the nonaffiliated third party,

to opt out.

Before a financial institution discloses nonpublic personal

information about a consumer to a nonaffiliated third party

under the exception in section 13, the financial institution must

provide to the consumer an initial notice of its privacy policies

and practices. Under the exception in section 13, the financial

institution must also enter into a contractual agreement with

the third party that prohibits the third party from disclosing or

using the information other than to perform services for the

institution or functions on the institution’s behalf, including

use under an exception in sections 14 or 15 in the ordinary

course of business to carry out those services or functions. If a

financial institution complies with these requirements, it is not

required to provide an opt out notice.

The financial institution may not disclose any nonpublic

personal information to nonaffiliated third parties except under

the enumerated exceptions unless these notices have been

provided and the consumer has not opted out (where

applicable). Additionally, the institution must provide a

revised notice before the financial institution begins to share a

new category of nonpublic personal information or shares

information with a new category of nonaffiliated third party in

a manner that was not described in the previous notice.

VIII–1.4 FDIC Consumer Compliance Examination Manual — April 2021

VIII. Privacy — GLBA

Note that a financial institution need not comply with the

initial and opt-out notice requirements for consumers who are

not customers if the institution limits disclosure of nonpublic

personal information to the exceptions in sections 14 and 15.

A financial institution that discloses nonpublic personal

information about a consumer to a nonaffiliated third party

under the exception in section 13 must provide an initial

notice. Under the exception in section 13, the financial

institution must also enter into a contractual agreement with

the third party that prohibits the third party from disclosing or

using the information other than to perform services for the

institution or functions on the institution’s behalf, including

use under an exception in sections 14 or 15 in the ordinary

course of business to carry out those services or functions. If

these requirements are met, the financial institution is not

required to provide an opt out notice.

Notice Duties to Customers:

In addition to the duties described above, there are several

duties unique to customers. In particular, regardless of whether

the institution discloses or intends to disclose nonpublic

personal information, a financial institution must provide

notice to its customers of its privacy policies and practices at

various times.

• A financial institution must provide an initial notice of its

privacy policies and practices to each customer, not later

than the time a customer relationship is established.

Section 4(e) of the regulation describes the exceptional

cases in which delivery of the notice is allowed

subsequent to the establishment of the customer

relationship.

• A financial institution must provide an annual notice at

least once in any period of 12 consecutive months during

the continuation of the customer relationship unless an

exception to the annual privacy notice requirement

applies.

• Generally, new privacy notices are not required for each

new product or service. However, a financial institution

must provide a new notice to an existing customer when

the customer obtains a new financial product or service

from the institution, if the initial or annual notice most

recently provided to the customer was not accurate with

respect to the new financial product or service.

• When a financial institution does not disclose nonpublic

personal information (other than as permitted under

section 14 and section 15 exceptions) and does not reserve

the right to do so, the institution has the option of

providing a simplified notice.

Requirements for Notices

Clear and Conspicuous. Privacy notices must be clear and

conspicuous, meaning they must be reasonably understandable

and designed to call attention to the nature and significance of

the information contained in the notice. The regulation does

not prescribe specific methods for making a notice clear and

conspicuous, but does provide examples of ways in which to

achieve the standard, such as the use of short explanatory

sentences or bullet lists, and the use of plain-language

headings and easily readable typeface and type size. Privacy

notices also must accurately reflect the institution’s privacy

practices.

Delivery Rules. Privacy notices must be provided so that each

recipient can reasonably be expected to receive actual notice in

writing, or if the consumer agrees, electronically. To meet this

standard, a financial institution could, for example, (1) hand-

deliver a printed copy of the notice to its consumers, (2) mail a

printed copy of the notice to a consumer’s last known address,

or (3) for the consumer who conducts transactions

electronically, post the notice on the institution’s web site and

require the consumer to acknowledge receipt of the notice as a

necessary step to completing the transaction.

For customers only, a financial institution must provide the

initial notice (as well as any annual notice and any revised

notice) so that a customer can retain or subsequently access

the notice. A written notice satisfies this requirement. For

customers who obtain financial products or services

electronically, and agree to receive their notices on the

institution’s web site, the institution may provide the current

version of its privacy notice on its web site.

As of October 28, 2014, a financial institution may use an

alternative delivery method for providing annual privacy

notices to customers through posting the annual notices on

their web sites if: (1) no opt out rights are triggered by the

financial institution’s information sharing practices under

GLBA or under FCRA section 603, and opt out notices

required by FCRA section 624 and Subpart C of Regulation V

have previously been provided, if applicable, or the annual

privacy notice is not the only notice provided to satisfy those

requirements; (2) certain information included in the annual

privacy notice has not changed since the previous notice; and

(3) the financial institution uses the model form provided in

the regulation as its annual privacy notice. In order to use this

alternative delivery method, an institution must: (1) insert a

clear and conspicuous statement at least once per year on an

account statement, coupon book, or a notice or disclosure the

institution issues under any provision of law that informs

customers that the annual privacy notice is available on the

institution’s web site, that the institution will mail the notice to

customers who request it by calling a specific telephone

number, and that the notice has not changed; (2) continuously

post the current privacy notice in a clear and conspicuous

manner on a page on its web site, on which the only content is

the privacy notice, without requiring the customer to provide

any information such as a login name or password or agree to

FDIC Consumer Compliance Examination Manual — April 2021

VIII–1.5

VIII. Privacy — GLBA

any conditions to access the web site; and (3) mail its current

privacy notice to those customers who request it by telephone

within ten calendar days of the request.

As of December 4, 2015, pursuant to the FAST Act’s GLBA

amendment, a financial institution is not required to provide an

annual privacy notice to its customers if it: (1) solely shares

nonpublic personal information in accordance with the

provisions of GLBA sections 502(b)(2) (corresponding to

Regulation P section 1016.13) or 502(e) (corresponding to

Regulation P sections 1016.14 and .15) or regulations

prescribed under GLBA section 504(b); and (2) has not

changed its policies and practices with regard to disclosing

nonpublic personal information since its most recent

disclosure to its customers that was made in accordance with

GLBA section 503. An institution that at any time fails to

comply with either of the criteria is not eligible for the

exception and is required to provide an annual privacy notice

to its customers.

Notice Content. A privacy notice must contain specific

disclosures. However, a financial institution may provide to

consumers who are not also customers a “short form” initial

notice together with an opt out notice stating that the

institution’s privacy notice is available upon request and

explaining a reasonable means for the consumer to obtain it.

The following is a list of disclosures regarding nonpublic

personal information that institutions must provide in their

privacy notices, as applicable:

1. categories of information collected;

2. categories of information disclosed;

3. categories of affiliates and nonaffiliated third parties to

whom the institution may disclose information;

4. policies and practices with respect to the treatment of

former customers’ information;

5. categories of information disclosed to nonaffiliated third

parties that perform services for the institution or

functions on the institution’s behalf and categories of third

parties with whom the institution has contracted (Section

13);

6. an explanation of the opt out right and methods for opting

out;

7. any opt out notices that the institution must provide under

the FCRA with respect to affiliate information sharing;

8. policies and practices for protecting the security and

confidentiality of information; and

9. a statement that the institution makes disclosures to other

nonaffiliated third parties for everyday business purposes

or as permitted by law (Sections 14 and 15).

Model Privacy Form. The Appendix to the regulation

contains the model privacy form. A financial institution can

use the model form to obtain a “safe harbor” for compliance

with the content requirements for notifying consumers of its

information-sharing practices and their right to opt out of

certain sharing practices. To obtain the safe harbor, the

institution must provide a model form in accordance with the

instructions set forth in the Appendix of the regulation.

Additionally, institutions using the alternative delivery method

for providing annual privacy notices to customers must use the

model form.

Limitations on Disclosure of Account Numbers (section 12):

A financial institution must not disclose an account number or

similar form of access number or access code for a credit card,

deposit, or transaction account to any nonaffiliated third party

(other than a consumer reporting agency) for use in

telemarketing, direct mail marketing, or other marketing

through electronic mail to the consumer.

The disclosure of encrypted account numbers without an

accompanying means of decryption, however, is not subject to

this prohibition. The regulation also expressly allows

disclosures by a financial institution to its agent to market the

institution’s own products or services (although the financial

institution must not authorize the agent to directly initiate

charges to the customer’s account). The regulation also does

not bar a financial institution from disclosing account numbers

to participants in private-label or affinity card programs, if the

participants are identified to the customer when the customer

enters the program.

Redisclosure and Reuse Limitations on Nonpublic Personal

Information Received (section 11):

If a financial institution receives nonpublic personal

information from a nonaffiliated financial institution, its

disclosure and use of the information is limited.

• For nonpublic personal information received under a

section 14 or 15 exception, the financial institution is

limited to:

° Disclosing the information to the affiliates of the

financial institution from which it received the

information;

° Disclosing the information to its own affiliates, who

may, in turn, disclose and use the information only to

the extent that the financial institution can do so; and

° Disclosing and using the information pursuant to a

section 14 or 15 exception (for example, an institution

receiving information for account processing could

disclose the information to its auditors).

• For nonpublic personal information received other than

under a section 14 or 15 exception, the recipient’s use of

the information is unlimited, but its disclosure of the

information is limited to:

VIII–1.6 FDIC Consumer Compliance Examination Manual — April 2021

____________________

VIII. Privacy — GLBA

° Disclosing the information to the affiliates of the

financial institution from which it received the

information;

° Disclosing the information to its own affiliates, who

may, in turn disclose the information only to the

extent that the financial institution can do so; and

° Disclosing the information to any other person, if the

disclosure would be lawful if made directly to that

person by the financial institution from which it

received the information. For example, an institution

that received a customer list from another financial

institution could disclose the list in accordance with

the privacy policy of the financial institution that

provided the list, subject to any opt out election or

revocation by the consumers on the list, and in

accordance with appropriate exceptions under sections

14 and 15.

Other Matters

Fair Credit Reporting Act

The regulation does not modify, limit, or supersede the

operation of the FCRA.

State Law

The regulation does not supersede, alter, or affect any state

statute, regulation, order, or interpretation, except to the extent

that it is inconsistent with the regulation. A state statute,

regulation, order, or interpretation is consistent with the

regulation if the protection it affords any consumer is greater

than the protection provided under the regulation, as

determined by the CFPB, on its own motion or upon the

petition of any interested party, after consultation with the

agency or authority with jurisdiction under section 505(a) of

GLBA over either the person who initiated the complaint or

that is the subject of the complaint.

Guidelines Regarding Protecting Customer Information

The regulation requires a financial institution to disclose its

policies and practices for protecting the confidentiality,

security, and integrity of nonpublic personal information about

consumers (whether or not they are customers). The disclosure

need not describe these policies and practices in detail, but

instead may describe in general terms who is authorized to

have access to the information and whether the institution has

security practices and procedures in place to ensure the

confidentiality of the information in accordance with the

institution’s policies.

The four federal banking agencies published guidelines,

pursuant to section 501(b) of GLBA, that address steps a

10

These reflect the interagency examination procedures in their entirety.

financial institution should take in order to protect customer

information. The guidelines relate only to information about

customers, rather than all consumers. Compliance examiners

should consider the findings of a 501(b) inspection during the

compliance examination of a financial institution for purposes

of evaluating the accuracy of the institution’s disclosure

regarding information security.

Examination Objectives

1. To assess the quality of a financial institution’s

compliance management policies, procedures, and internal

controls for implementing the regulation, specifically

ensuring consistency between what the financial

institution tells consumers in its notices about its policies

and practices and what it actually does.

2. To determine the reliance that can be placed on a financial

institution’s policies, procedures, and internal controls for

monitoring the institution’s compliance with the

regulation.

3. To determine a financial institution’s compliance with the

regulation, specifically in meeting the following

requirements:

• Providing to customers notices of its privacy policies

and practices that are timely, accurate, clear and

conspicuous, and delivered so that each customer can

reasonably be expected to receive actual notice;

• Disclosing nonpublic personal information to

nonaffiliated third parties, other than under an

exception, after first meeting the applicable

requirements for giving consumers notice and the

right to opt out;

• Appropriately honoring consumer opt out directions;

Lawfully using or disclosing nonpublic personal

information received from a nonaffiliated financial

institution; and

Disclosing account numbers only according to the

limits in the regulation.

4. To initiate effective corrective actions when violations of

law are identified, or when policies, procedures, or

internal controls are deficient.

Examination Procedures

10

A. Through discussions with management and review of

available information, identify the institution’s

information sharing practices (and changes to those

practices) with affiliates and nonaffiliated third parties;

how it treats nonpublic personal information; and how it

administers opt-outs. Consider the following as

appropriate:

FDIC Consumer Compliance Examination Manual — April 2021

VIII–1.7

VIII. Privacy — GLBA

1. Notices (initial, annual, revised, opt out, short-form,

and simplified);

2. Institutional privacy policies, procedures, and internal

controls, including those to:

• Process requests for nonpublic personal

information, including requests for aggregated

information;

• Deliver notices to consumers;

• Manage consumer opt out directions (e.g.,

designating files, allowing a reasonable time to

opt out, providing new opt out and privacy notices

when necessary, receiving opt out directions,

handling joint account holders);

• Prevent the unlawful disclosure and use of the

information received from nonaffiliated financial

institutions; and

prevent the unlawful disclosure of account

numbers;

3. Information sharing agreements between the

institution and affiliates and service agreements or

contracts between the institution and nonaffiliated

third parties either to obtain or provide information or

services;

4. Complaint logs, telemarketing scripts, and any other

information obtained from nonaffiliated third parties

(NOTE: review telemarketing scripts to determine

whether the contractual terms set forth under section

13 are met and whether the institution is disclosing

account number information in violation of section

12);

5. Categories of nonpublic personal information

collected from or about consumers in obtaining a

financial product or service (e.g., in the application

process for deposit, loan, or investment products; for

an over-the-counter purchase of a bank check; from

E-banking products or services, including information

collected electronically through Internet cookies; or

through ATM transactions);

6. Categories of nonpublic personal information shared

with, or received from, each nonaffiliated third party;

7. Consumer complaints regarding the treatment of

nonpublic personal information, including those

received electronically;

8. Records that reflect the bank’s categorization of its

information sharing practices under Sections 13, 14,

15, and outside of these exceptions; and

9. Results of a 501(b) inspection (used to determine the

accuracy of the institution’s privacy disclosures

regarding information security).

B. Use the information gathered from step A to work through

(Attachment A). Identify which module(s) of procedures

is (are) applicable.

C. Use the information gathered from step A to work through

the Redisclosure and Reuse and Account Number Sharing

Decision Trees, as necessary (Attachments B and C).

Identify which module is applicable.

D. Determine the adequacy of the financial institution’s

policies, procedures, and internal controls to ensure

compliance with the regulation as applicable. Consider

the following:

1. Sufficiency of internal policies, procedures, and

internal controls, including review of new products

and services and controls over servicing arrangements

and marketing arrangements;

2. Effectiveness of management information systems,

including the use of technology for monitoring,

exception reports, and standardization of forms and

procedures;

3. Frequency and effectiveness of monitoring

procedures;

4. Adequacy and regularity of the institution’s training

program;

5. Suitability of the compliance audit program for

ensuring that:

• The procedures address all regulatory provisions

as applicable;

• The work is accurate and comprehensive with

respect to the institution’s information sharing

practices;

• The frequency is appropriate;

• Conclusions are appropriately reached and

presented to responsible parties;

• Steps are taken to correct deficiencies and to

follow-up on previously identified deficiencies;

and

6. Knowledge level of management and personnel.

E. Ascertain areas of risk associated with the financial

institution’s sharing practices (especially those within

Section 13 and those that fall outside of the exceptions)

and any weaknesses found within the compliance

management program. Keep in mind any outstanding

deficiencies identified in the audit for follow-up when

completing the modules.

F. Based on the results of the foregoing initial procedures

and discussions with management, determine which

procedures if any should be completed in the applicable

module, focusing on areas of particular risk. The selection

of procedures to be employed depends upon the adequacy

of the institution’s compliance management system and

level of risk identified. Each module contains a series of

the “Privacy Notice and Opt Out Decision Tree”

general instructions to verify compliance, cross-referenced

VIII–1.8 FDIC Consumer Compliance Examination Manual — April 2021

VIII. Privacy — GLBA

to cites within the regulation. Additionally, there are

cross-references to a more comprehensive checklist, which

the examiner may use if needed to evaluate compliance in

more detail.

G. Evaluate any additional information or documentation

discovered during the course of the examination according

to these procedures. Note that this may reveal new or

different sharing practices necessitating reapplication of

the Decision Trees and completion of additional or

different modules.

H. Formulate conclusions.

Summarize all findings.

• For violation(s) noted, determine the cause by

identifying weaknesses in internal controls,

compliance review, training, management oversight,

or other areas.

• Identify action needed to correct violations and to

address weaknesses in the institution’s compliance

system, as appropriate.

• Discuss findings with management and obtain a

commitment for corrective action.

FDIC Consumer Compliance Examination Manual — April 2021

VIII–1.9

VIII. Privacy — GLBA

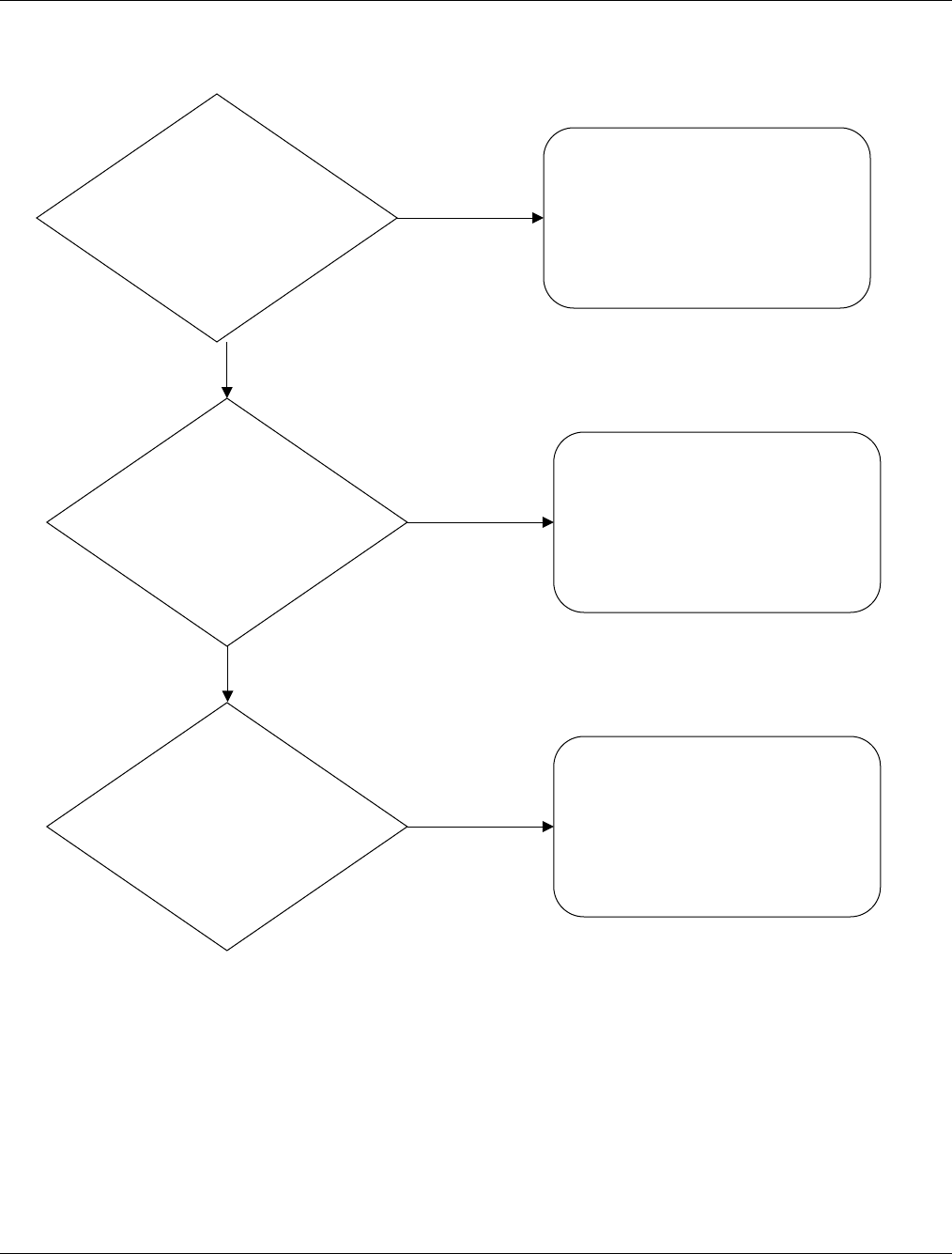

Privacy Notice and Opt Out Decision Tree

Does the

financial institution share

nonpublic personal information with

nonaffiliated third parties under sections 14

and/or 15 and outside of the exceptions

(with or without also sharing

under 13)?

No

Does the financial

institution share nonpublic personal

information with nonaffiliated third parties under

sections 13, and 14 and/or 15 but not

outside of the exceptions?

No

Module 1

Privacy Notice (presentation, content and

delivery)(with or without section 13 notice and

Yes

contracting)

Short form notice (optional for consumers)

Customer notice delivery rules

Opt out rules

Module 2

Yes

Privacy Notice

Customer notice delivery rules

Section 13 notice and contracting

Module 3

Does the financial institution share

Privacy Notice

Yes

nonpublic personal information with nonaffiliated

Simplified notice (if applicable)

third parties only under sections 14 and/or

Customer notice delivery rules

15

VIII–1.10 FDIC Consumer Compliance Examination Manual — April 2021

VIII. Privacy — GLBA

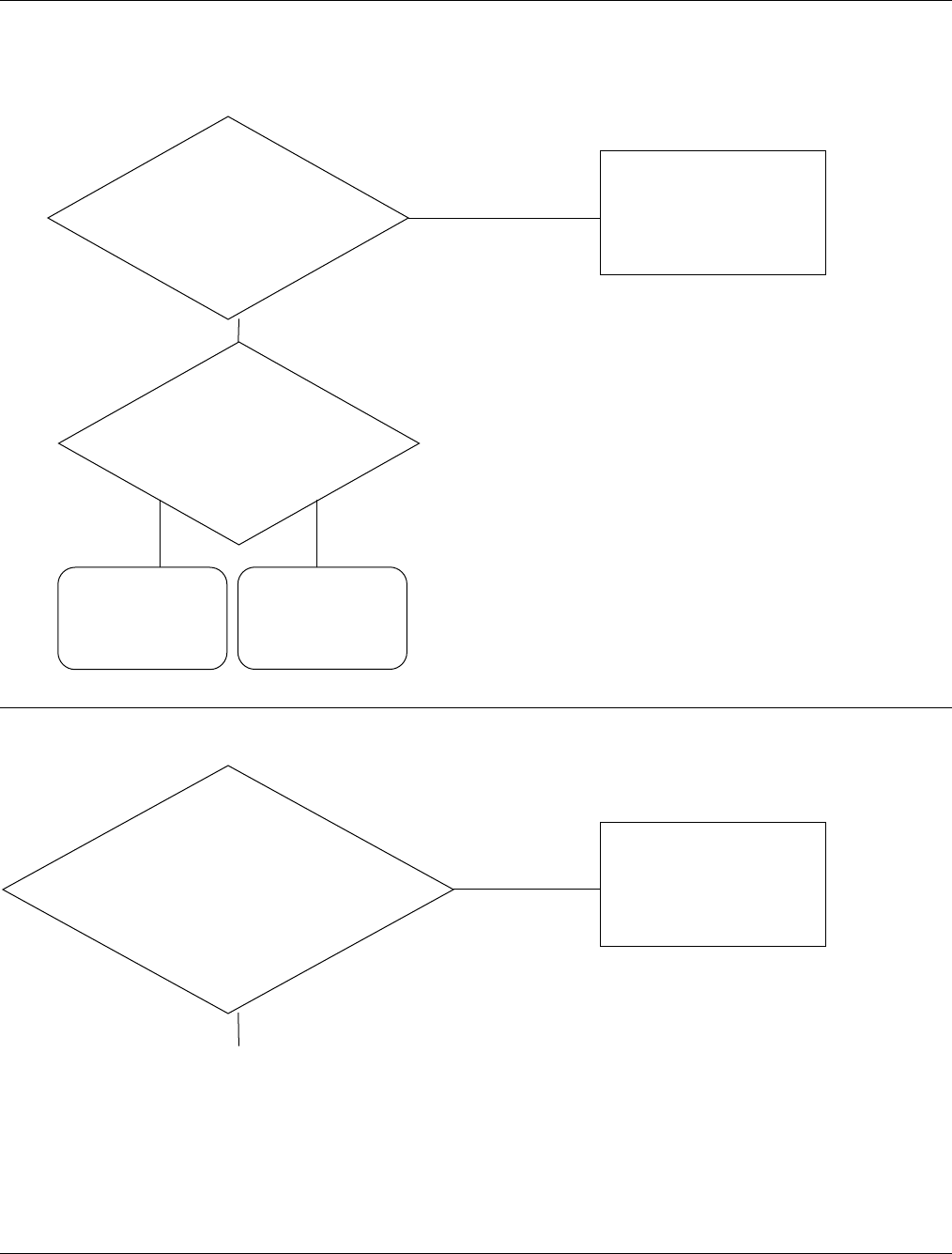

Redisclosure and Reuse of Nonpublic Personal Information Received from Nonaffiliated Financial Institutions Decision Tree

(Sections 11(a) and 11(b))

Does the financial institution

receive nonpublic public personal information from

nonaffiliated financial institutions?

How is that information received?

Module 4

Receipt of information

under 14 and/or 15

Module 5

Receipt of information

outside 14 and/or 15

Yes

Under Sections

14 and/or 15

Outside of Sections

14 and/or 15

No

No review necessary

Account Number Sharing Decision Tree (Section 12)

Does the financial institution

share account numbers or similar access

numbers or codes with nonaffiliated thrid parties (other

than a consumer reporting agency) for telemarketing,

direct mail or electronic mail

marketing?

No*

No review necessary

Module 6

Account number sharing

Yes

*This may include sharing of encrypted account numbers but not the decryption key.

FDIC Consumer Compliance Examination Manual — April 2021 VIII–1.11

VIII. Privacy — GLBA

Module 1

Sharing nonpublic personal information with nonaffiliated

third parties under Sections 14 and/or 15 and outside of the

exceptions (with or without also sharing under Section 13).

NOTE: Financial institutions whose practices fall within this

category engage in the most expansive degree of information

sharing permissible. Consequently, these institutions are held

to the most comprehensive compliance standards imposed by

the regulation.

NOTE: As of December 4, 2015, a financial institution is not

required to provide an annual privacy notice to its applicable

customers if it: (1) solely shares nonpublic personal

information in accordance with the provisions of GLBA

sections 502(b)(2) (corresponding to Regulation P section

1016.13) or 502(e) (corresponding to Regulation P sections

1016.14 and .15) or regulations prescribed under GLBA

section 504(b); and (2) has not changed its policies and

practices with regard to disclosing nonpublic personal

information since its most recent disclosure to its customers

that was made in accordance with GLBA section 503. A

financial institution that at any time fails to comply with either

of the criteria is not eligible for the exception and is required

to provide an annual privacy notice to its customers.

A. Disclosure of Nonpublic Personal Information

1. Select a sample of third party relationships with

nonaffiliated third parties and obtain a sample of

information shared between the institution and the

third party both inside and outside of the exceptions.

The sample should include a cross-section of

relationships but should emphasize those that are

higher risk in nature as determined by the initial

procedures. Perform the following comparisons to

evaluate the financial institution’s compliance with

disclosure limitations.

a. Compare the categories of information shared and

with whom the information was shared to those

stated in the privacy notice and verify that what

the institution tells consumers (both customers

and those who are not customers) in its notices

about its policies and practices in this regard and

what the institution actually does are consistent.

(Sections 6,10)

b. Compare the information shared to a sample of

opt out directions and verify that only nonpublic

personal information covered under the

exceptions or from consumers (customers and

those who are not customers) who chose not to

opt out is shared (Section 10).

2. If the financial institution also shares information

under Section 13, obtain and review contracts with

nonaffiliated third parties that perform services for the

financial institution not covered by the exceptions in

section 14 or 15. Determine whether the contracts

prohibit the third party from disclosing or using the

information other than to carry out the purposes for

which the information was disclosed (Section 13(a))

B. Presentation, Content, and Delivery of Privacy Notices

1. Review the financial institution’s initial, annual and

revised notices, as well as any short-form notices that

the institution may use for consumers who are not

customers. Determine whether or not these notices:

a. Are clear and conspicuous (Sections 3(b), 4(a),

5(a)(1), 8(a)(1));

b. Accurately reflect the institution’s policies and

practices. (Sections 4(a), 5(a)(1), 8(a)(1))

NOTE: this includes policies and practices

disclosed in the notices that exceed regulatory

requirements; and

c. Include, and adequately describe, all required

items of information and contain examples as

applicable (Section 6). Note that if the institution

shares under nonpublic personal information

under Section 13 the notice provisions for that

section shall also apply.

d. If the model privacy form is used, determine that

it reflects the institution’s policies and practices.

For institutions seeking a safe harbor for

compliance with the content requirements of the

regulation, verify that the notice has the proper

content and is in the proper format as specified in

the Appendix A of the regulation.

2. Through discussions with management, review of the

institution’s policies, procedures, and internal controls

and a sample of electronic or written consumer

records where available, determine if the institution

has adequate policies, procedures, and internal

controls in place to provide notices to consumers, as

appropriate. Assess the following:

Timeliness of delivery (Sections 4(a), 7(c), 8(a)); and

a. Reasonableness of the method of delivery (e.g.,

by hand; by mail; electronically, if the consumer

agrees; or as a necessary step of a transaction)

(Section 9).

b. For customers only, review the timeliness of

delivery (Sections 4(d), 4(e), 5(a)), means of

delivery of annual notice (Section 9(c)), and

accessibility of or ability to retain the notice

(Section 9(e)).

C. Opt Out Right

1. Review the financial institution’s opt out notices. An

opt out notice may be combined with the institution’s

privacy notices. Regardless, determine whether the

opt out notices:

VIII–1.12 FDIC Consumer Compliance Examination Manual — April 2021

VIII. Privacy — GLBA

a. Are clear and conspicuous (Sections 3(b) and

7(a)(1));

b. Accurately explain the right to opt out (Section

7(a)(1));

c. Include and adequately describe the three required

items of information (the institution’s policy

regarding disclosure of nonpublic personal

information, the consumer’s opt out right, and the

means to opt out) (Section 7(a)(1)); and

d. Describe how the institution treats joint

relationships, as applicable (Section 7(d)).

2. Through discussions with management, review of the

institution’s policies, procedures, and internal controls

and a sample of electronic or written consumer

records where available, determine if the institution

has adequate policies, procedures, and internal

controls in place to provide notices to consumers, as

appropriate. Assess the following:

a. Timeliness of delivery (Section 10(a)(1));

b. Reasonableness of the method of delivery (e.g.,

by hand; by mail; electronically, if the consumer

agrees; or as a necessary step of a transaction)

(Section 9).

c. Reasonableness of the opportunity to opt out (the

time allowed to and the means by which the

consumer may opt out) (Sections 10(a)(1)(iii),

10(a)(3)); and

d. Adequacy of procedures to implement and track

the status of a consumer’s (customers and those

who are not customers) opt out direction,

including those of former customers (Section 7(e),

(f), (g)).

D. Checklist Cross References—Module1

Regulation

Section

Subject

Checklist

Questions

4(a); 6(a, b, c, e);

and 9(a, b, g)

Privacy notices

(presentation,

content, and

delivery)

2, 8-11, 14, 18,

35, 36, 41

4(a, c, d, e); 5;

and 9(c, e)

Customer notice

delivery rules

1, 3-7, 37, 39

13

Section 13 notice

and contracting

rules (as

applicable)

12, 48

6(d)

Short form notice

rules (optional

for consumers

only)

15-17

7; 8; and 10

Opt out rules

19-34, 42-44

14, 15

Exceptions

49- 50

FDIC Consumer Compliance Examination Manual — April 2021 VIII–1.13

VIII. Privacy — GLBA

Module 2

Sharing nonpublic personal information with nonaffiliated

third parties under Sections 13, and 14 and/or 15 but not

outside of these exceptions

NOTE: As of December 4, 2015, a financial institution is not

required to provide an annual privacy notice to its applicable

customers if it: (1) solely shares nonpublic personal

information in accordance with the provisions of GLBA

sections 502(b)(2) (corresponding to Regulation P section

1016.13) or 502(e) (corresponding to Regulation P sections

1016.14 and .15) or regulations prescribed under GLBA

section 504(b); and (2) has not changed its policies and

practices with regard to disclosing nonpublic personal

information since its most recent disclosure to its customers

that was made in accordance with GLBA section 503. A

financial institution that at any time fails to comply with either

of the criteria is not eligible for the exception and is required

to provide an annual privacy notice to its customers.

A. Disclosure of Nonpublic Personal Information

1. Select a sample of third party relationships with

nonaffiliated third parties and obtain a sample of

information shared between the institution and the

third party. The sample should include a cross-section

of relationships but should emphasize those that are

higher risk in nature as determined by the initial

procedures. Perform the following comparisons to

evaluate the financial institution’s compliance with

disclosure limitations.

a. Compare the information shared and with whom

the information was shared to ensure that the

institution accurately categorized its information

sharing practices and is not sharing nonpublic

personal information outside the exceptions.

(Sections 13, 14, 15)

b. Compare the categories of information shared and

with whom the information was shared to those

stated in the privacy notice and verify that what

the institution tells consumers in its notices about

its policies and practices in this regard and what

the institution actually does are consistent.

(Sections 10, 6)

c. If the model privacy form is used, determine that

it reflects the institution’s policies and practices.

For institutions seeking a safe harbor for

compliance with the content requirements of the

regulation, verify that the notice has the proper

content and is in the proper format as specified in

the Appendix of the regulation.

2. Review contracts with nonaffiliated third parties that

perform services for the financial institution not

covered by the exceptions in section 14 or 15.

Determine whether the contracts adequately prohibit

the third party from disclosing or using the

information other than to carry out the purposes for

which the information was disclosed (Section 13(a)).

B. Presentation, Content, and Delivery of Privacy Notices

1. Review the financial institution’s initial and annual

privacy notices. Determine whether or not they:

a. Are clear and conspicuous (Sections 3(b), 4(a),

5(a)(1));

b. Accurately reflect the institution’s policies and

practices (Sections 4(a), 5(a)(1)). Note, this

includes policies and practices disclosed in the

notices that exceed regulatory requirements; and

c. Include, and adequately describe, all required

items of information and contain examples as

applicable. (Sections 6, 13)

2. Through discussions with management, review of the

institution’s policies, procedures, and internal controls

and a sample of electronic or written consumer

records where available, determine if the institution

has adequate policies, procedures, and internal

controls in place to provide notices to consumers, as

appropriate. Assess the following:

a. Timeliness of delivery (Section 4(a)); and

b. Reasonableness of the method of delivery (e.g.,

by hand; by mail; electronically, if the consumer

agrees; as a necessary step of a transaction; or

pursuant to the alternative delivery method)

(Section 9).

c. For customers only, review the timeliness of

delivery (Sections 4(d), 4(e), and 5(a)), means of

delivery of annual notice Section 9(c)), and

accessibility of or ability to retain the notice

(Section 9(e)).

C. Checklist Cross References—Module 2

Regulation

Section

Subject

Checklist

Questions

4(a); 6(a, b, c, e);

and 9(a, b, g)

Privacy notices

(presentation,

content, and

delivery)

2, 8-11, 14, 18,

35, 36, 41

4(a, c, d, e); 5;

and 9(c, e)

Customer notice

delivery rules

1, 3-7, 37, 39

13

Section 13 notice

and contracting

rules

12, 48

14, 15

Exceptions

49-51

VIII–1.14 FDIC Consumer Compliance Examination Manual — April 2021

VIII. Privacy — GLBA

Module 3

Sharing nonpublic personal information with nonaffiliated

third parties only under Sections 14 and/or 15.

NOTE: This module applies only to customers.

NOTE: As of December 4, 2015, a financial institution is not

required to provide an annual privacy notice to its applicable

customers if it: (1) solely shares nonpublic personal

information in accordance with the provisions of GLBA

sections 502(b)(2) (corresponding to Regulation P section

1016.13) or 502(e) (corresponding to Regulation P sections

1016.14 and .15) or regulations prescribed under GLBA

section 504(b); and (2) has not changed its policies and

practices with regard to disclosing nonpublic personal

information since its most recent disclosure to its customers

that was made in accordance with GLBA section 503. A

financial institution that at any time fails to comply with either

of the criteria is not eligible for the exception and is required

to provide an annual privacy notice to its customers.

A. Disclosure of Nonpublic Personal Information

1. Select a sample of third party relationships with

nonaffiliated third parties and obtain a sample of

information shared between the financial institution

and the third party.

a. Compare the information shared and with whom

the information was shared to ensure that the

institution accurately states its information

sharing practices and is not sharing nonpublic

personal information outside the exceptions.

B. Presentation, Content, and Delivery of Privacy Notices

1. Obtain and review the financial institution’s initial

and annual notices, as well as any simplified notice

that the institution may use. Note that the institution

may only use the simplified notice when it does not

also share nonpublic personal information with

affiliates outside of Section 14 and 15 exceptions.

Determine whether or not these notices:

a. Are clear and conspicuous (Sections 3(b), 4(a),

5(a)(1));

b. Accurately reflect the institution’s policies and

practices (Sections 4(a), 5(a)(1)). Note, this

includes practices disclosed in the notices that

exceed regulatory requirements; and

c. Include, and adequately describe, all required

items of information (Section 6).

d. If the model privacy form is used, determine that

it reflects the institution’s policies and practices.

For institutions seeking a safe harbor for

compliance with the content requirements of the

regulation, verify that the notice has the proper

content and is in the proper format as specified in

the Appendix of the regulation.

2. Through discussions with management, review of the

institution’s policies, procedures, and internal controls

and a sample of electronic or written customer records

where available, determine if the institution has

adequate policies, procedures, and internal controls in

place to provide notices to customers, as appropriate.

Assess the following:

a. Timeliness of delivery (Sections 4(a), 4(d), 4(e),

5(a)); and

b. Reasonableness of the method of delivery (e.g.,

by hand; by mail; electronically, if the customer

agrees; as a necessary step of a transaction; or

pursuant to the alternative delivery method)

(Section 9) and accessibility of or ability to retain

the notice (Section 9(e)).

C. Checklist Cross References—Module 3

Regulation

Section

Subject

Checklist

Questions

4(a, d, e); 5; and

9

Customer notice

delivery process

1, 3,-7, 35-41

6

Customer notice

content and

presentation

8-11, 14, 18

6(c)(5);

Simplified notice

content

(optional)

13

14, 15

Exceptions

49-51

Module 4

Redisclosure and Reuse of nonpublic personal information

received from a nonaffiliated financial institution under

Sections 14 and/or 15.

A. Through discussions with management and review of the

institution’s policies, procedures, and internal controls,

determine whether the institution has adequate policies,

procedures, and internal controls to prevent the unlawful

redisclosure and reuse of the information where the

institution is the recipient of nonpublic personal

information (Section 11(a)).

B. Select a sample of information received from nonaffiliated

financial institutions, to evaluate the financial institution’s

compliance with redisclosure and reuse limitations.

1. Verify that the institution’s redisclosure of the

information was only to affiliates of the financial

institution from which the information was obtained

or to the institution’s own affiliates, except as

otherwise allowed in the step 2 below (Section

11(a)(1)(i) and (ii)).

FDIC Consumer Compliance Examination Manual — April 2021

VIII–1.15

VIII. Privacy — GLBA

2. Verify that the institution only uses and shares the

information pursuant to an exception in Sections 14

and 15 (Section 11(a)(1)(iii)).

C. Checklist Cross References—Module 4

Regulation

Section

Subject

Checklist

Questions

11(a)

Reuse and

45

disclosure

presentation

14, 15

Exceptions

49-51

Module 5

Redisclosure of nonpublic personal information received from

a nonaffiliated financial institution outside of Sections 14 and

15.

A. Through discussions with management and review of the

institution’s policies, procedures, and internal controls,

determine whether the institution has adequate policies,

procedures, and internal controls to prevent the unlawful

redisclosure of the information where the institution is the

recipient of nonpublic personal information (Section

11(b)).

B. Select a sample of information received from nonaffiliated

financial institutions and shared with others to evaluate the

financial institution’s compliance with redisclosure

limitations.

1. Verify that the institution’s redisclosure of the

information was only to affiliates of the financial

institution from which the information was obtained

or to the institution’s own affiliates, except as

otherwise allowed in the step 2 below (Section

11(b)(1)(i) and (ii)).

2. If the institution shares information with entities other

than those under step 1 above, verify that the

institution’s information sharing practices conform to

those in the nonaffiliated financial institution’s

privacy notice (Section 11(b)(1)(iii)).

3. Also, review the procedures used by the institution to

ensure that the information sharing reflects the opt out

status of the consumers of the nonaffiliated financial

institution (Sections 10, 11(b)(1)(iii)).

C. Checklist Cross References—Module 5

Module 6

Account number sharing

A. If available, review a sample of telemarketer scripts used

when making sales calls to determine whether the scripts

indicate that the telemarketers have the account numbers

of the institution’s consumers (Section 12(a)).

B. Obtain and review a sample of contracts with agents or

service providers to whom the financial institution

discloses account numbers for use in connection with

marketing the institution’s own products or services.

Determine whether the institution shares account numbers

with nonaffiliated third parties only to perform marketing

for the institution’s own products and services. Ensure that

the contracts do not authorize these nonaffiliated third

parties to directly initiate charges to the accounts (Section

12(b)(1)).

C. Obtain a sample of materials and information provided to

the consumer upon entering a private label or affinity

credit card program. Determine if the participants in each

program are identified to the customer when the customer

enters into the program (Section 12(b)(2)).

D. Checklist Cross References—Module 6

Regulation

Section

Subject

Checklist

Questions

12

Account number

sharing

47

References

CFPB Part 1016: Privacy of Consumer Financial Information

FIL 01-106: Privacy of Consumer Financial Information

(Includes a link to an FDIC Press Release that included FDIC

Staff Response to Questions Regarding the Privacy of

Consumer Financial Information

Regulation

Section

Subject

Checklist

Questions

11(b)

Redisclosure

46

VIII–1.16 FDIC Consumer Compliance Examination Manual — April 2021

VIII. Privacy — GLBA

Examination Checklist - Subpart A

Response

Initial Privacy Notice

1. Does the institution provide a clear and conspicuous notice that accurately reflects its

privacy policies and practice to all customers not later than when the customer relation-

ship is established, other than as allowed in paragraph (e) of section four (4) of the reg-

ulation? [§4(a)(1)]

Note: No notice is required if nonpublic personal information is disclosed to

nonaffiliated third parties only under an exception in Sections 14 and 15, and there is

no customer relationship. [§4(b)] With respect to credit relationships, an institution

establishes a customer relationship when it originates a consumer loan. If the

institution subsequently sells the servicing rights of the loan to another financial

institution, the customer relationship transfers with the servicing rights. [§4(c)]

Yes / No / NA

2. Does the institution provide a clear and conspicuous notice that accurately reflects its

privacy policies and practices to all consumers, who are not customers, before any non-

public personal information about the consumer is disclosed to a nonaffiliated third

party, other than under an exception in §§14 or 15? [§4(a)(2)]

Yes / No / NA

3. Does the institution provide to existing customers, who obtain a new financial product

or service, an initial privacy notice that covers the customer’s new financial product or

service, if the most recent notice provided to the customer was not accurate with respect

to the new financial product or service? [§4(d)(1))]

Yes / No / NA

4. Does the institution provide initial notice after establishing a customer relationship only if:

a. The customer relationship is not established at the customer’s election;

[§4(e)(1)(i)] or

Yes / No / NA

b. To do otherwise would substantially delay the customer’s transaction (e.g. in the

case of a telephone application), and the customer agrees to the subsequent deliv-

ery? [§4(e)(1)(ii)]

Yes / No / NA

5. When the subsequent delivery of a privacy notice is permitted, does the institution pro-

vide notice after establishing a customer relationship within a reasonable time? [§4(e)]

Yes / No / NA

Annual Privacy Notice

6. Does the institution provide a clear and conspicuous notice that accurately reflects its

privacy policies and practices at least annually (that is, at least once in any period of 12

consecutive months) to all customers, throughout the customer relationship? [§5(a)(1)

& (2)].

Note: §9(c)(1)(i ) & §9(c)(2)(i ) allow alternative methods of providing this notice.

Note: annual notices are not required for former customers. [§5(b)(1) and (2)]

Note: The FAST Act amends section 503 of the GLBA by adding an exception to the

annual privacy notice if the bank: i) provides nonpublic personal information only in

accordance with section 502(b)(2) or (e) or section 504(b); and ii) has not changed its

policies or procedures with regard to disclosing nonpublic personal information from

that were disclosed previously.

Yes / No / NA

7. Does the institution provide an annual privacy notice to each customer whose loan the

institution owns the right to service? [§§5(c), 4(c)(2)]

Yes / No / NA

Content of Privacy Notice

8. Do the initial, annual, and revised privacy notices include each of the following, as applicable:

a. The categories of nonpublic personal information that the institution collects;

[§6(a)(1))]

Yes / No / NA

b. The categories of nonpublic personal information that the institution discloses;

[§6(a)(2))]

Yes / No / NA

c. The categories of affiliates and nonaffiliated third parties to whom the institution

discloses nonpublic personal information, other than parties to whom information

is disclosed under an exception in §14 or §15; [§6(a)(3)]

Yes / No / NA

FDIC Consumer Compliance Examination Manual — April 2021

VIII–1.17

VIII. Privacy — GLBA

d. The categories of nonpublic personal information disclosed about former custom-

ers, and the categories of affiliates and nonaffiliated third parties to whom the in-

stitution discloses that information, other than those parties to whom the institution

discloses information disclosed under an exception in §14 or §15; [§6(a)(4)]

Yes / No / NA

e. If the institution discloses nonpublic personal information to a nonaffiliated third

party under §13, and no exception under §14 or §15 applies, a separate statement

of the categories of information the institution discloses and the categories of third

parties with whom the institution has contracts; [§6(a)(5)]

Yes / No / NA

f. An explanation of the opt out right, including the method(s) of opt out that the con-

sumer can use at the time of the notice; [§6(a)(6)]

Yes / No / NA

g. Any disclosures that the institution makes under §603(d)(2)(A)(iii) of the Fair

Credit Reporting Act (FCRA); [§6(a)(7)]

h. The institution’s policies and practices with respect protecting the confidentiality

and security of nonpublic personal information; [§6(a)(8)] and

Yes / No / NA

i. a general statement – with no specific reference to the third parties – that the insti-

tution makes disclosures to other nonaffiliated third parties for everyday business

purposes, such as (with the institution including all that are applicable) to process

transactions, maintain accounts, respond to court orders and legal investigations, or

report to credit bureaus, or as otherwise permitted by law? [Section 6(a)(9), (b)(1)

and (2)]

NOTE: Institutions that provide a model privacy form in accordance with the